Global| Apr 17 2019

Global| Apr 17 2019EMU Trade Surplus Expands on Weak Imports

Summary

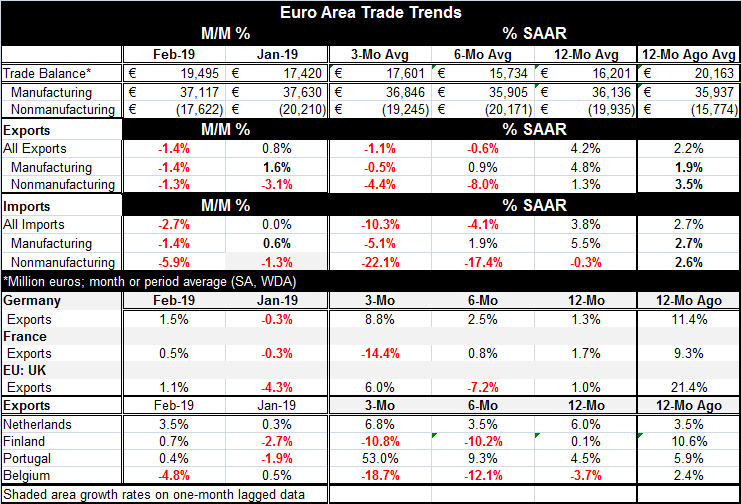

The euro area trade surplus rose to 19.5 billion euros in February from 17.4 billion euros in January. The surplus is slightly smaller than its 20.2 billion euros surplus of 12-months ago. Month-to-month the balance of trade for [...]

The euro area trade surplus rose to 19.5 billion euros in February from 17.4 billion euros in January. The surplus is slightly smaller than its 20.2 billion euros surplus of 12-months ago. Month-to-month the balance of trade for manufactures shrank. The month’s surplus expansion comes from the shrinkage of the deficit in nonmanufacturing trade.

The euro area trade surplus rose to 19.5 billion euros in February from 17.4 billion euros in January. The surplus is slightly smaller than its 20.2 billion euros surplus of 12-months ago. Month-to-month the balance of trade for manufactures shrank. The month’s surplus expansion comes from the shrinkage of the deficit in nonmanufacturing trade.

Exports show widespread weakness. Manufacturing exports are up by 4.8% over 12 months but slow to a 0.9% pace over six months and are contracting at a 0.5% annualized rate over three months. The exports of nonmanufactures are declining over three months and six months but growing at only a 1.3% pace over 12 months.

Imports echo the weakness for manufactures; manufacturing imports are decelerating their growth from 12-months to six-months to three-months. And nonmanufacturing imports are contracting on all timelines as well as decelerating following the lead of exports.

There is nothing reassuring in these trends as both exports and imports show ongoing shrinkage in their respective flows and manufacturing is showing gathering weakness. Weak exports suggest ongoing weak global demand. Weak imports suggest that domestic demand in the EMU area is weakening. Of course, these are nominal numbers and weak commodity prices will factor in for nonmanufacturing trends, but oil prices have been rising during this period not falling. And there is also the possibility that uncertainty over Brexit also has been affecting trade flows, creating weakness.

Export detail from selected European economies shows mixed results; there is no case for overarching weakness or strength. However, most flows are weak over 12 months. The strongest nominal exports are for a year-over-year growth rate of 6% by the Dutch with six countries logging 12-month rises that are less than that. But over three months, four of these countries show growth no weaker than 6% (annualized) while two others, Finland and Belgium show double-digit declines. These trends are hard to categorize; I consider them mixed. There is a sequential acceleration only in Portugal and Germany. Belgium, Finland and France show sequential deceleration.

The United States and China are reportedly getting closer to a trade deal, but we have head of such progress in other negotiations before that broke down. I hope that is not the case with China. Skepticism is warranted until a deal is actually announced. Meanwhile the U.S. and the EU are starting to square off over trade. Brexit continues to hang in the balance unresolved creating mischief especially for the U.K. but also for its main trading partners and that includes Germany. The global economy looks to be continuing to slow based on EU trade data trends. And there are still further shocks in train for the global economy. And we still have China playing cat and mouse in the South China Sea with Japan over their territorial claims and conflicts. Moreover, Kim Jong-un seems to be back to firing up activity in his nuclear facilities. Things are not settling down even though there is a movement afoot to regain lost optimism.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief