Global| Apr 20 2020

Global| Apr 20 2020EMU Trade Surpluses Expand As the Virus Swirls

Summary

In the EMU, neither exports nor imports show much zest. But exports had some life in their year-on-year trend and that is helping to drive a wider surplus in the EMU area. Broadly both exports and imports are fluctuating in relatively [...]

In the EMU, neither exports nor imports show much zest. But exports had some life in their year-on-year trend and that is helping to drive a wider surplus in the EMU area. Broadly both exports and imports are fluctuating in relatively low ranges, but the key difference is that imports are generally fluctuating at low rates of contraction while exports are fluctuating at low rates of expansion. That plus/minus line makes all the difference in the world.

In the EMU, neither exports nor imports show much zest. But exports had some life in their year-on-year trend and that is helping to drive a wider surplus in the EMU area. Broadly both exports and imports are fluctuating in relatively low ranges, but the key difference is that imports are generally fluctuating at low rates of contraction while exports are fluctuating at low rates of expansion. That plus/minus line makes all the difference in the world.

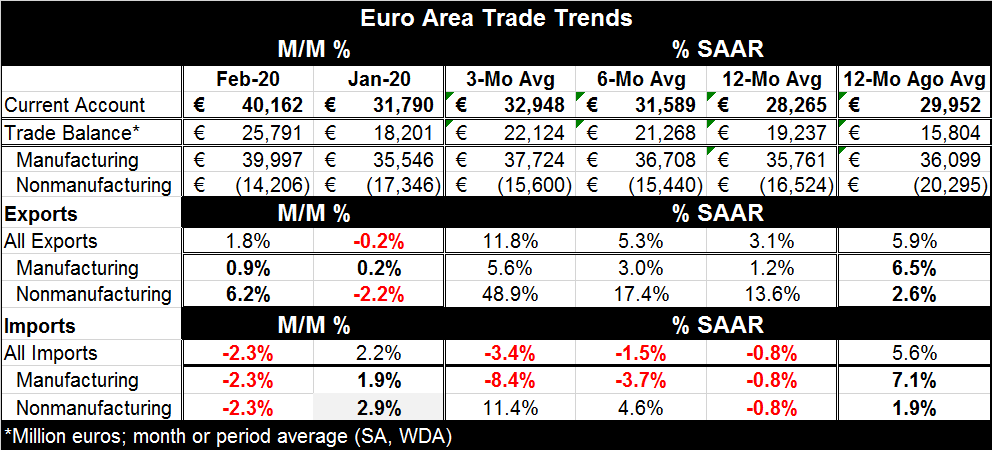

The trade balance and its three-month average are above the 12-month average and that is true of the current account as well. The EMU surpluses are sharply higher this month.

The reason is clear as exports grew by 1.8% while imports fell by 2.3% and created a powerful surge in the surplus which is the difference between these two flows. Interestingly both manufactured and nonmanufactured goods followed that same pattern in February,

EMU exports of nonmanufactured goods are surging, rising at a 48.9% annualized pace over three months, up steadily from a 13.6% pace over 12 months. On the import side, nonmanufactures are moving up too and accelerating from a -0.8% drop over 12 months to 4.6% gain over six months to an 11.4% pace of expansion over three months. Obviously, exports are dominating this net balance driving it to a sharply higher EMU surplus.

Manufactured goods show the same trend this time dominated by sinking EMU imports. On the export side, export growth does step up from a pace of 1.2% over 12 months to a pace of 5.6% over three months. But imports of manufactures that fall by 0.8% over 12 months decelerate and fall at an 8.4% annualized rate over three months dominating all trends in manufacturing.

These figures show that EMU exports are surviving, but that EMU domestic demand has dried up. Even the exports that are expanding and pulling in imports to support them, are not able to offset the impact of domestic demand weakness on imports. The sharp pullback in manufacturing imports helps to contract the trade deficit and to cushion the blow on EMU GDP growth.

Germany has been debating a domestic stimulus package and in a news report Angela Merkel is counseling for a smaller package lest southern European countries think Germany has the resources to help them too. Let there be no doubt that we are in a world of everyman for himself, obscured by some window-dressing of 'care' for our fellow man.

In this world, politics continue to play out in spades as U.S. President Trump has severed support for WHO because of its close ties and support of China that he sees as part of the reason that the pandemic spread so fast and has damaged his chance at reelection. In the U.K., there are calls to investigate the government's response, calls that are being set aside for another day. In the U.S., there is political infighting about support packages. Even candidate Joe Biden is trying to blame President Trump for being at fault because he was 'too close to China's Xi.'

Taiwan surprisingly reported a rise in export orders in March. The gain in Taiwan orders was rather broad based but not unequivocal. The report is for the month of March, a month in which significant weakness has emerged in most economies. Still, the growth in Taiwan's orders spans electronics, machinery, information and communications products led by a 23.8% jump in electronics. Many other categories showed declines. But Taiwan's numbers do seem to show that perhaps the tech-most aspect of economies are still vibrant especially with 'sheltering at home' and the need for technology equipment to permit and enhance that. While travel and leisure sectors are flat on their back, technology still has life and we can see that in the global equity market indexes and share prices where so many true tech companies have lost little or no ground in this selloff.

However, the overarching view is that global growth is weak and will remain so. A handful of countries are planning to reduce their lockdowns and think they may have passed the peak of the crisis. Still, those counties will move slowly and cautiously. Anyone looking for a V-shaped recovery will have to try a different planet.

In the U.S. talks, arguments and exposés are in vogue about the ongoing government programs and plans for new ones or just plans to top-up existing programs, just like in Germany. Australia has challenged China to tell the truth about what happened and it has been rebuked with China telling countries not to meddle in its affairs. This position by China will be resisted. China has no scope to call this 'its affair' when its public health failure has spawned a pandemic that has infected and killed people in nearly every country on earth. I think this crisis will put an end to China's obstinance or to the increased role it has been playing in the global economy. Something very significant has got to give and China needs to open up or to damp down its ambitions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief