Global| Sep 14 2018

Global| Sep 14 2018EMU Trade Trends Sour

Summary

As the chart amply demonstrates the EMU trade surplus has been under pressure for some time. Since late 2016 imports have been outpacing exports on a consistent basis although the differences in the export and import growth rates have [...]

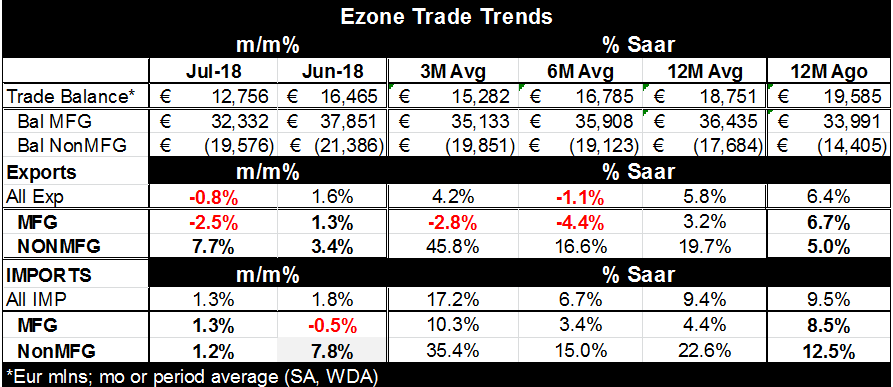

As the chart amply demonstrates the EMU trade surplus has been under pressure for some time. Since late 2016 imports have been outpacing exports on a consistent basis although the differences in the export and import growth rates have vacillated. It is only since late 2017 that the import growth outpaced exports enough to consistently drive the surplus lower. This month the drop in the surplus is a sharp €3.7bln. An outsized €5.5bln of the surplus reduction came from manufactured goods while the deficit on non-manufactures moved in the other direction shirking by €1.8 bln (adding to the surplus, or in this case, eating into the surplus reduction created by manufactured goods trade).

The exports of manufactured goods have been losing momentum with the imports of manufactured goods gaining momentum. Non-manufacturing import trends have bene volatile having been kicked around by the behavior of commodity prices, especially oil.

Manufactures make up 81% of EMU exports and 70% of EMU imports. So the manufacturing trend will dominate in the long run… but in the short run it is the nonmanufacturing trends that are the most volatile and influential despite their smaller size.

EMU shows manufactured exports moving from a 3.2% rate of growth over 12-months to -2.8% over three months. At the same time manufactured import trends show a shift from a 4.4% pace over 12-months to a sizable 10.3% pace over three months. Manufactured exports are shrinking as manufactured imports are surging- that shrinks the surplus.

Meanwhile, while on the same time line, non-manufactures both exports and imports are transitioning from near 20% growth rates over 12-months to a pace of 35% or 45% over three months, with imports growing faster than exports (also pushing the trade balance to a smaller surplus). Clearly the non manufactures are driving much of the change in the short run- event though they are a mitigating effect in this month’s balance calculation. The balance on manufacturing trade for EMU has actually been slightly rising showing a greater surplus since end 2016 - with this month’s drop being a notable exception to that trend. But the non-manufacturing balance has been in deficit and slipping into deeper deficit on that same time line-eroding the surplus. These two effects have been grinding at cross purposes.

The EU trade balance trend has embodies this two contrary forces for some time. These sorts of divergent trends make the trade picture a bit harder to understand.

Of course, a further complication in this picture is the pending trade war. Europe is now in the middle of one as it and the US are negotiating a new arrangement. But the US and China are embroiled in a trade war and that could get worse before it gets better. European trade could be impacted by two different effects (1) by leads and lags and (2) by trade deflection. If Chinese goods are being deflected from the US market by high tariffs they could wind up in greater numbers destined for Europe increasing European imports. Or trade could be affected by leads and lags as exporters between the US and Europe (on both sides) may decide to ramp up exports…They would do this just in case the simmering trade conflict breaks out into war if the US and Europe cannot reach an amicable result.

The chart of the Baltic dry goods index now gives us some information on this as it shows trade volumes rising sharply after a period of weakness and then it shows them tailing off again. This could be the leads and lags process as exporters tried to expedite shipments to get goods across a border before tariffs went into effect. After that surge flows are reduced in the wake of tariff imposition. The index does not tell us anything about trade deflection, however.

On balance the trade spat could have an impact on trade flows, on industrial output and on growth as well as on inflation. Short terms tariffs should raise inflation, but if tariffs impede growth, the longer terms effect would be for inflation to get lower. In addition as trade restrictions have an economic effect, exchange rates may be set in motion and since globally commodities are priced in dollars anything that impacts the dollar will also impact commodity prices to the rest of the world and set a different pulse of stimulus into the act.

Fortunately this is not your typical or garden variety trade war. Donald Trump started this war to try to get trade on fairer terms for the US with an aim of reducing trade barriers. This not tariffs being imposed for the sake of protection. Still, others have met this with retaliation and the US and China and the US and Canada are still embroiled in trade rows. So we are in an interim period in which the impact of tariffs may have their ‘classical effect.’ But this period is not supposed to last long. However, when trade negotiating is the issue no one ever knows how long it will take. So hold on! It could be short-lived or a long, disruptive ride.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief