Global| Jun 27 2014

Global| Jun 27 2014EU and EMU Sentiment Gauges Drop in June

Summary

The EU Commission indices for June 2014 show a slight decline in the reading for the overall European Union (EU) and a slightly larger decline for the countries of the European Monetary Union (EMU). The sector-wide indices for the EU [...]

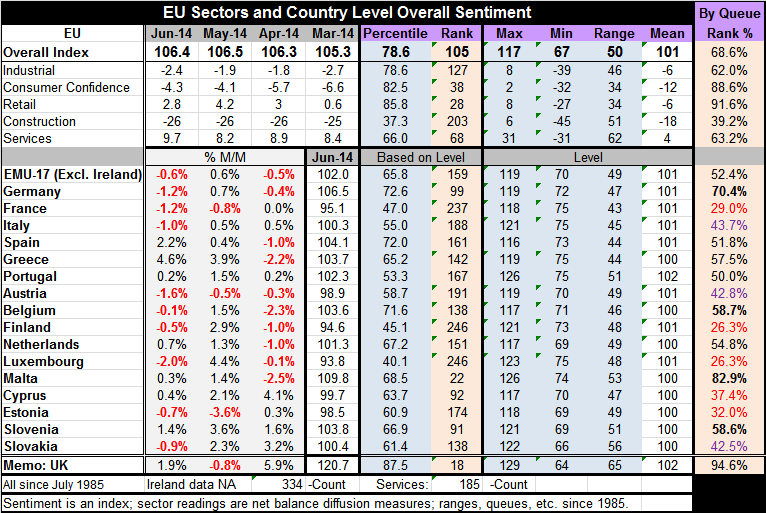

The EU Commission indices for June 2014 show a slight decline in the reading for the overall European Union (EU) and a slightly larger decline for the countries of the European Monetary Union (EMU). The sector-wide indices for the EU show a steeper decline in several sectors. The industrial sector index fell to -2.4 in June from -1.9 in May. There also is a steeper decline in consumer confidence, which fell to -4.3 in June from -4.1 in May. The retail sector shows less strength with a 2.8 reading in June, its weakest level since March 2014, down from 4.2 in May. The construction sector is showing a steady decline with a negative reading of -26 for the last consecutive three months. The services sector advanced; its index rose to 9.7 in June from 8.2 in May.

The EU Commission indices for June 2014 show a slight decline in the reading for the overall European Union (EU) and a slightly larger decline for the countries of the European Monetary Union (EMU). The sector-wide indices for the EU show a steeper decline in several sectors. The industrial sector index fell to -2.4 in June from -1.9 in May. There also is a steeper decline in consumer confidence, which fell to -4.3 in June from -4.1 in May. The retail sector shows less strength with a 2.8 reading in June, its weakest level since March 2014, down from 4.2 in May. The construction sector is showing a steady decline with a negative reading of -26 for the last consecutive three months. The services sector advanced; its index rose to 9.7 in June from 8.2 in May.

The EU indices rank in the top 68th percentile of their historic queue; that is stronger than the EMU reading which is only in its 52nd percentile. The EMU's sentiment index is 1.1% above its average while the EU index is 5.2 percentage points above its average.

Looking at the sector components, the EU's strongest sector is retailing which stands in the 91st percentile of its historic queue. That's followed by consumer confidence, which is in its 88th percentile. After that the services sector lies in its the 63rd percentile; the industrial sector sits at its 67th percentile. The construction sector is in the 39th percentile of its historic queue and remains weak as it has been throughout the recovery.

Turning to the individual EMU members, we see a proliferation of declines in June: 10 of the 16 reporting members showed declines in their sentiment indices in June. That's up sharply from only 3 in March and compares to 10 showing declines in April.

Among the 16 reporting EMU economies, the weakest are Finland and Luxembourg that both sit in the bottom 26th percentile of their historic queues. The next weakest is France in its 29th percentile, then Estonia in its 32nd percentile and Cyprus at its 37th percentile. Slightly stronger are Slovakia and Austria; both of which sit in the 42nd percentile. Italy stands in its 43rd percentile. The strongest country by its queue ranking is Malta in its 82nd percentile. That's followed by Germany in its 70th percentile and Finland in the 58th percentile along with Slovenia in its 58th queue percentile. Slightly below them is Greece at its 57th percentile

Among the four largest EMU economies, Germany, in the 70th queue percentile, is the strongest, followed by Spain in the 51st percentile, Italy in the 43rd percentile and France in its 29th queue percentile. Apart from Germany, the largest EMU economies are not faring particularly well. Germany, with its very large weight, is responsible for the above 50 percentile reading for the EMU as a whole.

Turning to the various sectors for the EMU, we find that industrial confidence sits in its 59th percentile in the EMU. Its strongest components are `production trend' and `export order volume' followed by overall `order volume'. German industrial sentiment is the highest among the big four with its 68th percentile standing. Spain and Italy have rankings slightly below the 50th percentile while France's ranking is only in the 20th percentile.

Confidence at the EMU level stands in its 76th percentile, a relatively elevated reading. However, unemployment expectations picked up slightly to post a raw score of 16 in June, up from 15 in May, elevating it to its 28th percentile. That's too high a percentile to consider things back to normal. By country, consumer confidence is highest among EMU members in Germany, which stands in the 92nd percentile, followed by Spain where it's in the 78th percentile and Italy where confidence is in the 66th percentile. For France confidence is only in the 32nd percentile.

Retailing confidence is high, in its 86th percentile, for EMU members. Here, Spain's assessment is the highest in the 96th percentile, followed by Germany in the 93rd percentile, Italy in the 73rd percentile and France in its 38th percentile.

The services sector was flat at the same reading of 4 over the last three months, leaving the index for EMU in its 42nd percentile. By country, the strongest EMU reading among the big 4 comes in Germany, in the 61st percentile; after that the other three readings are much lower with Spain in the 42nd percentile, Italy in the 35th percentile, and France in the 21st percentile. The services sector, a job sector, simply is lagging well behind the readings of the other sectors in the EMU. France also lags badly by each and every measure.

The construction sector has been lagging throughout the recovery. It slipped to -32 in June from -30 in May. Its rank percentile is only at the 18% level. However, in Germany, the construction sector is in the 88th percentile, followed by Italy in the 35th percentile and France in the 19th percentile. Spain, where the construction sector made a massive flop after overbuilding, has its index in the bottom 2% of its historic queue.

Employment conditions are showing some rebound based on sector rebounds. Employment expectations in the industrial sector stand in the 70th percentile. In retailing, employment expectations are even better, in the 73rd percentile. Current employment in the services sector, which is a lagging sector, stands only in its 40th percentile although expected employment in the services sector stands in its 47th percentile showing some expectation or hope for improvement. The construction sector which continues to lag has employment expectations that are in the lower 17th percentile of its historic queue. Overall expectations for unemployment stand in the 28th percentile and have risen in June compared to May.

On balance, it's a weaker report for the EMU than what was expected. There were setbacks across a wide array of countries including three of the four largest economies in the euro area. Only Spain, among the four largest, showed an advance. The European Central Bank is implementing its new policy to try to stimulate credit growth. In this environment, Italy's official debt continues to be well received in markets even though the quantity of Italian debt continues to grow to spectacular levels.

On the geopolitical front, the EU has just signed a pact with Ukraine, Georgia and Moldova, all former USSR states. This has rankled Russia and caused it to say that it will have serious consequences. These are states that Russia had hoped to pull into its fold or at the least keep them as buffer states between the West and Russia. Putin once said that any attempt to pull Ukraine into the orbit of the West would cause it to divide. But these former Soviet republics now appear to want to move closer to the countries in the West rather than to Russia, despite Russia's recent aggressive behavior. The unrest in Ukraine may already have taken some toll on growth in Europe. These geopolitical elements simply add to the ongoing problems of economic integration and assimilation occurring across Europe. This month, simply put, was not a good month for Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief