Global| Dec 17 2018

Global| Dec 17 2018EMU Trade Shows Some Trade Flow Rebound

Summary

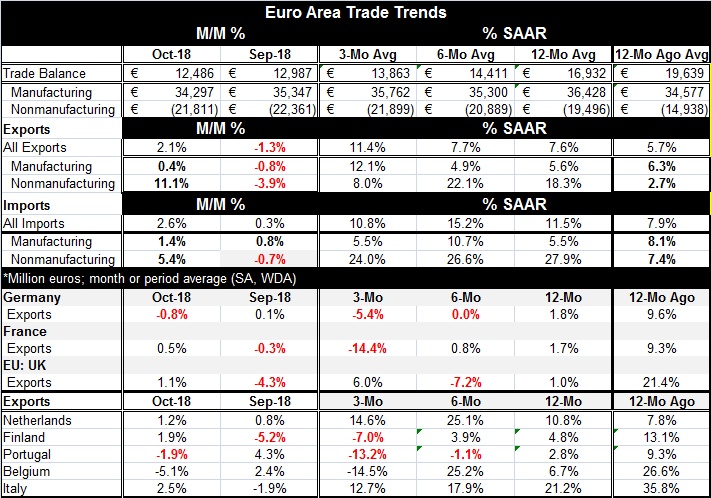

Trade flows are rebounding on differing dynamics in the euro area. The aggregate results (see Chart) show year-on-year flows sharply higher in October compared to the previous month's rate of growth. Monthly changes show solid gains [...]

Trade flows are rebounding on differing dynamics in the euro area. The aggregate results (see Chart) show year-on-year flows sharply higher in October compared to the previous month's rate of growth. Monthly changes show solid gains for both exports and imports in some cases representing a rebound from a September decline. However, over three months both exports and imports log double-digit growth. For exports it's an acceleration but not for imports.

Trade flows are rebounding on differing dynamics in the euro area. The aggregate results (see Chart) show year-on-year flows sharply higher in October compared to the previous month's rate of growth. Monthly changes show solid gains for both exports and imports in some cases representing a rebound from a September decline. However, over three months both exports and imports log double-digit growth. For exports it's an acceleration but not for imports.

Manufactured goods exports show a double-digit gain over three months that is stronger than their six-month and 12-month rates of growth. For imports, manufactures have a growth rate in single digits that is the same as or below its six-month and 12-month rates of expansion.

Nonmanufacturing exports show an uneven slowing progression with the three-month pace dipping into single-digits. Nonmanufacturing imports demonstrate a steady, strong, double-digit rate of expansion on all horizons.

As a result of these divergent export and import trends, the EMU finds its manufactures trade position only a slight bit weaker month-to-month and still well in line with past levels of surplus. For nonmanufactures the deficit is a slight bit lower in October and is broadly in line with its three-month and six-month average but is larger than its 12-month average and its year-ago average.

The larger deficit for nonmanufactures reflects higher costs for energy and commodities while for manufactured goods the trade position for the EMU has not changed very much at all over the last 12 or last 24 months.

Results for some individual members reside in the lower portion of the table. There we see that all listed members show exports are rising year-on-year. But over three months, Germany, France, Finland, Portugal, and Belgium each show declining exports. Over six months, exports are flat or lower in Germany, the U.K., and Portugal and are decelerating in France, Finland, and Italy (although Italian exports are still quite strong over six months).

On balance, European trade trends do not show any clear sign of impact from trade war or trade concerns. There are some flow declines and some slowing, but individual countries differences are not unusual; there is nothing going on in unison as we might expect from one common negative shock like a trade war. The Baltic dry goods index of international shipment volumes has come off its highs and shown some weakness but has stabilized. The EMU region as a whole shows no tendency for either exports or imports to wither; in fact, exports and imports are on the rebound in October and their year-on-year pace solid for manufactures as well as for nonmanufactures.

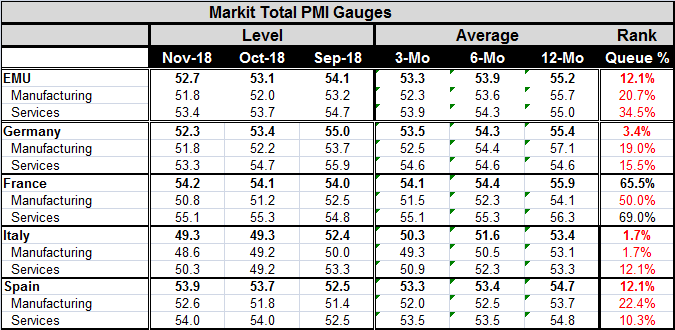

However, the manufacturing sector for EMU is weakening and the overall PMI indexes show weaker growth. When ranked against their performance back to January 2014, the current gauges are weak and reside below their median values in almost all cases for the EMU's largest members. In fact, most are even weaker at or below their respective 20th percentile (giving off readings that reside in the lower one-fifth of what we have been used to since January 2014). Still, as of November, only Italy has raw PMI readings below 50 and that is for manufacturing and the overall PMI. Still, for all of the EMU, the total PMI, at a diffusion value of 52.7, is in the lower 12th percentile of its recent range of values back to 2014 and its manufacturing reading stands in its 20th percentile with services in their 34th percentile. The relatively and substantially lower standing for the composite PMI indicates the unusual nature of the joint weakness in manufacturing and services in the same month. That does not speak of trade war effects either; it speaks of old fashioned weakness.

As the year winds down and as trade tensions percolate and as central banks craft their year-end strategies and look to 'normalize' their future operations, there is a lot in the mix. Europe is beset by more than just trade fears. Brexit has battered at the U.K. while Italy continues to argue about its allowable fiscal deficit. The EU Commission has no compassion for a country that has complied with its laws for a decade while its GDP has failed to grow and whose real GDP is lower on balance over the last decade! No wonder the Italian electorate is up in arms and has voted into office a 'renegade' government to fight the EU. Now the 'yellow vests' pose a threat for France and it will be out of budget compliance too.

Meanwhile, the geopolitical environment has hardly stabilized as Russian aggression in the Sea of Azov looks like a step up in operations not just a one-off event. In the U.S., the President faces nearly unprecedented opposition and legal threats but so far appears unfazed by any of it. In fact, the media seem more concerned about it than the President himself. In Europe, the Germans are shifting to new political leadership and Brexit seems finally to be gnawing at the last vestiges of support for Prime Minister May who has done her best to carry the will of the people's Brexit plans forward. France is hard to handicap. Conditions in China have eroded enough that some wonder if China could slow enough to undermine the leadership position of Xi Jinping.

As I said, there is a lot in the mix and slowing economic conditions are in the center of the storm but do not constitute the whole of the storm by any means. As 2018 draws to a close, its troubles are not and may only be coming to a head.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief