Global| Nov 30 2007

Global| Nov 30 2007EU Sentiment is Fading Fast

Summary

Mixed but weakening, conditions. The monthly EU sectors show that weakness still stalks the EU region. Still some sectors have improved this month. The EU industrial index improved in November to +3 from +2. The retail index improved [...]

Mixed but weakening, conditions. The

monthly EU sectors show that weakness still stalks the EU region. Still

some sectors have improved this month. The EU industrial index improved

in November to +3 from +2. The retail index improved from +2 to +4.

Despite that consumer confidence slipped to -7 from -5. The

construction sector also switched from being flat to a -1 reading. But

the largest drop was in services where the index fell to +14 from +19.

The services readings now stand only in the 52nd percentile of its

range. Retailing and construction are still in the 90th-something

percentiles of their respective ranges. The industrial sector is now in

its 88th percentile. But consumer confidence has slipped to the 69th

percentile. While there is some mixture in these figures it is clear

that the consumer is beset with concerns while the MFG sector has held

up. Construction, not having ever been very strong, give us a very high

positive range ranking on a raw reading of -1.

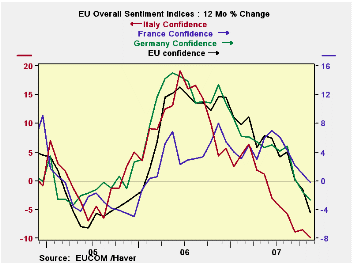

The good, the bad and the ugly. Across EMU

countries we find weaker conditions in general. The overall sentiment

is at a ranking of only the 71st percentile. France still ranks in its

81st percentile. Germany has slipped to its 64th. Italy and Spain hover

around the 50% mark for overall sentiment.

Risk of action…and inaction. On balance,

Europe is slipping but not yet doing poorly. But we know that exchange

rates work with a lag and there is more of that strong euro impact in

train. Also, that the recent inflation headline of 3% will send chills

up the spine of the ECB. Despite concerns of an overly strong EURO the

ECB with too-strong money and credit growth will have a hard time

balancing the things it wants to do (hike rates and fight inflation)

with the things it does not want to do (weaken already weakening growth

and spur an even stronger euro).

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Nov 07 |

Oct 07 |

Sep 07 |

Aug 07 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/ Overall |

| Overall | 107.6 | 109.6 | 110.6 | 113.1 | 78.5 | 62 | 117 | 74 | 43 | 100 | 1.00 |

| Industrial | 3 | 2 | 3 | 5 | 88.2 | 19 | 7 | -27 | 34 | -7 | 0.89 |

| Consumer Confidence | -7 | -5 | -4 | -3 | 69.0 | 60 | 2 | -27 | 29 | -10 | 0.82 |

| Retail | 4 | 2 | 1 | 6 | 92.6 | 7 | 6 | -21 | 27 | -6 | 0.47 |

| Construction | -1 | 0 | 1 | 0 | 91.1 | 17 | 3 | -42 | 45 | -18 | 0.44 |

| Services | 14 | 19 | 19 | 22 | 52.6 | 75 | 32 | -6 | 38 | 17 | 0.80 |

| % M/M | Based on Level |

Level | |||||||||

| EMU | -1.1% | -0.8% | -2.8% | -0.9% | 71.2 | 80 | 117 | 74 | 44 | 100 | 0.94 |

| Germany | 0.1% | -0.6% | -3.3% | -0.9% | 64.0 | 62 | 121 | 79 | 42 | 100 | 0.62 |

| France | -0.4% | 0.5% | -1.5% | -1.2% | 81.6 | 27 | 119 | 72 | 47 | 100 | 0.80 |

| Italy | -4.2% | -0.2% | -0.8% | -3.0% | 52.7 | 125 | 121 | 72 | 49 | 100 | 0.79 |

| Spain | -0.2% | -2.7% | -3.4% | 1.1% | 50.0 | 178 | 118 | 67 | 50 | 100 | 0.65 |

| Memo: UK | -4.4% | -2.0% | 1.1% | 4.5% | 78.2 | 60 | 119 | 69 | 50 | 101 | 0.40 |

| Since 1990 except Services(Oct 1996) | 208 | -Count | Services: | 126 | -Count | ||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief