Global| Oct 30 2017

Global| Oct 30 2017EU Commission Indexes Climb But Slow Their Rate of Ascent

Summary

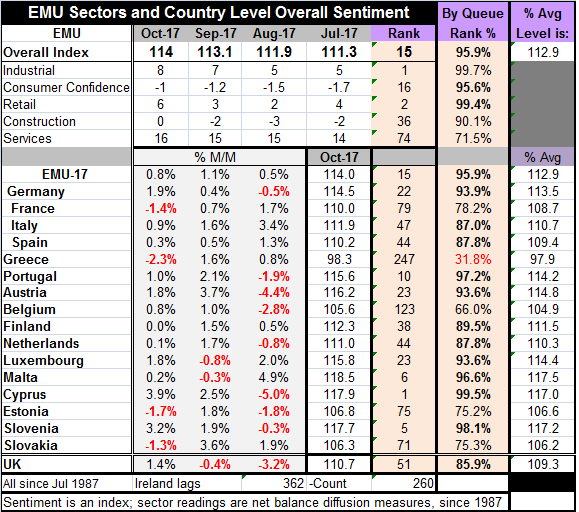

The EU commission indexes are still rising with gains posted in each of the sector or special function indexes in October. Retailing gained three points month-to-month; construction gained two points; the industrial and service [...]

The EU commission indexes are still rising with gains posted in each of the sector or special function indexes in October. Retailing gained three points month-to-month; construction gained two points; the industrial and service sectors each gained one point; and consumer confidence edged up by 0.2 points.

The EU commission indexes are still rising with gains posted in each of the sector or special function indexes in October. Retailing gained three points month-to-month; construction gained two points; the industrial and service sectors each gained one point; and consumer confidence edged up by 0.2 points.

The overall EMU sentiment index now stands in the 95th percentile of its historic queue of data with the industrial reading, the retailing reading and the consumer confidence reading each at a standing of the 95th percentile or better. Construction has a 90th percentile standing. Services post a 71st percentile standing. These rankings tell us, for example, that retailing has been this strong or stronger only 0.6% of the time while the services gauge has been stronger about 29% of the time. These all are impressive readings. And each still has upward momentum as all the indicators are higher on balance over three months.

Turning to country-level data for overall sentiment, we find only four countries out of the early reporting 16 that have backslid in October. The backsliders are Greece, Estonia, France and Slovakia. This is impressive especially after September when only two countries experienced retrograde motion.

Among the 16 early reporters, only five fail to have sentiment standings in the top 20% of their respective historic queues of data back to 1987 (or less for fresher reporters). Only Greece has a standing below its 50th percentile (at its 31st percentile) while the other reporters have standings somewhere in the decile of their respective 70th percentile (except Belgium with a 66th percentile standing).

ECB plans

The ECB has announced its plan to begin to strip off some of the layers of stimulus policy it has been wearing. The Germans want that done faster and markets were somewhat surprised that the ECB's announced policies for stepping back were so muted.

One trick pony

Still, the ECB is a one-trick pony; an inflation targeting central bank and inflation is still well below its target. In data released today, German inflation in October that had been pressing higher backed off. German inflation is up by 1.5% year-on-year while Spain also has reported October inflation that shows a 1.7% gain. For the EMU as a whole, inflation was at 1.8% in September on the headline, but only at 1.2% on the core. Recently, the core has been emphasized because of the temporary and distortive nature of oil price gyrations on the headline.

Central bankers united in their 'unease'

At the ECB, as at the Fed, many policymakers are uncomfortable keeping to their word. Central bankers are wary that they have been too easy for too long and that historically only more inflation has come from that. They want to hike rates regardless of inflation's current reading. That is one reading of history. Another reading that is in the wake of financial crises central bankers have tried to restore rates to their previous normal levels too soon and that has led to backsliding. So where is the ECB and the Fed? Are they too slow too fast or just about right? All of this is a matter of opinion. But as they opine at their respective policy meetings, they have to find a way to make policy that still pays homage to their goals. Draghi, it seems, is doing this albeit under pressure from the Germans and others who seem to tend to view the ECB's 'just less than 2%' objective as a ceiling. The Fed in the U.S. is either doing it or not (depending on your perspective) by using a forward-looking inflation forecasts and saying it 'assesses' inflation in the medium term. Of course, that was the reason/excuse for the December 2015 rate rise and as of today (new PCE report) the core inflation stayed at 1.3% in October where it has been for two months running and apart from these two months you have to go back to 2015 to find inflation at this level and back to 2007 to find it lower. The approach reminds me less of Paul Revere and his 'The British are coming' forecast than of the comedian Johnathon Winters' farce 'The Russians Are Coming.'

Reverse exorcism?

Central bankers are on the horns of a dilemma. Their usual 'charge' is to fight inflation to attain price stability. They are extremely uncomfortable that the definition of price stability they adopted and that is implied by their target now requires that they encourage some inflation. They act almost as if they were priests who you'd asked to do a reverse exorcism. Not surprisingly, central banking policymakers are having a tough time with this prescription and an even tougher time since they have looked closely at the medicine and have found their own names on the label as the prescribers.

The road ahead

Global economic conditions are improving and that has central bankers wary again. But forecasts are just barley edging up. No forecaster is boldly marking up growth rates by one half a percentage point or by a full percentage point. We are talking technical ticky-tacky 'send-a-signal' forecast increases. And while some geopolitical events have flared, populist tendencies across Europe have blown the U.K. out of the EU and sent the Catalonians into separatist fever. Merkel has lost some of her grip on policy in Germany. Yet, consumers still seem nonplused and positive. Global tensions remain high in the Middle East in Afghanistan and there are special high tensions surrounding events in Iran and North Korea. And after its five-year party Congress, China seems like a less friendly place with which we share any values at all. For the time being, a view of optimism or denial prevails. It seems likely that there is a lot more risk in events and in the outlook than traditional market-measures would give you partly for that reason. Markets are doing well and are fully priced because fear has been suppressed; also because the alternatives to stocks are so poor. And if central banks move rates up more aggressively, they will likely depress long-term rates even more, flattening global yield curves. Markets clearly do not fear or expect inflation. This leaves central bankers in a peculiar spot. It looks a lot like central banker purgatory to me.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.