Global| May 29 2008

Global| May 29 2008EU Index is Still Sinking Fast…Inflation in EMU Still High

Summary

The EU overall sentiment reading fell to 96.7 in May from 98 in April. The EMU area’s overall index was unchanged in the month. For the EU area, the industrial sector continues to be the relative strongest. We gauge this NOT from the [...]

The EU overall sentiment reading fell to 96.7 in May from 98

in April. The EMU area’s overall index was unchanged in the month. For

the EU area, the industrial sector continues to be the relative

strongest. We gauge this NOT from the absolute index value for the

month but from its ranking for the month within its own range (see

percentile or rank column). The industrial sector has a raw reading of

-3 but a range percentile standing of 70.6 percent. In contrast the

services sector has a stronger looking +6 raw reading, but that reading

resides in the bottom 30 percentile of its range. Since sectors have

different intrinsic averages and volatility we view the percentiles as

a superior way to assess the readings across the various measures.

Comparisons to the mean also makes this clear since the service sector

mean is +16 compared to its current reading of +6 while for the

industrial sector the average reading is -7 and the current reading is

-3.

Retail and construction sectors are in moderately good shape

at the border of the top third of their respective ranges, consumer

confidence is quite weak residing in the 44th percentile of its range.

Country indices are uniformly lower, with Germany having the

relative best reading of this group in the 65th percentile of its range

followed by France in the 60th percentile of its range. Italy is in the

47th percentile of its range, even with the sharp jump in its sentiment

index this month. Spain is in the 25th percentile of its range and the

UK, a large EU (not EMU) member, stands in the 44th percentile of its

range.

The components readings: The EU/EMU region is still having

some difficulty. The EMU sentiment indicator stalled this month but the

EU measure continued to fall at a fairly rapid pace. The service sector

has been moving sideways for several months, while consumer sentiment,

having steadied in earlier months, fell sharply in May, amid some very

weak component readings. For industry, confidence has stayed aloft

while most components are showing decay. The production expectation

reading is the weakest relative component in the industrial sector

survey. Retailing shows encroaching weakness in employment expectations

and in orders placed. For services all of the main components are

around the bottom third of their respective ranges. Construction is a

relatively solid sector with firm component readings in the top third

of their respective ranges. While the industrial sector has the highest

range readings its components look weaker. Time will tell how ell

Europe holds up as the strong euro continues to take a toll along with

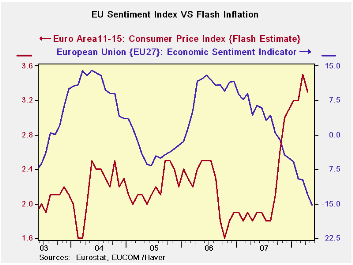

ebbing financial distress and a weakening global environment.

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | May 08 |

Apr 08 |

Mar 08 |

Feb 08 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/ Overall |

| Overall | 96.7 | 98 | 101.9 | 100.3 | 54.7 | 132 | 116 | 73 | 43 | 100 | 1.00 |

| Industrial | -3 | -2 | 0 | 0 | 70.6 | 72 | 7 | -27 | 34 | -7 | 0.87 |

| Consumer Confidence | -14 | -12 | -11 | -11 | 44.8 | 149 | 2 | -27 | 29 | -10 | 0.83 |

| Retail | -3 | -6 | 1 | 1 | 66.7 | 48 | 6 | -21 | 27 | -6 | 0.47 |

| Construction | -12 | -11 | -9 | -7 | 66.7 | 83 | 3 | -42 | 45 | -17 | 0.42 |

| Services | 6 | 6 | 11 | 6 | 31.6 | 104 | 32 | -6 | 38 | 16 | 0.81 |

| % m/m | May 08 |

Based

on Level |

Level | ||||||||

| EMU | 0.0% | -2.5% | -0.6% | 97.1 | 54.6 | 123 | 117 | 73 | 44 | 99 | 0.95 |

| Germany | 0.2% | -1.2% | 0.3% | 103.0 | 65.1 | 83 | 116 | 79 | 37 | 99 | 0.73 |

| France | -3.2% | -2.4% | 0.0% | 99.8 | 60.0 | 120 | 119 | 72 | 47 | 100 | 0.79 |

| Italy | 3.3% | -1.7% | -1.3% | 95.1 | 47.6 | 144 | 121 | 71 | 50 | 100 | 0.79 |

| Spain | -1.1% | -3.8% | -4.1% | 79.8 | 25.5 | 194 | 118 | 67 | 51 | 100 | 0.62 |

| Memo:UK | -5.4% | -8.5% | 10.7% | 90.6 | 44.2 | 179 | 118 | 69 | 50 | 101 | 0.44 |

| Since 1990 except Services (Oct 1996) 208 - Count | Services: | 126 -Count | |||||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief