Global| Dec 02 2020

Global| Dec 02 2020EMU Unemployment Rate Ticks Lower

Summary

The number of unemployed in the EMU continues to fall and this month that drop was enough to move the rate of unemployment lower as well. The EMU-wide unemployment rate fell to 8.4% in October from 8.5% in September. The EMU [...]

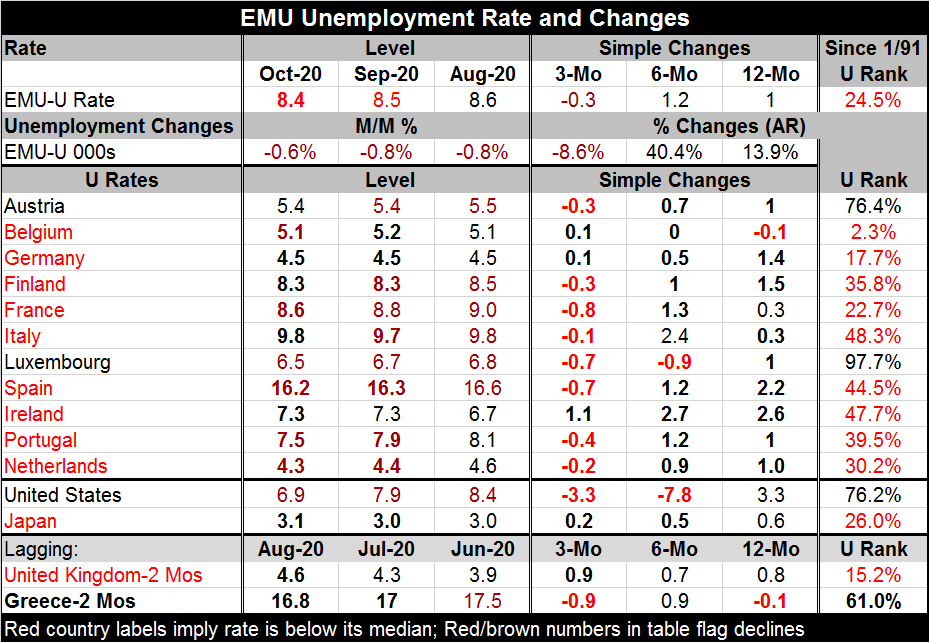

The number of unemployed in the EMU continues to fall and this month that drop was enough to move the rate of unemployment lower as well. The EMU-wide unemployment rate fell to 8.4% in October from 8.5% in September. The EMU unemployment rate is lower by 0.3 percentage points over the last three months, compared to being higher by 1.2 percentage points over six months and higher by 1.0 percentage point over 12 months.

The number of unemployed in the EMU continues to fall and this month that drop was enough to move the rate of unemployment lower as well. The EMU-wide unemployment rate fell to 8.4% in October from 8.5% in September. The EMU unemployment rate is lower by 0.3 percentage points over the last three months, compared to being higher by 1.2 percentage points over six months and higher by 1.0 percentage point over 12 months.

Of the 11 EMU members reporting October unemployment rates in the table, six showed rate declines in October and four countries showed a steady rate month-to-month while Italy shows an unemployment rate increase. Eight countries had shown month-to-month unemployment rate declines in September.

Trends show widespread unemployment rate declines over three months within the EMU, compared to widespread increases in unemployment rates over six months and 12 months.

Among the 12 EMU countries reporting data in the table (this total includes Greece where unemployment data lag), only three countries – Austria, Luxembourg and Greece – have unemployment rates that reside above their historic medians (calculated on data since 1991).

Germany reports the numerically lowest unemployment rate at 4.5%, but by ranking Belgium has the lowest percentile standing among all countries; its rate of unemployment ranking is at the 2.3 percentile. Germany at the 17.7 percentile is the next lowest. The ranking for the population weighted EMU rate overall is in its 24.5 percentile.

The table also provides comparisons with the United States, Japan, and the United Kingdom. Although the U.S. economy overall seems to be performing better than the EMU, the U.S. labor market is not. U.S. unemployment sits well above its median for the period at a 76.2 percentile standing. While the U.S. has been able to sustain consumer demand and revive industry to some extent, the hammer blow to the U.S. service sector dislodged a number of workers who remain unemployed and for who a debate about providing assistance is now in gear. The unemployed have become a political football in the U.S. caught in an argument between Republicans and Democrats about how much assistance to provide overall.

Clearly the virus has had differential impacts on economies and on local labor markets. The U.S. economic system has probably put the most stress on those whose businesses were shuttered or whose jobs were lost. That is notwithstanding that the U.S. has done a good job of rebounding GDP and of supporting aggregate demand. The impact on all aspects of the economy has not been as successful as support of demand.

Of course, November proves to be a more difficult month for Europe with many further restrictions having been put in place. The U.S. is in the middle of its own virus expansion that it has so far tried to handle without broad nationwide measures. The virus is not done wreaking havoc with economic trends yet.

However, the light at the end of the viral tunnel flashed on today with the U.K. announcement that it has approved the Pfizer-BioNTech vaccine. Britain’s regulator has deemed the vaccine safe paving the way for a roll-out. Pfizer reports that the first doses for the U.K. are already on their way. This could well be the beginning of the end game for the virus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief