Global| Feb 27 2020

Global| Feb 27 2020EU Indexes Show Monthly Improvement; Can It Be Sustained?

Summary

The EU Commission sector indexes showed improvement or stability in February with no declines logged among the major components. Among the 18 reporting EMU members, only five showed a decline in overall sentiment on the month compared [...]

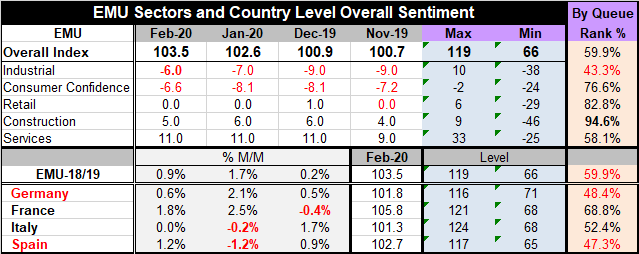

The EU Commission sector indexes showed improvement or stability in February with no declines logged among the major components. Among the 18 reporting EMU members, only five showed a decline in overall sentiment on the month compared to 6 in January and 8 in December. Germany, Austria, Belgium and Estonian have no declines logged in the past three months while only Finland shows declines in each of the last three months. On data ranked back to 1998 (where possible), the queue standings of the current indexes are still weak with only 10 of the 18 displaying rankings above the 50th percentile mark that represents the median for each series. That means that for a large number of members performance remains sub-standard. The ranking for the pooled and weighted data represented by the EMU index shows a 59.9 percentile standing. The EMU index has improved month-to-month for three months running.

The EU Commission sector indexes showed improvement or stability in February with no declines logged among the major components. Among the 18 reporting EMU members, only five showed a decline in overall sentiment on the month compared to 6 in January and 8 in December. Germany, Austria, Belgium and Estonian have no declines logged in the past three months while only Finland shows declines in each of the last three months. On data ranked back to 1998 (where possible), the queue standings of the current indexes are still weak with only 10 of the 18 displaying rankings above the 50th percentile mark that represents the median for each series. That means that for a large number of members performance remains sub-standard. The ranking for the pooled and weighted data represented by the EMU index shows a 59.9 percentile standing. The EMU index has improved month-to-month for three months running.

Of course, the disconnection here is that the coronavirus has been spreading and poses an ever greater risk globally. Among EMU members, Italy is affected the worst so far, but this month Italy’s economic sentiment is flat month-to-month. Global stock markets have been dropping sharply and yet these indexes show a tranquil ongoing improvement. Somehow I have to wonder about this and must urge a certain ‘open-mindedness’ to the results of this report that might find responses quite different one month from now.

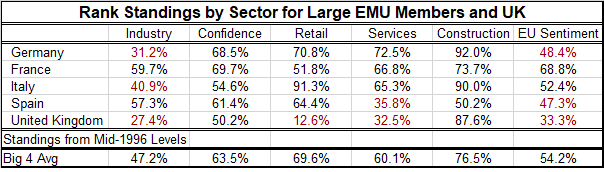

Percentile standings for the largest EMU economics and the United Kingdom.

The rankings of the various sectors for countries shows only consumer confidence and construction sectors with no readings below a 50th percentile standing. The weakest sector reading that also drags down the EU sentiment reading for each country is for industry. Only Spain and France have percentile standings above their respective medians in the sector. Germany and the U.K. are especially weak.

The EMU industrial survey shows weakness and below median readings across the surveyed components. Only the inventory assessment is above median and that might not be a good sign. Production expectations are well below their medians with a 34.1 queue percentile standing; order volume is about ten diffusion points higher, but it is still below 50, where its median occurs.

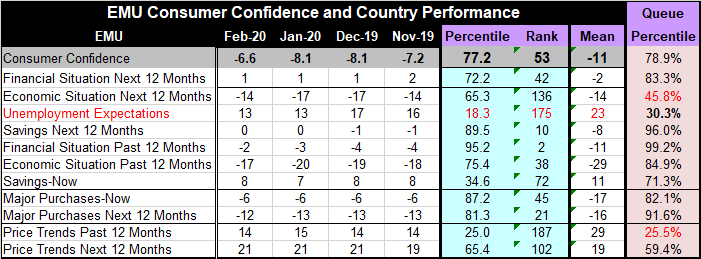

Consumer confidence has a relatively strong 78.9 percentile standing. Components are strong across the surveyed components. Only two components, the financial situation expected over the next 12-months and past price trends have below-median assessments. Overall consumer responses are strong across the board.

The EU Commission indexes showing similar weaknesses are to those chronicled in the Markit report. Overall and sector weakness for the industrial sector and the services sector are similar in the EU Commission indexes to what is recorded by the Markit indexes. The Markit indexes have a weaker standing overall. The industrial gauge is weaker in the EU framework, but the services sector has weaker standing in the in the Markit framework. Still, it’s all about weakness.

The question for the month is whether this EU survey will stand up next month. The gradual claw back to stability that is reflected in the headline, the sectors, as well as across country readings with few countries declines month-to-month are their own powerful signs of stability. But we are seeing broadly weak signs for financial markets and also from economic variables. Do the signals in this report trump those of more recent events or are they about to be swamped by them?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief