Global| Mar 27 2018

Global| Mar 27 2018EU Commission Indexes for EMU Fall Again; What Is the Message Here?

Summary

EU Commission indexes for the EMU area turned down broadly, falling for the straight third month. The five sector indexes saw declines in three sectors (industrial, retail, and services), a gain in one (construction), and unchanged [...]

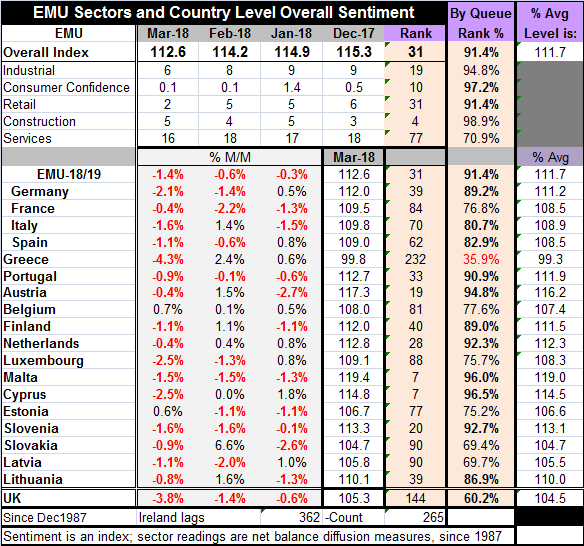

EU Commission indexes for the EMU area turned down broadly, falling for the straight third month. The five sector indexes saw declines in three sectors (industrial, retail, and services), a gain in one (construction), and unchanged conditions for consumer confidence. The overall index fell to 112.6 in March from 114.2 in February. The overall index was last lower in August of last year.

EU Commission indexes for the EMU area turned down broadly, falling for the straight third month. The five sector indexes saw declines in three sectors (industrial, retail, and services), a gain in one (construction), and unchanged conditions for consumer confidence. The overall index fell to 112.6 in March from 114.2 in February. The overall index was last lower in August of last year.

Eighteen of the 19 EMU members report these indexes in a timely fashion. Of those 18 all indexes fell in March except for Belgium and Estonia. Nine of 18 indexes fell in February. France, Portugal, Malta and Slovenia report three declines in a row.

However, the sector standings of index levels are still strong with the overall EMU reading and all sectors except services on a 90th percentile or higher standing. The services sector, however, has only a 70.9 percentile standing. The sectors are generally back to their August-September values with the run up to a peak around December now a thing of the past.

The country-by-country tabulation finds seven of nineteen with standings in their respective 90th percentiles, five in their 80th percentiles, four in their 70th percentiles, and two in their upper 60th percentiles. And then there is Greece with a 35.9 percentile standing.

Greece is the only member with an index level below its historic average, at 99.3% of its average. The EMU gauge is standing 11.7 percentage points above its average.

A closer look at some sectors

The industry gauge is strong on very strong components readings for order volume, the production trend, employment expectations and export orders. However, production expectations are bit less ebullient and selling price expectations, with a 70th percentile standing, are moderate. Among the Big-Four economies industrial sector readings have a 90th percentile standing in Germany, an 83rd percentile standing in Spain, a more modest standing of 81st percentile in Italy, and a 77th percentile in France.

Consumer confidence is exceptional in the EMU especially given the momentum backtracking and political conflicts boiling in Germany, Spain and Italy. Nonetheless, the economic situation over the next 12 months has a very strong standing as does the situation over the past 12 months. The environment to make major purchases is very strong; expectations are for it to stay that way with little slippage. Expected price trends are modest with a 66th percentile standing.

The services sector has a weaker standing with weakness emanating from expected demand that has only a 64.9 percentile standing. Germany’s services sector and France’s services sector have only 66th percentile standings. The standing for Italy is in its 86th percentile and for Spain it is in its 71st percentile.

On balance, the EMU is doing well, with only one country reporting weaker than average conditions and most with standings in the upper 60th percentile or much higher. But momentum is being lost and it is hard to gauge the degree of slippage. The EU Commission indexes continue to track the Markit PMI gauges closely.

Undercutting or underpinning policy?

With central banks poised to transition to or toward normalcy and with the Fed in the U.S. now well along that path, the fading growth in real money balances is not a phenomenon that clearly supports these policies. In the U.S., credit growth also has become and remained quite weak. Inflation globally and in all major markets (except the U.K.) is undershooting. Yet, central bankers are fixated on raising the level of rates back toward normalcy. Not only are stock markets unstable largely from unrelated policies and concerns over trade policies, but the erosion of momentum in such things as the EU Commission indexes in Europe, and in the UK, the loss of momentum in global money growth rates, and weak readings in the GDP-now-casts in the U.S., all do the equivalent of raising their eyebrows not just on Fed policy in the U.S. but on the degree of unanimity there seems to be on the need to return to normal... and to do so now. But the question remains: how can you get back to normal when you do not know where the new normal is? Oh, don’t bother you with such details? Then never mind.

Monetary Trends Also Decay

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief