Global| Apr 29 2013

Global| Apr 29 2013EU/EMU Economic Sentiment Drops: What's Next?

Summary

Indices of economic sentiment from the European Commission show declines for the Economic Union (EU) and for the European Monetary Union (EMU) for April. The overall EMU index has fallen for the third month in a row, as has the index [...]

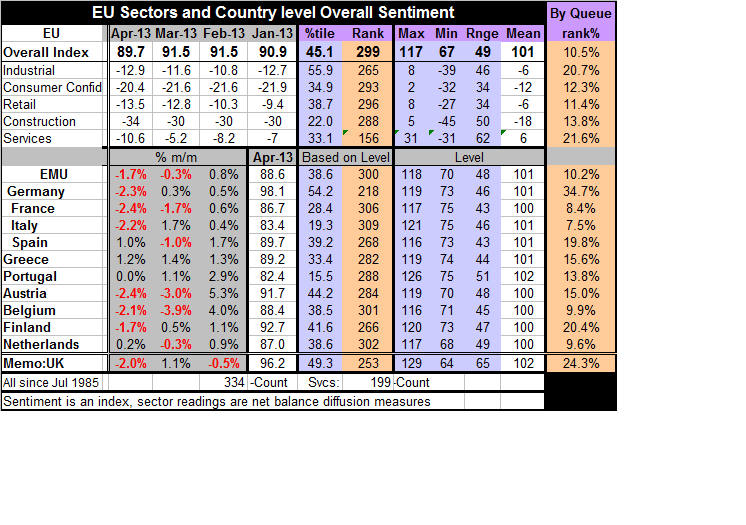

Indices of economic sentiment from the European Commission show declines for the Economic Union (EU) and for the European Monetary Union (EMU) for April. The overall EMU index has fallen for the third month in a row, as has the index for the Monetary Union. The current level of the EU index puts it along with the EMU index in the lower 10th percentile of its historic queue since 1985. That ranking covers a period from before the formation of the Monetary Union and includes the appropriate data assembled and weighted to mimic the current monetary union for the five years previously.

Indices of economic sentiment from the European Commission show declines for the Economic Union (EU) and for the European Monetary Union (EMU) for April. The overall EMU index has fallen for the third month in a row, as has the index for the Monetary Union. The current level of the EU index puts it along with the EMU index in the lower 10th percentile of its historic queue since 1985. That ranking covers a period from before the formation of the Monetary Union and includes the appropriate data assembled and weighted to mimic the current monetary union for the five years previously.

Weakness has rotated to some extent from the peripheral countries into the core countries as we find that the countries that ranked lowest in their historic queue of values now are Italy at 7.5%, France at 8.4%, Belgium at 9.9%, and the Netherlands, which resides in the lower 9.6 percentile of its historic queue.

It's not really that the peripheral countries have the been in trouble are doing that much better, but that in fact they have in this cycle carved out much lower lows from which they had made some rebound so that now the relative rankings are not quite so low for them; they experienced substantially weaker numbers already in this cycle. For example, Spain does still reside in the lower 19 percentile of its queue Greece is in the lower 50th percentile of its queue and Portugal in the lower 13th percentile of its queue.

In addition to these metrics there is a report on Europe form the Conference Board that shows that its leading economic index is fading, pointing to further challenges for Europe in the months ahead.

If we look at the sectors from the Economic Union's perspective we don't find anything that is very strong; the best queue standings among the various sector readings are from industrial sector in the 20th percentile and the services sector in the 21st percentile. After those we have the construction sector in the 13th percentile, consumer confidence in the 12 percentile, and the retail sector in the 11th percentile. All of these are very weak. Interestingly the overall sentiment index when placed in its historic queue is actually weaker than any of the components when placed in their respective historic queues. What this tells us is that not only are the sector rankings low, but the confluence of having all this weakness at the same time is unusual.

But there are also straws of change in the wind. It's not clear that there is a mandate for any change in Germany but the EU Social Affairs Commissioner, Laszlo Andor, is arguing that Germany must raise its wages and must move away from its economic model of export led growth. In a world where so many countries are so indebted it's obvious that export led growth strategies are going to put exporting nations in conflict with their neighbors. To be a consistent exporting nation you must consistently be at the top of the heap in terms of competiveness and productivity, innovation and the like. This is exactly what Germany did. And it means keeping fell EMU members at a lower level in terms of those metrics. This conflict, inherent in an export-led growth model, is already a major factor behind the shifts that we see in China. In another e-zone change that may only be temporary, Italy has seen a new government introduced. It's not clear that this government will be independent or will have any staying power. The people in Italy have spoken and they are against austerity. However the ECB has spoken and any country that does not hold the line of austerity, no longer gets support from its banking sector in the form of LTRO loans. Italy having a government only means that Italy now has somebody who is ostensibly in charge who can make a decision on this difficult impasse.

EMU sectors The industrial readings across the large EMU nations Germany, France, Italy, Spain and the UK show month-to-month deterioration everyplace except in the UK where the index was stable month-to-month at a reading of -8.

Consumer confidence is the lone sector that improved in both EU and in EMU. It improved in four of the five largest EMU economies with Germany being the exception, holding confidence flat at a reading of -5 in both March and April. Countries with month-to-month improvement showed small improvements; Spain logged the largest month-to-month gain with its index improving by three points to -29 from -32.

The retail sector in EMU saw improvements in three of the major five countries. Spain's reading improved the most, moving up to -14 from -18; it was joined by minor increases of one point in Italy and in the UK. However, the two largest countries saw more substantial drops where the Germany index dropped to -14 in April from -11 in March and France's reading dropped to -21 in April from a level of -18 in March. If we look at the changes over a broader horizon since January the only two countries in the retail sector have done better: they are Italy and Spain.

The service sector, an important sector in the EMU economy, took a strong step lower as the reading in April dropped to -11 from a reading of -7 in March. The -11 reading is the weakest since November and it compares to a weakest reading in this recovery cycle of -13, as of September 2012. Those readings compare to a financial crisis low of -26 in March 2009. The service sector readings have been quite rocky and volatile. This month the German index fell very sharply to a reading of +4 from +14 in March but Germany's March reading had showed a sharp increase to 14 from 8.8 in February. France has shown more consistent slippage with its index for April slipping to -15.8 from -14.7 in March Italy which has had readings in the -20 category more steadily improved to -16.4 in March and now it's back down to -23.6 in April. Spain's reading of -22.3 in April as much better than its -30.0 reading in March which brought it to a new local recovery low. Its current reading of -22.3 is generally better than readings have been since about August of last year. The trends for services, while still fairly herky-jerky, look a little more like a failed recovery in progress except for the UK where even with the month's setback there seems to be some improvement in train.

The construction sector deteriorated in all five large EMU economies except Germany where it increased by one point. France and Italy each saw their indices deteriorate by one point. But in Spain the index took a sharp turn lower -56 from -49 and in the UK an even sharper turn lower was taken as index fell to -38 from -27. Spain's reading now sits in the bottom 6% of all of its historic readings; UK reading is in the bottom 25th percentile of its historic queue.

The employment readings from the various reports across the monetary union show generalized deterioration. The industrial sector saw employment expectations fell to -13 in April from -11 in March. Retailing employment expectations fell to -10 from -9. For services current employment fell to -7 in April from -6 in March. Services expected employment fell to -6 in April from -5 in March. The construction sector saw employment expectations fall to -24 from a reading of -22. Despite all of that bearishness about employment, unemployment expectations actually were reduced to a reading of 38 in April from a reading of 42 in March. Employment expectations are the best in the industrial sector where they lie in the 40th percentile of its historic queue. Other sectors' employment readings are roughly the same order of magnitude between the 20th and 25th percentile for current services and services expectations and for expected employment in construction. Employment expectations are the weakest in retailing where they reside in the lower 12 percentile of their historic range. Unemployment expectations from the consumer confidence report lie in the 80 percentile of their range completing a symmetric picture of employment and unemployment expectations..

Conditions in the e-Zone and expected conditions in the e-Zone are weak. While there may be some positive developments on the geopolitical front particularly with a new government in place in Italy, still it's not clear that that's going to change the circumstances or the worries about what happens next there in the months ahead. I suppose with no government in place there wasn't any chance of Italy doing anything and now with the government in place there is some chance of Italy doing something. But beyond that, Zone-wide economic conditions are deteriorating, expectations are worsening, trends are worsening, and along with the EU Commission reading's dismal signal there is the Conference Board's leading index for the region that is sending some warning signals. After some glimmers of hope from some, including ECB head Mario Draghi, early this year, conditions in the euro-Zone and in the EU have clearly deteriorated and now point to more risk.

Ohhh...the ECB might cut rates While some look at this report conclude that it all-but-seals-the-case for an ECB rate cut, I can only wonder why anybody would care about that.

Rate cuts by central banks have the most impact on markets when they have the possibility of putting together a string of cuts rather than providing you one last tiny cut that will have no follow-up. In this environment the ECB cutting rates will be a little bit like the Lone Ranger, surrounded, shooting his last silver bullet. Why would that make you upbeat? Maybe some see it as the ECB engaging in the last bit of conventional easing that it can and paving the way for the ECB to engage in some of the same expansionary hijinks that we've seen in the US and in Japan. Maybe...(which also, wonderfully, means maybe not). The Germans have been very much against any such plan and support a strict adherence to the ECB charter. What the ECB has been able to do is its LTRO lending. Italy's predicament makes it clear what a dangerous and fragile a weapon that can be.

Some are encouraged that austerity is working in Europe and there is no denying it; it surely has been making headway. But my concern is, and always has been, that austerity is just too painful and it takes too long to work. We are starting to see articles written on the 'other costs' of austerity; costs in terms of human suffering, human depression, and even suicides. It's hard for me to see how the little bit of progress that has been made at the cost of so much pain can be viewed as "progress."

John Maynard Keynes when confronted by a person noting that Keynes had just changed his position on an issue famously said, "When the facts changes, sir, I change my mind. What do you do?' In Europe we have to wonder is this what the leaders expected? Are these the expected facts of austerity? Are these the sufferings that member countries were expected to endure? For how long are they expected to endure them? Do the people in the countries that are suffering agree that they should continue to bear this burden? Can the countries undergoing austerity continue under this plan long enough to adopt truly sustainable notions about public spending and taxes and will this program of austerity really fix the competitiveness differences within EMU? These are the critical questions for monetary union leaders. In the meantime they also have to deal with the road they are on and the fact that the differential suffering within the euro-zone is breeding contempt and animosity. To the extent that austerity is bringing zone members' economic fundamentals closer together, is the relationship between the haves and have-nots in the Eurozone getting to be so bad that even with converging economic performance zone members will not want to be together in a single unit because they won't be able to stand one another? That's another question zone members need to address.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief