Global| Mar 18 2020

Global| Mar 18 2020EU Passenger Car Registrations Tick Higher But Are Broadly Weak While Markets Remain Broadly Scared

Summary

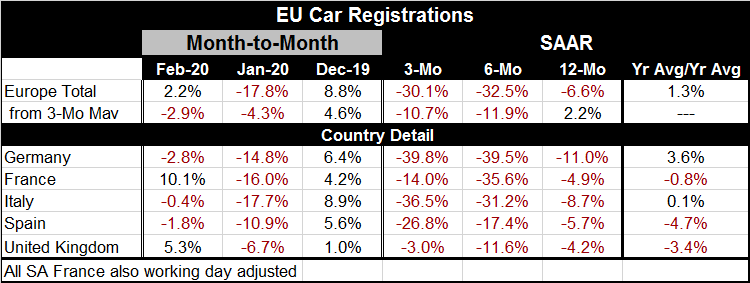

Car registrations weakened sharply in January ahead of any virus effect in Europe. In February, sales edged higher by 2.2%. Still, that leaves sales/registrations falling at a 30% annual rate over three months, falling at a 32% annual [...]

Car registrations weakened sharply in January ahead of any virus effect in Europe. In February, sales edged higher by 2.2%.

Car registrations weakened sharply in January ahead of any virus effect in Europe. In February, sales edged higher by 2.2%.

Still, that leaves sales/registrations falling at a 30% annual rate over three months, falling at a 32% annual rate over six months and falling by 6.6% over 12 months.

Those hyper-weak growth rates are moderated by calculating growth from three-month average data. On that basis, sales fall in February by 2.9% after falling by 4.3% in January. The smoothed three-month growth rate clocks a -10.7% annual rate of decline compared to -11.9% over six months and a small 2.2% rise over 12 months.

For the broadest smoothing the last 12-month average for sales is up by 1.3% over the previous 12-month average in sales (13 through 24 months ago). On balance, these smoothing operations seem to identify a rising trend, but it is a trend that is rising very, very, slowly. Unsmoothed data tell a much more worrisome story of momentum.

Unsmoothed country level data show declines in three of five countries in February compared to decline in five of five in January which followed expanded sales across the board in December. Unsmoothed country level data show registration declines in all five countries over all three horizons of three-months, six-months and 12-months. The pace of decline escalates consistently in Germany, Spain and Italy.

In big broad terms, the year average change over the previous year average in registrations shows declines in registrations in France, Spain and in the EU. Italy ekes out a technical gain of 0.1% and Germany logs a strong 3.6% rise on this very broad sluggish gauge.

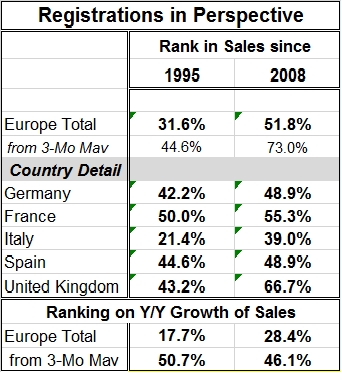

Table “Registrations in Perspective” ranks the current sales pace against the sales paces back to 1995 and also on a shorter timeline back to 2008. All countries show stronger sales rankings over the 2008 period when car registrations were weaker. On the longer timeline, only France has sales ranking above the 50% mark that identifies its median. Sales everywhere else are below their historic median pace; in Italy they are particularly weak with only a 21.4 percentile ranking back to 1995.

Table “Registrations in Perspective” ranks the current sales pace against the sales paces back to 1995 and also on a shorter timeline back to 2008. All countries show stronger sales rankings over the 2008 period when car registrations were weaker. On the longer timeline, only France has sales ranking above the 50% mark that identifies its median. Sales everywhere else are below their historic median pace; in Italy they are particularly weak with only a 21.4 percentile ranking back to 1995.

Ranked on the growth rate of sales instead of the number of sales Europe’s ranking back to 1995 is only 17.7%, much weaker than its ranking of 31.6% based on the number of sales. However, ranked on smoothed data those results reverse with the growth ranking rising sharply to 50.7% above its historic median compared to 17.7% unsmoothed. This also points out how much of the sales weakness reflects recent weakness.

The coming European scene

On balance, European car sales/registrations are weak and have lost a great deal of momentum recently. With the coronavirus beginning to take hold, these sales are going to weaken even more. Several car makers have announced that they are shuttering production facilities for a while.

The unfolding global scene

Globally we are seeing a sharp market reaction of heretofore unknown proportions. Despite central banks cutting rates to (and in some cases through) zero, we see bond yields now on the rise. The steepened yield curve reflects concerns that so much global fiscal stimulus with the monetary spigot wide open will become inflationary. However, there has been no inflation to speak of for many years among the major monetary center countries. Has the virus changed the facts and the paradigm? It is possible, of course. But what I see is a desperate need for the RIGHT KIND of fiscal spending to underpin demand at a time that private demand is going to be flat or contract at least in part due to actions taken to slow the spread of the virus. Some people will lose jobs and income and will have to dig into savings if they have any. Others will maintain income but will be all but confined to quarters, as so many businesses are shuttered. This is an arrangement that will push up their savings rate. Spending overall is hardly posed to accelerate and ‘strain’ systemic capabilities. That is not what is happening. There is no crowding out. But with weak growth and weak prospects companies may find rolling over maturing bonds is more difficult than they expected.

The future: Inflation or deflation?

In the U.S. as well as in Europe municipalities are crying for more central government funding as the various business and event closings have hit the transportation sector hard and cities with large transportation networks are running massive deficits as a result of corona attenuation programs. Government funding is needed to close that gap. For the most part, it appears as though federal spending will not be in addition to private spending but will substitute for it in large part. The rise in bond yields and the yield curve steepening that we see is precautionary, but I do not see it as presaging in a higher inflation era ahead. In all likelihood even with more government spending and higher government debt-to-GDP ratios, the world’s economies are not going to be as strong in the period ahead and inflation is not going to be ignited by ‘fiscal excess.’ For one thing oil prices are now going down the rabbit hole and with demand ever weakening the Saudis are going to find it very hard to regain control of that one… The bigger worry right now, paradoxically, is probably deflation even with all this global fiscal spending.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief