Global| Jun 27 2013

Global| Jun 27 2013EU Does Better...Can it Continue?

Summary

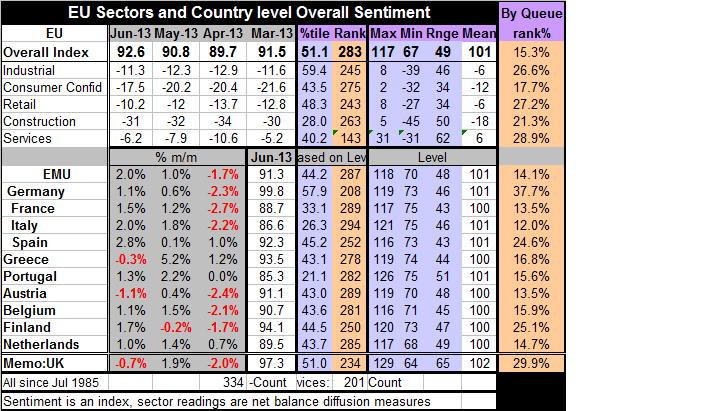

The new overall EU sentiment index for June, at 92.6, is up from 90.8 in May. This is highest level since April 2012, a little more than a year ago. It's good mark but still it continues to be a very, very, low reading. Place this [...]

The new overall EU sentiment index for June, at 92.6, is up from 90.8 in May. This is highest level since April 2012, a little more than a year ago. It's good mark but still it continues to be a very, very, low reading. Place this June reading in the historic context of its queue of values and a 92.6 reading for June 2013 ranks in the lower 15% of its history meaning it has been weaker than this only 15% of the time. This is still an exceptionally low reading for economic sentiment. I suppose if you're looking for good news the good news is that the bad news isn't worse, but this isn't particularly good news

The new overall EU sentiment index for June, at 92.6, is up from 90.8 in May. This is highest level since April 2012, a little more than a year ago. It's good mark but still it continues to be a very, very, low reading. Place this June reading in the historic context of its queue of values and a 92.6 reading for June 2013 ranks in the lower 15% of its history meaning it has been weaker than this only 15% of the time. This is still an exceptionally low reading for economic sentiment. I suppose if you're looking for good news the good news is that the bad news isn't worse, but this isn't particularly good news

Of course, having said that I know that improvement will come one step at a time and that the steps may not be large and may not be monotonic- but that too is part of the point. We need to understand what this process is and to recognize that the risk of backsliding may dog this recovery for some time and may require near constant vigilance.

The reading for industry improved by one point, from -12.3 in May 2013 to -11.3, in June. At this level the industrial sector is in the lower 26 percentile of its historic queue roughly a bottom quarter of the range reading.

Consumer confidence improved to -17.5 from -20.2. Consumer confidence occupies a -17th percentile standing in its historic queue.

For the retailing index, an improvement to -10.2 in June was recognized from -12 in May. This is a modest 27th percentile standing in its historic queue.

The construction sector improved to -31 from -32; its standing is in the 21st percentile of its historic queue.

The services index improved to -6.2 in June from -7.9 in May as the standing rose to the 28th - nearly the 29th - percentile of its historic queue.

While these are improvements, they are not improvements to very strong positions. The chart makes it clear that there is a turn of some sort in train but it's also clear that it's very slow-moving and because of the short-term nature the chart doesn't give you any idea how weak things still are. But you get that information in the table by looking at the percentile rankings.

Let's look at the circumstances of countries: we Chronicle 10 members of the common currency union plus the UK in the table at hand. In the month there are declines for overall sentiment only in Greece, in the UK and in Austria. If we look to the percentile standings of the countries we find that Germany has the strongest percentile standing in the 37th percentile of its historic queue followed by the UK in nearly the 30th percentile followed by Finland and the 25th percentile and Spain in its 25th percentile. These are the 'best of the best' and the readings all are still trapped below the 50th percentile and even though these are the top four nations their standings reach down to the top of the lower 25th percentile. The 'best rating is not even to the 40th percentile let alone the break-even mark of the 50th percentile.

After that, counting up from the bottom, the weakest is Italy in the bottom 12 percentile of its historic queue, after that there's a tie the 13.2 percentile between Austria and France just above them is the Netherlands in the 14.7 percentile and so on.

While we see improvement in the zone we don't see very strong improvement. Still the gains are relatively broad-based with seven of the 10 common currency members in the table showing consecutive monthly gains in their respective sentiment indices, and with Portugal and Spain and the Netherlands showing three months without a setback. There certainly is some good news in the euro-Zone.

But the bank bail-in bill that has been approved clearly is something that is going to overhang market and although there is no adverse market reaction today. It seems to build on the Cyprus model which we were told at the time would not be a framework for any future banking assistance. Never mind.

Eurozone ministers renewed their failed declaration of a year ago to make progress on reducing high unemployment levels in the Zone. And once again they have given us an objective without a means to reach it.

The BIS continues to see austerity is the answer and a little austerity as the reason that things have gone wrong. While it's easy to look back in history and the say there has been too much borrowing the and therefore not enough austerity in Europe or in the United States, the pressing question is what to do about it now. While there seems to be some renewed interest in pursuing more of a growth strategy, there is no interest in throwing out the austerity gains the with the bathwater. However, it's completely unclear how countries are going to be able to proceed to pursue greater growth in an environment where they are going to have to be mindful to hang on to gains that they have made under austerity. As always it sounds better as rhetoric than it will play out as policy.

Quite apart from pulling a rabbit out of their hats euro-Zone countries continues to have conflicting goals and constraints that are all too binding. While the Zone has been able to come together to have some degree of a banking 'bail-in' plan, because of its restrictions is not clear whether it will be useful, particularly for any of the banking systems in southern Europe.

There is some sense of progress in the euro-Zone. However, there are still big question marks as to the speed for that progress into its durability. While it's not part of the euro-Zone issue is no doubt that the backsliding and sense of risk in China is simply another risk element that the euro-Zone is going to have to deal with. At the moment I don't see any positive bandwagon to jump upon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief