Global| Apr 19 2017

Global| Apr 19 2017EMU Trade Surplus Rises But Remains Moderate; Still There Is No Sign of Fundamental Deficit Adjustment in Europe

Summary

The EMU trade surplus popped up again, reversing part of last month's drop. Still, the surplus appears to be on a declining path. Apart from last month, this month's surplus is the smallest in 16 months. However, it is too soon to [...]

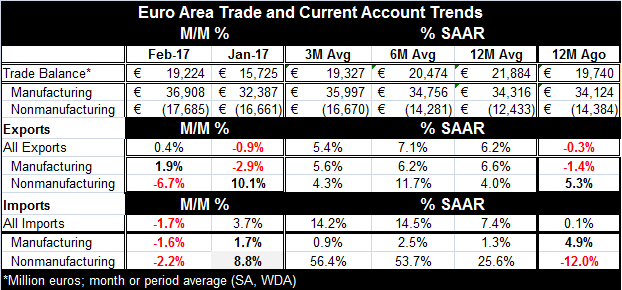

The EMU trade surplus popped up again, reversing part of last month's drop. Still, the surplus appears to be on a declining path. Apart from last month, this month's surplus is the smallest in 16 months. However, it is too soon to call this a durable trend in the balance since we have seen balances narrow then balloon again. The question is this: is the shrinkage based on something fundamental? Imports are growing faster than exports and are doing so on each horizon from 12-month to six-month to three-month. That much looks like solid adjustment under way. But unfortunately, since oil prices have been rising, the import gain has a lot to do with oil and with oil prices. If we compare trends on manufacturing exports and imports, exports still outpace imports on all horizons.

The EMU trade surplus popped up again, reversing part of last month's drop. Still, the surplus appears to be on a declining path. Apart from last month, this month's surplus is the smallest in 16 months. However, it is too soon to call this a durable trend in the balance since we have seen balances narrow then balloon again. The question is this: is the shrinkage based on something fundamental? Imports are growing faster than exports and are doing so on each horizon from 12-month to six-month to three-month. That much looks like solid adjustment under way. But unfortunately, since oil prices have been rising, the import gain has a lot to do with oil and with oil prices. If we compare trends on manufacturing exports and imports, exports still outpace imports on all horizons.

In fact, the trend in the manufactured goods trade balance shows that surplus to be moving mostly sideways with a small uptrend. EMU surpluses under the cover of oil prices are still large and steady or expanding. There is no fundamental shrinkage in play despite the headline and the 'trend' of the last two months.

Not only have EMU exports traded in the 5.6% to 6.6% growth range, but import growth (i.e., domestic demand) remains stunted. The growth in manufactured imports on sequential growth rates from 12-month to six-month to three-month varies in a range from 2.5% to 0.9%. These are pathetically weak numbers since they are expressed in nominal terms.

Nonetheless, the good news on the trade front is that the International Monetary Fund is for a change raising its forecasts for growth. The IMF said in a report released Tuesday that world economic growth is set to improve to 3.5% this year from 3.1% in 2016. That is not a huge pick-up, but it is good news and represents a change from the pattern of paring the outlook that previously had been the IMF's practice. Still, Europe remains constrained by its debt and deficit ratios under the Maastricht rules. Germany has flexibility to act but does not seem to have the taste to do it.

What is interesting is to ponder where this growth expansion will occur and what will drive it. We would expect trade growth to pick up in an environment in which global GDP speeds up. But Europe is still very debt constrained and the U.S. may be in the process of reconsidering exactly what it will do. After the election of Donald Trump, there was some excitement about U.S. growth prospects. Market gauges have flared and held their gains for the most part; even the Fed got excited enough to speak of a program of rate hikes (which it claimed did not factor in much if any fiscal stimulus). But recently the rise in bond yields has given way to back-sliding and the optimism on tax cutting has also been somewhat scaled back. Economic performance in Q1 has steadily diminished to the point where first quarter U.S. GDP growth could come in below 1%. In China, leaders are warning of potential unemployment and economic displacement as they shift gears and exit some old and inefficient industries. Moody's recently saw evidence of some reflation in Japan, but we should not expect too much of that. The IMF has just cut its outlook slightly for India. In short, if global growth is going to pick up, where will that be and how will it be motivated? Go here to see the IMF's comment which at this point is still very general.

Thoughts on the outlook are still developing, but there is more optimism and a feeling that the new Trump Administration in the U.S. will bear some fruit in terms of enhancing growth. Apparently some of the early talk about trade disruption potential and that being negative has been set aside. There is very little pick-up in growth being assessed in the developed economy group as a whole. Instead emerging market economies are expected to have the largest gains. The IMF is looking for a restoration of normalcy across emerging markets and for some growth pick-up in China. Despite the optimism, the IMF sees global risk as tilted with risks still leaning to the downside.

The economic environment is complicated with the new president in the U.S. ruffling feathers and the EMU still struggling to gain its balance as central banks ponder switching their own gears. OPEC gave prices a shot of juice in the form of higher oil prices that that perked up inflation, but that already is showing itself to be more a relative price lift than an actual inflation force. EMU and U.S. inflation statistics have settled back quickly since the oil price push lost its gusto. Central banks that were getting restless for policy change now feel less motivated and less threatened by inflation. It is unclear where the Fed sees things as U.S. inflation has failed to continue to rise and as wage pressure fails to mount even on what is deemed to be now an 'excessively low' unemployment rate. The outlook remains more muddled than settled and is still as prone to change as any we had in the last several years. Despite the IMF growth upgrade, there is still economic risk and the geopolitical climate has deteriorated considerably at the same time. The growth 'outlook' may have been raised, but there is still a lot of caution among those that evaluate the global economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief