Global| Mar 27 2013

Global| Mar 27 2013EU Index Drops Off in March

Summary

The EU Commission index for the European Union fell from a level of 92 in February to 91.4 in March 2013. The industrial sector index fell to a net reading of -11.8 from -10.9. Consumer confidence was unchanged at -21.6. The retailing [...]

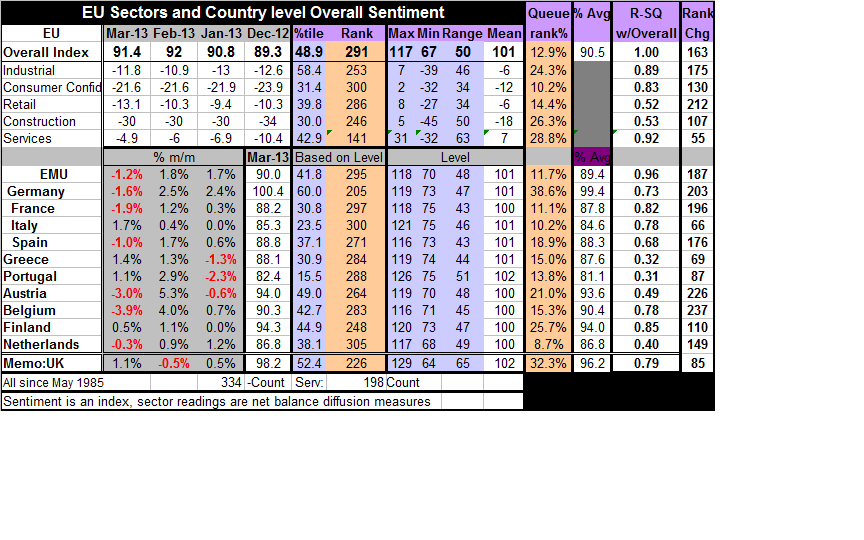

The EU Commission index for the European Union fell from a level of 92 in February to 91.4 in March 2013. The industrial sector index fell to a net reading of -11.8 from -10.9. Consumer confidence was unchanged at -21.6. The retailing index slipped -13.1 from -10.3. The construction index remained steady at -30. Services index improved to -4.9 in March from -6 in February.

The EU Commission index for the European Union fell from a level of 92 in February to 91.4 in March 2013. The industrial sector index fell to a net reading of -11.8 from -10.9. Consumer confidence was unchanged at -21.6. The retailing index slipped -13.1 from -10.3. The construction index remained steady at -30. Services index improved to -4.9 in March from -6 in February.

Despite months of setback, improvement seems still in gear - The chart shows that there has been an ongoing improvement in the EMU and across large countries over the past several months. March has brought a setback to that progress. Even so, the March setback leaves the uptrend intact. But the recession was severe and the overall bounce back with all of its twists and turns continues to leave the European Monetary Union and their members in very weak territory. For the European Union, the overall index resides in the lower 12.9% of its historic queue of values. The index for the European Monetary Union is only slightly better in the 11.7 percentile of its historic queue. By industry, the European Union is weakest for consumer confidence which resides in its lower 10th percentile; retailing resides in its lower 14th percentile; its industrial sector resides in its lower 24th percentile; construction resides in its lower 26th percentile; and, the services sector stands in its lower 28th percentile. These are uniformly weak standings. These ranking or queue percentile readings tell you how often various indices have been lower than what they are now. At 12.9% for the overall queue standing, the European Union has had weaker readings in this about 13% of the time.

Shifting fortunes in the Zone - Looking at reporting EMU members, there are some considerable variations as to where these nations stand in their individual queues. Germany stands tallest in the 38th percentile of its historic queue followed by Finland at the 25th percentile and Austria in its 21st percentile. On the weaker side of the scale, the Netherlands is now the weakest in its historic queue in its 8.7th percentile. Greece has moved up to the 15th percentile, Portugal has moved up to the 13.8th percentile. Among countries that are larger and have been stronger, we see the effects of the crisis spreading to the core of the monetary union. France has slipped to the 11.1 percentile mark of its queue. Italy has slipped to the 10.2 percentile mark of its queue. Clearly weakness permeates the European Monetary Union. Even its strongest member, Germany, stands in a relatively weak position when measured against its historic profile.

No sign of impact from Cyprus - These are readings for the month of March, the Cyprus bank closings occurred on March 15. The early days of the bank closing were regarded as a kind of garden-variety set of bank closings that have been long expected. It's hard to say how much of the Cyprus crisis is reflected in the EU indices and survey for March. As time went on, the situation in Cyprus began to look stickier and uglier and the policymakers' fumbling became more bumbling. Next month, by the time we get the readings for April, we will put much of this behind us and we will be seeing reactions to the crisis in its aftermath and the quality of the post crisis resolution European policymakers have been able to achieve.

Consumer sentiment - The consumer sentiment numbers, which were unchanged overall in March, do not show much evidence that the Cyprus showdown had any impact on consumers and leads us to wonder if the effects of the crisis were recaptured at all in this month's survey. Not only is the overall indicator unchanged, but across the various components there are very, very few changes from February to March. Even looking at the country indicators of the seven countries that we track monthly, only one - Portugal - saw a change of more than one point in its confidence reading on the month. Portugal's consumer confidence reading slipped to -56 in March from -53 in February and at that reading it remains extremely low in its historic queue in the bottom 4% of its range. Looking at the retailing sector, another consumer-sensitive sector, the results appear to be driving more from individual country differences. Retailing slipped in the European monetary union to -18 from -16. The expected business situation slipped to -16 in March form -13 in February. Orders-placed slipped back to -21 in March from -19 February but are still slightly elevated compared of the -22 level in January 2013. Nothing very dramatic is going on in the overall retailing gauge. By country though we see that France has slipped to -20 in March from -17 in February compared to a -15 reading back in December. This in accord with the ongoing and escalated slippage we've seen in other French measures. The UK has slipped sharply from February to March to a reading of -2 from a reading of +7. However, in March Greece has made a rather substantial improvement to a level of -26 from -33 in February. EMU circumstances and responses to stimuli remains mixed.

The service sector slips in EMU - The services sector in the European Monetary Union slipped to -7 from a -5. That's contrary to the sector's improvement for the economic union as a whole. Current demand slipped by one point in March to -8 from -7. Expected demand slipped by four points to a reading of -2 from a reading of +2. However, there was an improvement in current employment from February's -5 to its March standing of -3. Compared to December levels all the categories show that to be an improvement. By country Germany, France and Spain all slipped on the month. Improving were Italy, the UK, Greece and Portugal. Italy improved rather sharply to a reading of -16 in March from a reading of -20 in February. The UK generated a sharp improvement to a reading of minus 2, from a reading of -12 in February. Compared to December levels only France and Spain have deteriorated. Compared to December levels the UK has made an enormous move upward to a level of -2 in March from -23 in December. Italy has made substantial improvement to a level of -16 from a level of -22 in December. Germany has risen to +16 in March from a net of +10 in December. The service sectors in France and in Portugal are the lowest relative rankings, with France in the lower 5% of its queue and Portugal in the lower 6.7% of its queue.

Where to now/next? The evidence continues to show us that the US leads the European business cycle. US industrial gauges have continued to turn up even in the face of the recent softening of the European measures and in global demand/output generally. Cyprus of course is a wildcard for the outlook, not because of its intrinsic worth, certainly (!), but because of the European policy bungling during the crisis and what that might portend for other EMU members as they might seek help in the future. Not to be forgotten is Italy whose elections have yet to produce a government and where renewed efforts to secure a new government appeared to continue to fall short. Italy is the country of the Treaty of Rome which got the European ball rolling. It is the third-largest country in the Union and its newest and fastest-growing political party, one with increasing political punch, is seeking a referendum on the continued use of the euro. It is hard for me to understand how the events in Cyprus trump the effects in Italy but they do. The Cypriot crisis is the stuff that tabloids love - and TV. There are people standing in line, they brandish colorful placards, there is graffiti, there is chanting... There is a Parliament that doesn't seem to know its butt from its elbow, and there are bad guys that might be getting bailed out, the Russians (or have they already left?).

Italy read all about it - if you DARE! While Italy's Grillo and his Five-Star Movement are also good press and theater, it is not in the limelight in Italy at the moment. There, the process moves at a speed that is somewhere between that of a glacier and that of a snail. The financial press is not good at time-lapse photography. And, at that, the maneuvering goes on behind closed doors. But just because the situation in Italy is not as colorful or as media-friendly or as fast-paced, that does not make it less important. The fact that the Italian people support this new movement, the fact that there is grassroots opposition that is questioning -demanding to change- the ongoing grip of austerity, and that this movement raises the possibly of ending the use of the euro and therefore of ending euro membership all make Italy the center-ring of any three-ring (or greater number of rings) in any EU circus. Those seeking entertainment read about Cyprus. Those seeking to be informed about the future of Europe read about Italy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief