Global| Jan 07 2021

Global| Jan 07 2021EU Indexes Show a Net Gain for December But Mixed Trends

Summary

The comprehensive EU indexes for December echo some of the recent findings of the Markit indexes for manufacturing and services. We see in the EU framework that the overall index rises month-to-month to 90.4 in December from 87.7 in [...]

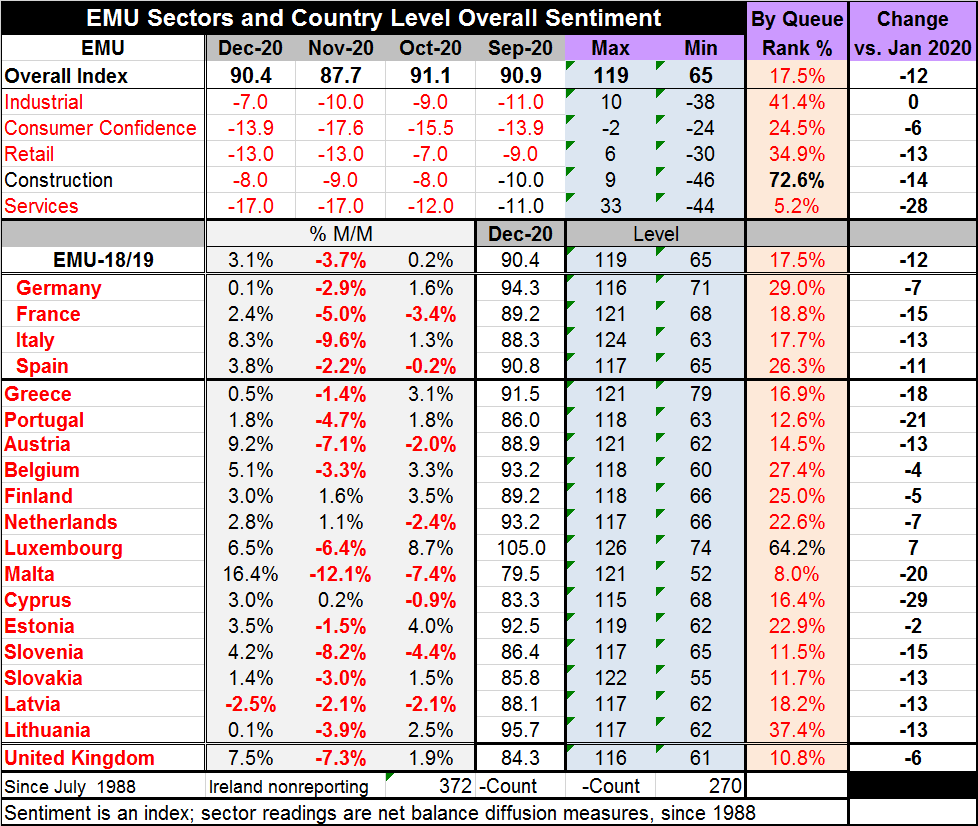

The comprehensive EU indexes for December echo some of the recent findings of the Markit indexes for manufacturing and services. We see in the EU framework that the overall index rises month-to-month to 90.4 in December from 87.7 in November. The Markit composite index also improved month-to-month.

The comprehensive EU indexes for December echo some of the recent findings of the Markit indexes for manufacturing and services. We see in the EU framework that the overall index rises month-to-month to 90.4 in December from 87.7 in November. The Markit composite index also improved month-to-month.

In the Markit presentation both manufacturing and services improved in December. Not so with the EU framework. There the industrial sector improved but the services sector was unchanged after weakening the previous month. In the EU framework retailing also was unchanged in December and the construction sector improved somewhat. Consumer confidence took a step for the better. Assessed over the same period, the Markit manufacturing gauge is much stronger relative to its history than is the EU gauge. For services, the Markit gauge is the slightly weaker one. The broad strokes that match, however, are that manufacturing is doing much better and the services sector is lagging. That is reassuring since everything we see up close and personal about how the virus is impacting the economy suggests that is what it is doing. And it is doing that everywhere, regardless of the method used to asses it.

The EMU is also undergoing another round of virus spread in January, building on the worsening situation from December. The steps taken to contain the virus are becoming more stringent. It is unclear how much the virus disturbed outcomes in December since it was also circulating and worsening then. While policymakers were admonishing people to stay home and to only mingle with the people with whom they lived, and not to travel… because of the holidays, no one really put their foot down to stop ravel or halt at-home gatherings. In fact, in NYC where the virus was not spreading that fast at the time restaurants that had been allowed 25% indoor occupancy were shut for inside eating undoubtedly forcing more people into the more dangerous at-home meetings. All that undoubtedly helped to sow the seeds for the worsening that is being experienced in January with Angela Merkel in Germany using especially strong language to warn Germans that if they do not obey the German rules the rules will get tougher and last longer. The U.K. has a serious outbreak and a new more communicable strain of the virus circulating. January is sure to be worse than December.

As of December, however, only the construction industry metric has a standing above its median. Among the 18 reporting EMU members, only Luxembourg has a reading above its historic median. The standing for EMU overall is only in its 17.5 percentile- a very weak reading. However, in December after a broad slide in November, EMU reporters indicate a month-to-month improvement everywhere except in Latvia. The overall EMU gauge improved by 3.1% in December after falling by 3.7% in November. On balance, the EMU gauge still is lower than its September and October readings even with the sizeable December rebound.

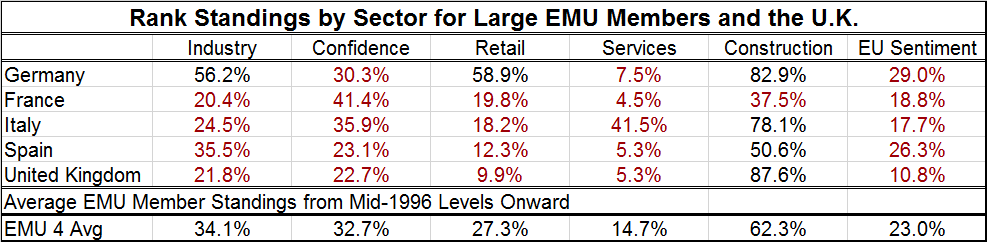

Turning to the standings of the various sectors in the largest EMU member economies and the U.K., the table below shows that the construction sector is the strongest or just about the strongest reading everywhere. Only Germany has three industries with readings above their historic medians (above 50%). Italy, Spain and the U.K. each have only one. France has none, but its strongest sector at a 37.5 percentile standing is construction.

Italy has the relative strongest services sector; the Italians have been obstreperous about closing their services sector down. Germany has the relative strongest industry and retail sectors by a long shot. Confidence is relatively strongest in France compared other places. The U.K. readings are at or among the weakest in all categories except construction where it posts the highest relative reading of all. Still, overall sentiment is the lowest in the U.K. and the highest in Germany.

The percentile standings mark this as a time of extreme weakness. The Markit view sees more resiliency in manufacturing than the EU survey sees in its industry metric. The standings for the past four years show currently about the largest discrepancy between the two surveys in their assessment of the industrial or manufacturing sectors on that timeline. In the past, these differences have not persisted.

The vaccines were first seen as a Godsend, but as time marches on we begin to see them as the foot-soldiers against the disease that they are. They are not instant panaceas and their rollout takes a lot of logistical input. The new virus strain has increased the pressure to distribute the vaccine more widely more quickly and this desperation is leading to some rethinking about how the vaccines can be deployed. In sum, there are still not easy answers. The existence of vaccines that are approved for use but still not fully known does provide some reassurance that the disease will be corralled in some sort of timely fashion, but putting tight parameters on what that really means is still beyond the scope of policy. The disease remains a global problem with Japan just declaring a new state of emergency. No country seems to have the magic touch. Those that at first were more successful are now having more problems. The surprise is that China, where it all started, seems to have emerged the fastest and with the most complete recovery. But we do not know what China really encountered or what it did and it is still blocking WHO investigators from doing their jobs one year after the outbreaks began in China. One year on, and still no cooperation from China.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief