Global| Jan 09 2020

Global| Jan 09 2020EMU Unemployment Stabilizes and Divides a Region

Summary

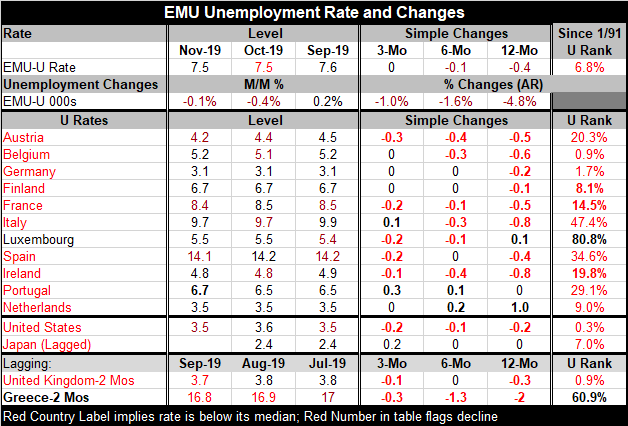

The EMU unemployment rate remains in November at its lowest rate since 2008. On the month, the unemployment rate fell in Austria, France, and Spain. With a lag, the unemployment rate fell in Greece and also in EU member, the United [...]

The EMU unemployment rate remains in November at its lowest rate since 2008. On the month, the unemployment rate fell in Austria, France, and Spain. With a lag, the unemployment rate fell in Greece and also in EU member, the United Kingdom. Over three months unemployment rates (or the lagged rate in the case of Greece) fell in six countries while rising in Italy and Portugal. Over six months unemployment rates fell in seven countries while rising in Portugal and the Netherlands. Over 12 months unemployment rates fell in nine countries while rising in Luxembourg and the Netherlands. On these time lines Germany had no unemployment rate drops over three months or six months and only the second smallest drop over 12 months. Germany often is different.

The EMU unemployment rate remains in November at its lowest rate since 2008. On the month, the unemployment rate fell in Austria, France, and Spain. With a lag, the unemployment rate fell in Greece and also in EU member, the United Kingdom. Over three months unemployment rates (or the lagged rate in the case of Greece) fell in six countries while rising in Italy and Portugal. Over six months unemployment rates fell in seven countries while rising in Portugal and the Netherlands. Over 12 months unemployment rates fell in nine countries while rising in Luxembourg and the Netherlands. On these time lines Germany had no unemployment rate drops over three months or six months and only the second smallest drop over 12 months. Germany often is different.

The EMU-wide rate of unemployment has been lower only about 6.8% of the time since January 1991. Looking across EMU members, only Belgium and Germany have their unemployment rates lower less often (current unemployment rates are exceptionally low there). In that sense, the unemployment rate ranking for the EMU is not really representative of most of the countries of the EMU. Austria, France, Finland and the Netherlands have ranking in a range from 9% to 20%. Ireland, Portugal and Spain have rankings near the 30th percentile mark. Italy ranks just below its median at the 47.4 percentile mark. Luxembourg and Greece have standings still well above their medians at rankings at the 80.8 percentile and the 60.9 percentile, respectively.

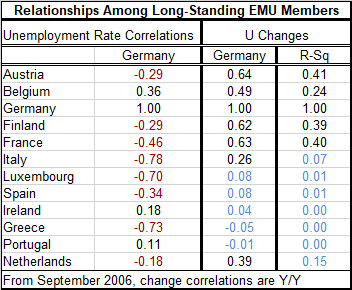

Table "Relationships Among Long-Standing EMU Members" contains correlations run on unemployment levels and on 12-month changes in unemployment levels. The change correlations also are presented as R-Squared values. As we saw in Table "EMU Unemployment Rate and Changes," Germany has a much lower unemployment rate than other members and it has all but stopped falling while most members (9 of 12 in the table) are still seeing their rates fall on balance over 12 months. Over shorter periods unemployment rates fall for 6 to 7 members, about half of the group. But Germany is not in that grouping. The table of correlations shows how poorly the German unemployment rate correlates to its fellow long-term members' rates. Over the 12 countries in the table, Germany has negative correlations with unemployment levels in eight of them. The correlations on changes in unemployment are 'better' in the sense that there are fewer negative correlations (only two, for Greece and Portugal). When converted to R-squared values, these correlations on changes in unemployment rates drop to near zero for seven countries. Thus, for seven countries, Germany has a near zero correlation to unemployment rate changes. How do you run one monetary policy that takes all those differences into account?

Table "Relationships Among Long-Standing EMU Members" contains correlations run on unemployment levels and on 12-month changes in unemployment levels. The change correlations also are presented as R-Squared values. As we saw in Table "EMU Unemployment Rate and Changes," Germany has a much lower unemployment rate than other members and it has all but stopped falling while most members (9 of 12 in the table) are still seeing their rates fall on balance over 12 months. Over shorter periods unemployment rates fall for 6 to 7 members, about half of the group. But Germany is not in that grouping. The table of correlations shows how poorly the German unemployment rate correlates to its fellow long-term members' rates. Over the 12 countries in the table, Germany has negative correlations with unemployment levels in eight of them. The correlations on changes in unemployment are 'better' in the sense that there are fewer negative correlations (only two, for Greece and Portugal). When converted to R-squared values, these correlations on changes in unemployment rates drop to near zero for seven countries. Thus, for seven countries, Germany has a near zero correlation to unemployment rate changes. How do you run one monetary policy that takes all those differences into account?

While Germany is the largest economy in Europe, it is clear from this framework that is not necessarily the bellwether of European economic performance. As we see from the ranking of EMU data, the weight that Germany has in the EMU causes it to skew the economic performance of the EMU to an interpretation that is much more like what is happening in the German economy than to what is happening across more country jurisdictions.

Therefore, the notion that 'as goes Germany, so goes Europe' is subject to a caveat of how one wishes to understand the particular definition of Europe (meaning the EMU in this case) to which one is referring.

As we see in the chart at the top, the unemployment rates of the EMU, the U.S. and Japan have broadly moved together, but Germany's own unemployment rate has come down much more in line with the rates in the U.S. and Japan. The EMU rate itself is high where Spain's 14.1% rate and Greece's 16.8% rate along with Italy's 9.7% rate elevate the European average well above the German level (3.1% for Germany vs. 7.5% for the EMU).

These differences also help to 'frame' the ECB policy debate. Germany has seemingly no concerns that the ECB has been missing its inflation target chronically because the miss has been on the too-low side and because during this period German unemployment has been extremely low and far lower than for the rest of the European community. Germany's willingness to shrug off this target miss and to push for the ECB to normalized interest rates (i.e., to raise them) when the rest of the EMU area is not experiencing the same degree of economic joy as Germany is a potentially destabilizing political decision that cold isolate Germany even more if it comes to be seen as more than just an argument about 'monetary policy.' At a time that domestic demand is scare in the EMU, Germany is also running a fiscal surplus while other countries are running deficits and some of them are near (or over) the maximum deficit that is allowed. Germany's actions are not filled with any sense of 'team spirit.'

In short, there is a great deal of economic disharmony in the euro area that runs a single monetary policy for all. Germany has the largest EMU economy and its data skew the overall result for 'Europe' in its favor. But even so, EMU data do not support the move away from monetary stimulus that German policy officials seek. And Germany's decision to run budget surpluses when its fellow EMU members need stimulus is not an act of economic kindness. Moreover, amid this richness of economic results, Germany demonstrates how it does it by continuing to stone-wall the U.S. on making the larger contribution to NATO that has been sought for a long time. As it is Germany's own standing army is a joke of capability and preparedness. European unity has a long way to go. And it is fair to wonder if it will ever reach its destination or Europe will remain a place where local jurisdictions (countries) will continue to pursue their own best interests regardless of the mess it makes for the rest of the community.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief