Global| Feb 15 2017

Global| Feb 15 2017EMU Trade Surplus to 8-month High - More Angst for Trump

Summary

A surplus bigger than a bread box...bigger than the bread factory The EMU trade surplus swung to an even wider surplus in December, its widest in eight month and the second widest on record. Exports and import are swinging up as both [...]

A surplus bigger than a bread box...bigger than the bread factory The EMU trade surplus swung to an even wider surplus in December, its widest in eight month and the second widest on record. Exports and import are swinging up as both flows hint at some sort of recovery in progress that is enveloping both exports and imports.

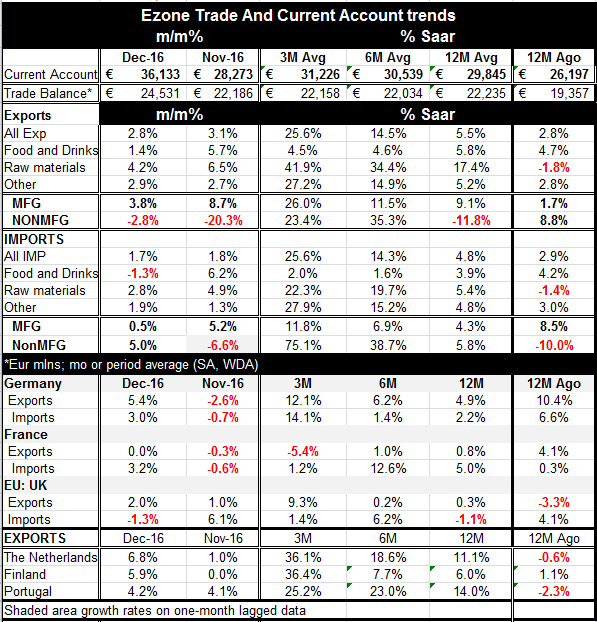

Trade flows accelerate Overall EMU exports and imports are both accelerating on growth rates over 12-Mo to 6M- to 3-Mo and both are expanding solidly over 12-months. But more importantly manufacturing exports and imports are showing the same pattern. Free of distortions from oil prices and other commodity prices EMU trade flows show expanding trade on both the export and import side.

Trends are widespread Among the individual countries we detail in the table all show expanding exports on all multi-month horizons except for France over three-months. All also show expanding imports on all multi-month horizons except for U.K. imports over 12-months. The UK is a bit of a special case with the pound sterling having fallen sharply, an action that should pinch imports and expand exports-and that process does seem to be well underway in the U.K.

Some are very strong Dutch, Finnish and Portuguese exports are especially strong over the most recent three-months with all showing annualized growth rates of 25% of more on that horizon.

Support for view of a global pick-up On balance trade seems to signal what other economic indicators have been showing: that there is an economic revival. Or course, we have to be careful when using trade as a litmus test for activity since exchange rates play an important role and can affect trade flows quite apart from whatever activity trends are in play. The ongoing weakness of the euro will tend to boost EMU exports and reduce imports. But so far there is no evidence of any special import weakness. However, more broadly, the growing EMU trade and current account surplus is indicative of a currency that is too weak and is unduly restricting imports and boosting exports.

PPP calculations identify the euro as a problem The chart above looks at the euro using a trade weighted framework and an inflation adjusted indicator. PPP (purchasing power parity) provides a simple way to assess the exchange rate. For EMU we see that the real multilateral exchange rate measure has been below its average value (or the estimate of its parity value) marking the currency as a candidate to be considered undervalued. The euro on this gauge is nearly 7% below its mean and is at its second weakest level on data back to 1990. Meanwhile, supporting the idea of a euro that is "too weak" is the fact that the exchange rate is persisting at this position with the second highest current account surplus on record. QED?

FX and trade performance leave their fingerprints as the "crime scene" This couplet of data is exactly the sort of thing that the Trump Administration has been railing about.. The Euro-Area surplus began in late 2011 but has continued to mushroom as the region has fought its own demons with excessive monetary weakness and as the euro has plunged below its average on the same time line that the surplus expanded. Germany"s surplus is a big part of this and its surplus as percent of its own GDP is the highest in the world among developed economies and others. Moreover, Germany has not been a "good citizen" trying to restore its trade to a balanced position. Germany was targeting a fiscal budget surplus until the migrant situation developed and it long has underspent its NATO objective for military spending of 2% of GDP. It"s not like the Germans have been true to their other obligations as all this happened. It did not "happen." It was "engineered."

German engineering...apart from VW Germany has created a sheltered nest for the implicit deutsche mark nestled deep in EMU by running the persistently lowest inflation rate in EMU making Germany the most competitive country in EMU. By getting shelter in the euro and an added boost to competitiveness by being in a union with other much weaker less-competitive economies whose circumstances draw down the value of the euro Germany has further enhanced its competiveness and economic performance. No wonder Germany is willing to do so much to keep Greece in the fold. In this way the euro itself has become an anti-competitive currency bloc and a bloc whose currency value is actually in some ways inconsistent with the very existences of free trade since its own internal disequilibria prevents the euro from being at a value that is consistent with equilibrium for most of its members and for Germany at the same time.

Danger! The danger of deficits These are the sorts of things that have developed in the global economy to the detriment of the US trade position and US competiveness. The erosion of US competitiveness costs the US jobs and causes US firms to seek to build plants overseas instead of inside the US itself. The strong dollar keeps US purchasing power strong and makes the US an export target for other nations. But all of this is eventually incompatible since a country cannot specialize in importing with a too-strong currency that prevents investment and exporting and imbues that economy with a large structural and growing current account deficit without consequence. At some point the deficit will undermine income growth and will drain wealth and the consumption machine will crumble. The point is to fix this arrangement before it goes too far and puts the US in that adverse dynamic. Right now the US is still in the stage that is akin to running up the balance on its credit card. This part is still "fun." Despite being the principal global reserve unit, the day of reckoning when the US credit limit is reached and debt will have to be repaid on onerous terms (think Greece) is still out there. Credit rating agencies already are watching the US and the Trump administration very closely in setting the US credit ratings. It is best to act long before such a dead end is on the horizon. Right now Europe is part of the problem not part of the solution. Japan is running the same sort of policy. China has never ending surpluses; so do many other Asian economies. The Trump Administration is going to tackle these uncompetitive arrangements and everyone is upset... yet all this amounts to is that the US trying to re-establish a level playing ground where none now exists. Don"t kid yourself. There is very little in the world today that really conforms to the label "Free Trade". Europe"s scheme is a great example of why. Some see Trump as rocking the boat but he is not the one making most of the waves out there. He is simply trying to better navigate the chop.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief