Global| Feb 27 2014

Global| Feb 27 2014EU and EMU Sentiment Rise in February

Summary

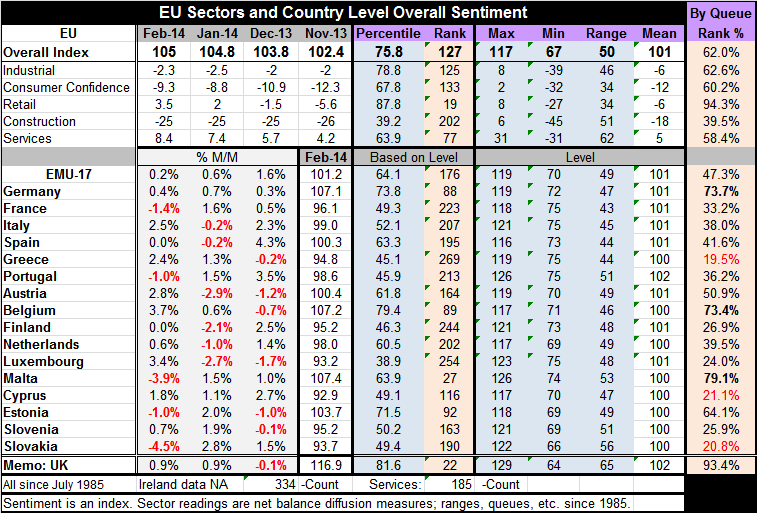

The EMU overall sentiment gauge and the reading on the EU overall rose in February. The sector readings for the whole of the EU show weakening consumer confidence in the month, a flat construction sector and a small rise in the [...]

The EMU overall sentiment gauge and the reading on the EU overall rose in February. The sector readings for the whole of the EU show weakening consumer confidence in the month, a flat construction sector and a small rise in the industrial sector. Retailing and services improved more substantially.

The EMU overall sentiment gauge and the reading on the EU overall rose in February. The sector readings for the whole of the EU show weakening consumer confidence in the month, a flat construction sector and a small rise in the industrial sector. Retailing and services improved more substantially.

Of the 16 members that have reported on this basis, only five of them showed overall sentiment declines in February. The rebound is widespread. Of the 48 various monthly changes for the 17 EMU members and the EMU itself over the past three months, only 17 have showed declines; that is about one-third of the one month changes for this group of eighteen over three months.

We also present the queue standings for the EU's various sectors and for the EMU and its key members. EMU sentiment as a whole stands only in the 47th percentile of its historic queue. For the broader EU, the standing is in the 62nd percentile of its historic queue.

The sectors show raw up-minus down diffusion scores in the table. The raw scores show the strongest raw readings are for services and retail. Next the industrial sector has raw reading of minus 2.3, consumer confidence is at minus 9.3 and construction is at minus 25. However, growth is about changes and this month only consumer confidence backtracked.

The EU region and the sector readings, therefore, are stronger than the EMU readings. The EU sits in the 62nd percentile of its historic range. The EMU indicator sits in the 47th percentile of its range. The EU contains all the countries of EMU and more. Those other countries of the EU are generally stronger than the run-of-the-mill EMU member. One of them is the UK whose values are presented in the table at the bottom.

Another way to understand the current readings is to evaluate them versus their respective historic means. On that basis, irrespective of whether the absolute reading is positive or negative, all EU sectors are above their historic means except construction. However, we can also look at the standing of each indicator in its historic queue, a statistic that speaks a lot more directly to the median, as for each country or sector, the median will lie at the 50% mark of its range by definition.

The EMU countries show stratified rankings. Only 3 countries are in the top 30% of their historic queue while six are in their lower 30th percentile. The average queue ranking of the members in the EMU is the 41.7 percentile. That compares to an EMU statistic of the 47.3 percentile. The EMU-wide figure is a weighted average. It indicates that the larger economies are doing better than the smaller economies. Germany, the largest EMU economy, has a queue ranking in its 73.7 percentile. Malta, a small economy with a shorter data history, is the only country doing relatively better than Germany.

Across EMU expected unemployment is back to a ranking in the 49.4 percentile. Expectations for hiring are getting better; the fastest expected improvement is in the manufacturing sector and next in the retail sector.

In looking at the service sector's queue rankings in February, Germany stands at 69.7% with France at 18.4%, Italy at 35.1% and Spain at 42.2%. Germany lives in a world of its own and its large economic weight tends to dress up the EMU total which, for services, stands at the 39.5% level. You can only imagine how weak other member readings are with Germany pulling such a high weight and having a strong reading to boot. Similarly consumer confidence across countries shows Germany at the 77.3% mark, France at 29.9%, Italy at 36.3% and Spain at 38.2%. Among the large economies, Germany again is in a world of its own. Largely due to the German weight, the EMU standing is at the 52.6 percentile. There is still a lot but not as much divergence for the industrial sector. Still, the German index is at 74.3%, France at 51.0%, Italy at 44.3% and Spain at 43.1%. The EMU metric is at the 65th percentile.

These are only a few samplings of the divergences we see by sector. The table provides a hint of how great the divergences must be if we look at the circumstances of the countries whose aggregate measures are among the worst. And it is not like there are only a few stragglers that are lagging: six of the 16 countries detailed in the table are still in the bottom one-third of their respective historic ranges for economic sentiment.

These divergences are the reason that I remain on guard in evaluating the EMU economy and its prospects. There is so much yet to do and so many risks that are internal to the community and are not addressed by looking at the state of the aggregate, weighted, and anesthetized measures.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief