Global| Feb 25 2021

Global| Feb 25 2021EU Commission Indexes Coalesce Well Short of Normalcy

Summary

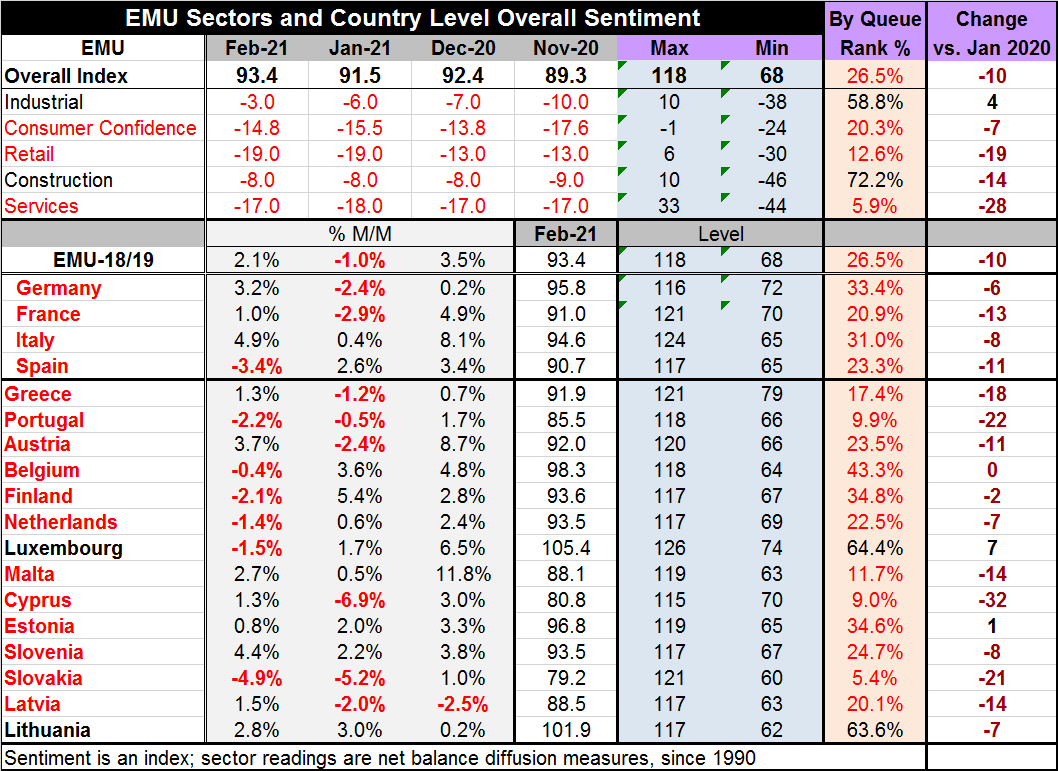

The EU Commission Index for the EMU shows an improvement to 93.4 in February from 91.5 in January putting the index back on the rise after a month in which the index fell. Ranking the current value on the index in a queue of its [...]

The EU Commission Index for the EMU shows an improvement to 93.4 in February from 91.5 in January putting the index back on the rise after a month in which the index fell. Ranking the current value on the index in a queue of its observations back to January 1990 leaves the current reading in the 26.5 percentile-right at the border of the bottom one-quarter of its historic values. The EMU index has been stronger than it is in February about three-quarters of time.

The EU Commission Index for the EMU shows an improvement to 93.4 in February from 91.5 in January putting the index back on the rise after a month in which the index fell. Ranking the current value on the index in a queue of its observations back to January 1990 leaves the current reading in the 26.5 percentile-right at the border of the bottom one-quarter of its historic values. The EMU index has been stronger than it is in February about three-quarters of time.

The EMU index was briefly as weak at 67.8 (in April 2020) in this cycle. Then it climbed quickly to a reading in the 80s (by July 2020) then progressed to a reading in the 90s (September 2020), but it has had a hard time advancing steadily since then. In November, for example, the EMU index drifted back into the upper 80s (89.3). The reason, of course, is the virus spread then was diminished then it came back strong. These reinfection cycles set back the economy despite the fact that countries have learned a lot about how to deal with the virus. On the other hand, a lot of people have lost the will to continue to isolate, wear masks and do the things that make containment work. Of course, now there is more infection around (more natural herd immunity too) and the program of vaccinations is moving ahead to create more immunity. But the vaccine rollouts have been slower than desired.

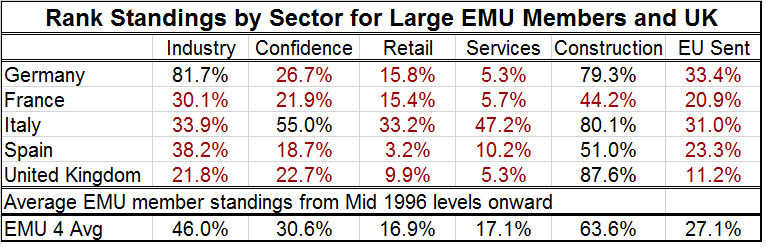

Table Rank Standings by Sector shows sector indexes for the largest European economies. Four are EMU members. There are several generalizations. (1) Construction tends to be the strongest sector in each country (Germany is an exception). (2) Services tend to be the weakest sector (Italy is an exception). (3) France has the strongest nothing nor the weakest anything. (4) The United Kingdom is at or near the bottom of every category except construction where its ranking for that industry is the highest. But the U.K. is clearly struggling fighting off the virus, being the center for a new more highly contagious and a more lethal strain of the virus as well as dealing with Brexit. The U.K. has the lowest EU Commission sentiment reading of any country; within the EMU the weakest is France although the EMU country standings are all quite similar on a range from 20.9% to 33.4%.

The data for the EMU in February show seven out of 18 countries weaker month-to-month; nine had weakened in January.

The country level percentile queue standings show only two with standings above their historic median (above a standing of 50%). There are three countries in single digit standings, two with standings in the ‘teens,’ six with standings in their 20th percentile decile, four with standings in the 30th percentile decile and one in the fortieth percentile decile. There clearly is a lot of weakness yet in the EMU.

Still, the clear trend is to improvement. Only three countries Slovakia, Cypress and Portugal fail to make EU Commission Index gains over three months. Over six months add France and Slovenia to that list as five (out of 18) countries are weaker on balance over six months. At the other extreme only Luxembourg is higher on balance over 12 months.

By component, only the industrial sector is higher over 12 months, six months and three months. Only retailing is lower over 12 months, lower over six months and lower over three-months. The services sector is flat over three months and over six months. Consumer confidence is up over three months but lower on balance over six months. Construction is higher over six months and stronger over three months as well.

Since January of last year when the virus struck, all countries except two (Luxembourg and Lithuania) are weaker on balance in terms of the value of their EU index. The weighted EMU index is lower by 10 points and the unweighted average loss across the 18 reporting EMU members is also 10 points weaker.

The data paint a picture of a weak area. While there is recovery taking hold, it is most widely identifiable over three months. At the same time, we know that trends really do not matter because a rise in the virus can quash the strongest trend. Alternatively, the weakest trend can be reversed if the virus becomes contained and an economy throws off the shackles of a lockdown.

There is too much epidemiological whimsy in the air to make any sort of certain statement about the future. We are hopeful that immunity is gaining on the virus fast enough to allow the various service sector firms to reopen. We are hopeful that the process of vaccination will gather pace. We are also hopeful that new strains of the virus will not arise and prove to be vaccine resistant. For once we can say that the future rests far more on the prospects of things we hope for than on things we know or can control.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief