Global| Apr 23 2015

Global| Apr 23 2015EMU Upward Momentum Stalls in April

Summary

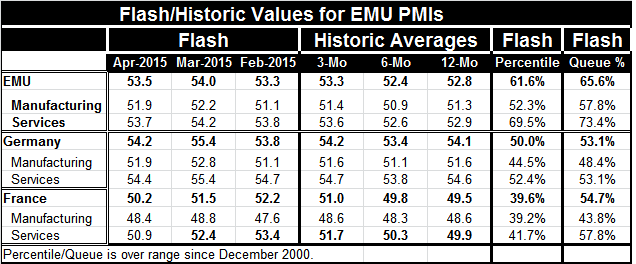

Both the EMU manufacturing and services indices backtracked in April. The overall index fell by one-half point; each component fell by one-half point or less. Yet, for the EMU as a whole, the overall index and each component continue [...]

Both the EMU manufacturing and services indices backtracked in April. The overall index fell by one-half point; each component fell by one-half point or less. Yet, for the EMU as a whole, the overall index and each component continue to reside above their respective three-month averages, indicating that progress may still be in train.

Both the EMU manufacturing and services indices backtracked in April. The overall index fell by one-half point; each component fell by one-half point or less. Yet, for the EMU as a whole, the overall index and each component continue to reside above their respective three-month averages, indicating that progress may still be in train.

However, that is not true for the two biggest EMU economies. For Germany and France, each component is weaker than the month before as for the EMU, but the German and French indices generally still are below their respective three-month averages. To the extent that upward momentum is being maintained, it is through the smaller EMU economies.

The queue standings of the month's indicators continue to be moderate to weak. The queue reading places each monthly diffusion value in a queue of its historic observations expressing the result as a percentile standing in that queue. The best standing among all sectors for the EMU and its two largest economies is for the EMU-wide services sector that stands in its 73rd queue percentile. However, at that level the index is still higher nearly 27% of the time.

The services sector is leading in the EMU, Germany and France. The services sector raw score is higher than its companion manufacturing sector score in each country and region in the table and the queue standings of the services sector are higher as well. All services sectors stand above their 50th queue percentile and that result leaves them above their respective historic medians. But for France and Germany the manufacturing PMIs are below their 50th percentile marks and therefore are below their historic medians. At this point in an economic expansion, that is still extremely weak.

The overall PMI gauges for the EMU, Germany and France are still very moderate. For the EMU, the gauge stands in only its 65th percentile. Germany stands in its 53rd percentile and France in its 54th percentile.

Despite the weak euro, the services sector continues to lead the EMU ahead. The euro has been falling for some time and we might have expected its drop to have ignited growth by this time. And maybe that effect is in train. But for now, we see manufacturing is still lagging and the domestic oriented services sector is leading the EMU ahead. This is also true for Germany, an economy that tends to have export-led growth. The broad euro exchange rate expressed in inflation-adjusted terms has fallen by nearly 14% over the past year. Over the period, the EMU manufacturing sector has continued to be weaker on balance.

At some point, we expect the weaker exchange rate to jump start growth and push the manufacturing sector ahead. But that is not in progress at the moment. As much as there has been optimism about the recent rebound in the European economies - which you can easily see as a rise in the PMI gauges from their recent swale - there is still a lot of work to do. Both sectors have lost momentum and manufacturing remains particularly restrained although it is still largely expanding. At this point in the cycle, the economies of Europe need to go over a higher hurdle than simply expanding; they need to show some strength.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.