Global| Nov 19 2015

Global| Nov 19 2015EMU Trade Surplus Climbs While Underlying Flows Sink

Summary

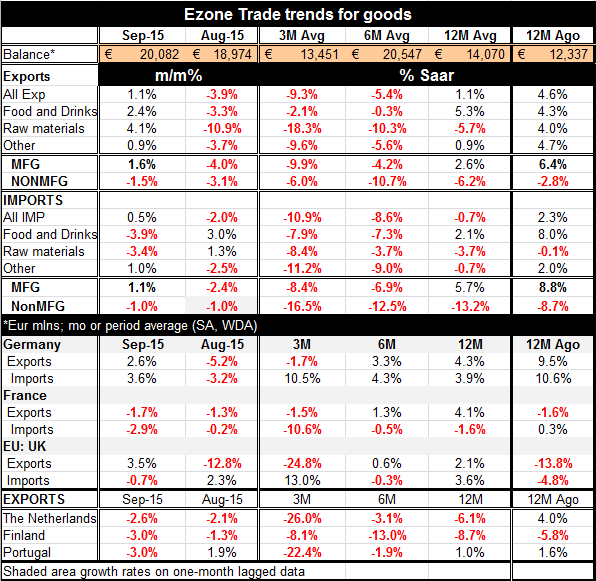

EMU posted a wider trade surplus in September as that surplus moved up to 20.1bln from 19.0bln Euros in August. But a widening surplus does not mean that all is well in EMU or in the rest of the world. EMU exports rose by 1.1% in [...]

EMU posted a wider trade surplus in September as that surplus moved up to 20.1bln from 19.0bln Euros in August. But a widening surplus does not mean that all is well in EMU or in the rest of the world.

EMU posted a wider trade surplus in September as that surplus moved up to 20.1bln from 19.0bln Euros in August. But a widening surplus does not mean that all is well in EMU or in the rest of the world.

EMU exports rose by 1.1% in September after plunging by 3.9% in August. EMU exports are still on a path of solid deceleration as exports rise by 1.1% over 12-mo then contract at a 5.4% annualized pace over 6-months and at -9.4% pace over 3-months. EMU exports are in a tailspin! Not even a highly competitive exchange rate can stoke EMU exports. The EMU trade surplus is being created by even weaker imports: Not Good News!

In September EMU exports ticked higher, rising by 0.5%. But EMU imports are not strong; they are weak. They are falling by 0.7% over 12-months and declining at a horrific -8.6% annualized rate over six months and at a more disturbing pace of -10.9% over three-months. This is an alarming trend. It says very bad things about domestic demand in EMU.

EMU imports and exports are declining over three-months and over six months in all major categories. This is very bad news since trade drives global growth as well as growth in productivity.

The OECD today reports that in Q3 the OECD area slowed growth to 0.4% compared to a 0.6% pace in Q2. This slowdown simply reinforces the sluggish and somewhat dangerous state of the OECD area. We show some trade results for six counties in the bottom of the table and five of the six show exports falling in September. Six of six show exports falling over three months.

The weakness in the global economy and in the euro-zone is real. So far in EMU, as well as in the U.S., service sector performance has been keeping growth alive. But service sectors are also burdened. And in Europe their momentum is uneven. In the U.S., the service sector has been strong, but it has started to show some unevenness.

The service sector is a low-productivity sector. Services are largely not tradeable goods as only special categories of services engage in international trade. When growth is led by the service sector it will be much less dynamic and less remunerative to workers. And that is what we are seeing in the U.S. and in Europe as well as in China and in Japan. In a report released today Japan reported a decline in its all-industry index; it fell despite a growth contribution from Japan's service sector.

While the dollar did not react to the release yesterday of the last Fed meeting minutes that seem to point to a December rate hike, the dollar remains overvalued. With the Fed set to hike rates and the ECB set to engage in further stimulus, the dollar surely is poised to move even higher. With such confusion at the Fed about what to do, and how fast to do it, markets could not possibly have digested what policy will be and could not have braced for it. The dollar could still have some major moves ahead of it with adverse consequences for U.S. trade flows and for U.S. and global inflation. After the speech given by Fed Vice chairman Stanley Fisher about the transmissions effects of the strong dollar, it does not seem that the Fed projects a very large role for dollar strength in spreading deflation through commodity prices- even though it does that. The Fed seems ready to make policy and to ignore important international repercussions.

We live in a world where monetary policy has been overused but where there is nothing else to replace it. Just because monetary policy has been less than fully effective in kindling growth I would warn against adoption of the philosophy of symmetry and the belief that monetary policy now can tighten without much effect either.

The weakness in global trade flows is a wake-up call about global weakness. We do not just have weakness but the weakness is getting worse. I doubt that the service sector can really stop this from unraveling. I hope policy-makers have a better grip on things than they seem to have judging from their published remarks.

Layering new concerns about terrorism on top of all this is not a good thing. Although migrants escaping warfare will need to be taken care of and some additional monies will be spent on them, I would like to not exaggerate the stimulative aspect of this sort of spending. They are not getting expense accounts a Harrods after all. They will be fed and sheltered and clothed as they would have been had they stayed home (and lived). Let's not exaggerate that impact.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief