Global| Jul 01 2021

Global| Jul 01 2021EMU Unemployment Rate Falls in May As Progress Continues; The Good, the Bad, the Blemished...and the Worried

Summary

The EMU unemployment rate dropped in May, signaling that EMU-wide progress is still on track. However, the EMU unemployment rate is only four tenths of a percentage point (0.4) higher than it was before Covid-19 struck, leaving EMU [...]

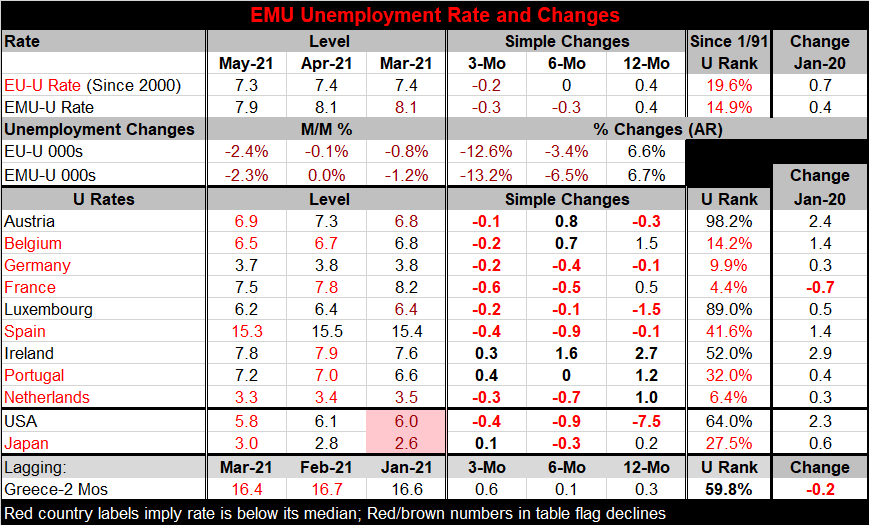

The EMU unemployment rate dropped in May, signaling that EMU-wide progress is still on track. However, the EMU unemployment rate is only four tenths of a percentage point (0.4) higher than it was before Covid-19 struck, leaving EMU labor markets less shocked than the labor market Covid experiences that Japan and that the U.S. have experienced. In the U.S. in particular, the shock is much greater since the unemployment rate there is higher by 2.3 percentage points even though it is down by much more from its Covid peak.

The EMU unemployment rate dropped in May, signaling that EMU-wide progress is still on track. However, the EMU unemployment rate is only four tenths of a percentage point (0.4) higher than it was before Covid-19 struck, leaving EMU labor markets less shocked than the labor market Covid experiences that Japan and that the U.S. have experienced. In the U.S. in particular, the shock is much greater since the unemployment rate there is higher by 2.3 percentage points even though it is down by much more from its Covid peak.

The Covid-19 infection was financial too

The U.S. and Europe managed the impact on their labor markets quite differently as Europe buffered the impact by taking policy steps to keep people employment. In the U.S., it was unfettered capitalism at work with distressed firms letting staff go, or going out of business themselves, and with a few government programs providing assistance to firms to try to keep them afloat. Of course, policy in the U.S. was more interventionist as far as workers were concerned. Policymakers sent several blankets of checks to all tax filers below certain income levels and topped up unemployment benefits. And states generally administered the unemployment programs with great generosity. These policies produced very different results for consumers and very different impacts on labor markets in the U.S. compared to the EMU. U.S. consumer spending has run ‘off the charts' recently in response to the payments (despite elevated unemployment in the U.S.) and the savings rate is up sharply too. The clear message is that Covid displacements were more than compensated for in the U.S.-at least in the aggregate. Europeans were supported but less aggressively and they were not made whole or over-compensated as in the U.S.

Covid leaves is mark…and it's not done yet

Official fiscal debt data do not yet fully describe the extent of debt increases incurred during the Covid crisis. But Europe and the U.S. are going to show huge increases in their respective debt-to-GDP ratios. Germany was trying hard to compress is ratio below 60% mark sought by EU rules and to accomplish that it was resisting U.S. calls for Germany to spend more on military aid to NATO. Germany refused to pay more for its own defense to make this fiscal progress. This objective has to give way and to allow its debt-to-GDP ratio to surge back up toward the 80% mark as Germany pulled out the stops for Covid spending. I guess Germany sees Covid-19 as a bigger enemy of the state than Russia (…from whom Germany is going to purchase an even larger proportion of its energy).

The distribution of unemployment

Among the nine EMU nations in the table, only France has a net lower unemployment rate since January 2020 before Covid struck Europe. Greece, on a two-month lag, also reports a net lower unemployment rate but at a much higher level of unemployment. However, three EMU nations (four countries including lagging Greek data) show rates of unemployment above their historic medians; these include Austria, Luxembourg and Ireland. The U.S. is also a member of such a group.

In the EMU, of the nine countries in the table 7 have unemployment rates falling on balance over three months, five have them falling on balance over six months. Only four of them are falling on balance over 12 months. These metrics make it clear that much of the progress in Europe is recent. And while Christine Lagarde has continued to focus on getting Europe on the mend, several have begun to raise questions about how long it is appropriate to keep such stimulus in gear. This week Germany's Jens Weidmann and Austria's Robert Holzmann became the first European central bank officials to openly debate winding down its pandemic emergency stimulus. So Europe is now engaging that debate too.

The legacy of Covid

Unemployment rates are falling. The act of putting the pieces back together to reform Humpty Dumpty is well underway. And although Humpty could not be put back together, in this case repair will be made but there will be blemishes. Lives have been interrupted. Some have been lost. Businesses have been harmed or bankrupted; Covid-19 will leave its scars. The remaining question is how badly Covid scars will weigh on the economy in other ways such as in scarring workers' memories and willingness to work or even consumer willingness to participate in the economy again.

Soccer fans (football fans) fear no Covid

Some of these concerns may be overblown. This week what we are witnessing is scorching criticism against the European Cup officials who have allowed high occupancy stadiums to cheer on their teams. Fans as a result are ‘spreading Covid-19. It will take some time before we see how much damage this tournament has done or how well vaccination protected us all… Or how safe it is to congregate if we are outside… These notions all will be tested. But for now we see football fans with seemingly no scarring whatsoever. They are only afraid of their team losing.

Manufacturing PMIs (hot, hot, hot)

Manufacturing PMIs (hot, hot, hot)

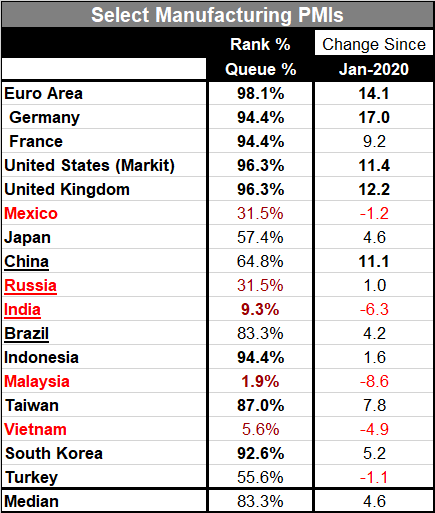

Also launched today were the final manufacturing gauges for the Markit manufacturing PMI data. We see for a number of high-profile manufacturing sectors from the U.S. to Europe to Asia the average percentile standing (on data ranked over the past 4.5 years) is at its 83rd percentile. This unweighted measure suggests that manufacturing has been in better shape over the period only 17% of the time. Meanwhile, from January 2020 the median gain in the manufacturing PMIs has been 4.6 points…although some have done much better.

Five countries on that period have experienced double-digit point gains. These gains are led by Germany (+17.0), the whole of the euro area (+14.1), the U.K. (+12.2), the U.S. (+11.4), and China (+11.1). France is a near-miss with a gain of 9.2 points.

Five countries are still worse off on this timeline; they are all developing economies: Malaysia (-8.6), India (-6.3), Vietnam (-4.9), Mexico (-1.2), and Turkey (-1.1).

There is a ‘theme' here as the most developed countries are doing the best while developing economies lag.

On a different scaling, there are five countries whose queue or rank standings are below their historic medians (below a ranking of 50%) on this timeline. They are Russia, Mexico, India, Vietnam, and Malaysia.

Getting better but with issues

The manufacturing scene is getting better; yet, it is also beset with supply chain problems. Still, it is moving ahead. In the European data today, very hot input prices were recorded and the same is true of input prices in the U.S. reports. Of course, when markets heat up, output and employment expand. And when demand exceeds the ability of physical supply to deliver the goods, price rationing and non-price rationing sets in. With that, those willing pay more have their demand sated and others may have to sit back and endure longer delivery lags.

Central banking song book: Don't think twice, it's alright

The Bank of England has joined the Fed in singing the chorus of policy restraint on the belief that the bottleneck pressures will alleviate themselves in time with no lasting scar on inflation. Will they? Meanwhile, several monetary officials at the ECB are taking this opportunity to try to phase out or at least question the retention of the Covid stimulus as that Bank has been in a super stimulus mode since the financial crisis. Some monetary officials in Europe fear the impact of such stimulus being excessive and have begun the process to undo it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief