Global| Sep 29 2020

Global| Sep 29 2020EU Indexes Continue to Claw Their Way Back with Speed But from the Depths

Summary

This month the EU indexes for the EMU area rose to 91.1 from 87.5; another strong month-to-month gain. There were improvements in all sector segments month-to-month. With services making a very strong gain, notching a five-point (net [...]

This month the EU indexes for the EMU area rose to 91.1 from 87.5; another strong month-to-month gain. There were improvements in all sector segments month-to-month. With services making a very strong gain, notching a five-point (net diffusion points) improvement from August, the overall sentiment reading for September has been pushed strongly higher.

This month the EU indexes for the EMU area rose to 91.1 from 87.5; another strong month-to-month gain. There were improvements in all sector segments month-to-month. With services making a very strong gain, notching a five-point (net diffusion points) improvement from August, the overall sentiment reading for September has been pushed strongly higher.

By Sector- However, even with those gains, the EMU index standing is only in its 18.5 percentile, the lower one fifth of its historic queue of values. Services, despite their strong gain on the month, have an even weaker 5.9 percentile standing. The industrial and consumer sectors register mid-20th percentile queue standings. Retailing nearly gets back to its median with a 49.2 percentile standing. Construction alone is above its median with a 69.1 percentile standing. Clearly, by ranking metric, it is the services sector that is holding things back the most. And that is the sector that generally requires the most face-to-face contact with customers. Progress there is being held back the most by the virus that has just stepped up is spread across Europe. Right now it looks like we will have to hold our breath for October since it looks like the virus is going to have a significant depressing effect.

By Country- The results by country show that of the 18 early-reporting EMU nations all four showed improvements –and unusually substantial improvements in September. Only six countries have had a setback in one of the last two months as recovery has been strong and steady with substantial breadth across the EMU. However, Greece, Finland and Luxembourg each have seen declines in each of the last two months. Cyprus and Slovakia registered a decline in September.

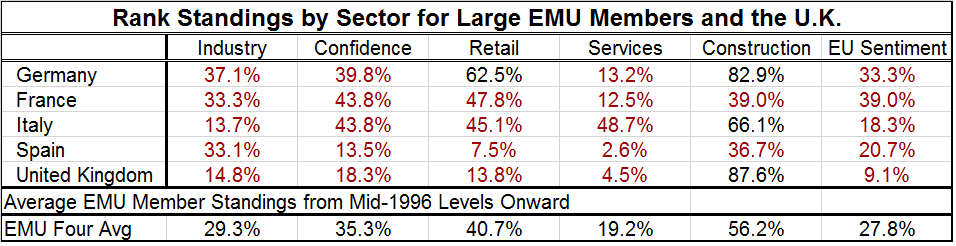

Levels vs. Changes in Levels- Despite the substantial and broad traction for recovery, the EMU area has only an 18.5 percentile standing for its aggregated and weighted sentiment index. The four largest economies in the EMU show France with a 39.0 percentile standing, Germany with a 33.3 percentile standing, Spain with a 20.7 percentile standing and Italy with an 18.3 percentile standing. Among the other 14 early-reporters in the EMU, ten have percentile standings in the lower one-fifth of their historic queues of data. Only tiny Lithuania and Luxembourg have standings above their lower one-third. Despite the widespread traction of recovery, the process still has a long way to go to get back to normalcy let alone strength.

Sector Performance in Large Countries- The small table below gives a bit more information on sectors by country by focusing on the four largest EMU economies plus the United Kingdom. The U.K. still has the lowest sentiment standing among this group; it has the second lowest standing in every category except for the small construction sector where it ranks as the strongest. All sectors in the large EMU countries are below their median rankings except for construction in Germany and in Italy. Except for Italy, each country has the service sector with the relative weakest standing. Services have the second-best sector standing in Italy. However, that is an idiosyncrasy and everywhere else services are pulling the overall sentiment ranking lower.

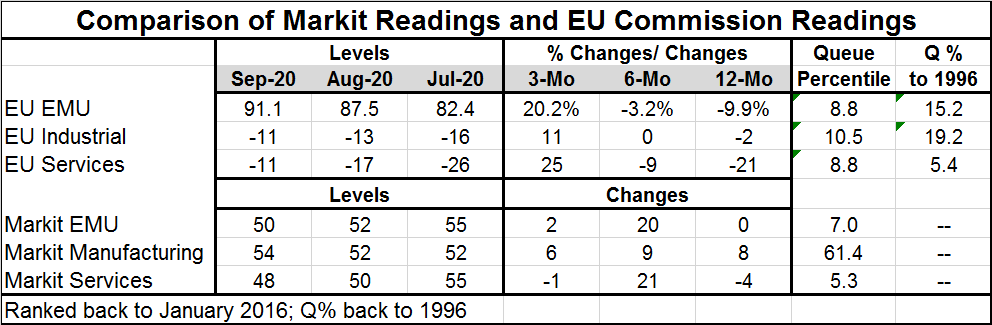

Markit vs. EU Indexes- The table below compares the signals for the overall economy, for manufacturing or industry and for the services sector between the Markit and the EU frameworks. For the most part, the two surveys show the same big picture assessments. Both have the overall economy assessed below its 10th percentile on data from 2016 onward. Both have the services sector in that same weak ranking cohort. But the Markit survey has much more strength in manufacturing compared to the EU assessment of industry. And while the Markit framework has the diffusion index for manufacturing higher by 8 diffusion points over 12 months, the EMU indexes see industry weaker by 2 points over 12 months. The EU services gauge is much weaker over 12 months than is the Markit services gauge. However, the EU framework is showing strong momentum over three months in both sectors. On balance, these reports that purport to survey the same things will always show some differences due to coverage, methodology and sampling. This month the two gauges seem to be roughly showing the same assessments at least as far as policymakers would be concerned. There is some significant difference of opinion on the state and performance of the manufacturing/industrial sector, however.

Sum Up- The EU indexes each month give us an early snapshot for the month ahead of other more conventional data points. Still, diffusion data are not accounting data and we must always use caution in interpreting their signal. Formally diffusion measures breadth not strength although we infer one from the other. While recovery still seems to be in gear, there are new virus issues in Europe and also spreading in the U.S. It is not clear if it is a step backward in progress or a real second wave. And it is coming just as the conventional flu season arrives. That timing will further complicated any ability to create quick and easy diagnoses of the virus. And that could further impede growth going forward.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief