Global| Aug 18 2014

Global| Aug 18 2014EMU Trade Posts Lower Surplus

Summary

Geopolitical news is starting to take its toll on European Monetary Union data. But we are not seeing these effects in June trade flows. The confrontation in Ukraine began six months ago, but the imposition of sanctions is a much more [...]

Geopolitical news is starting to take its toll on European Monetary Union data. But we are not seeing these effects in June trade flows. The confrontation in Ukraine began six months ago, but the imposition of sanctions is a much more recent phenomenon. The downing of the Malaysian airliner on July 17 was the catalyst for European sanctions to get tougher. So we should not expect to find any impact of sanctions in June data. Still, at that time, there were considerable worries about where things were headed. Total EU exports to the Russian Federation are about 7% of overall EU exports.

Geopolitical news is starting to take its toll on European Monetary Union data. But we are not seeing these effects in June trade flows. The confrontation in Ukraine began six months ago, but the imposition of sanctions is a much more recent phenomenon. The downing of the Malaysian airliner on July 17 was the catalyst for European sanctions to get tougher. So we should not expect to find any impact of sanctions in June data. Still, at that time, there were considerable worries about where things were headed. Total EU exports to the Russian Federation are about 7% of overall EU exports.

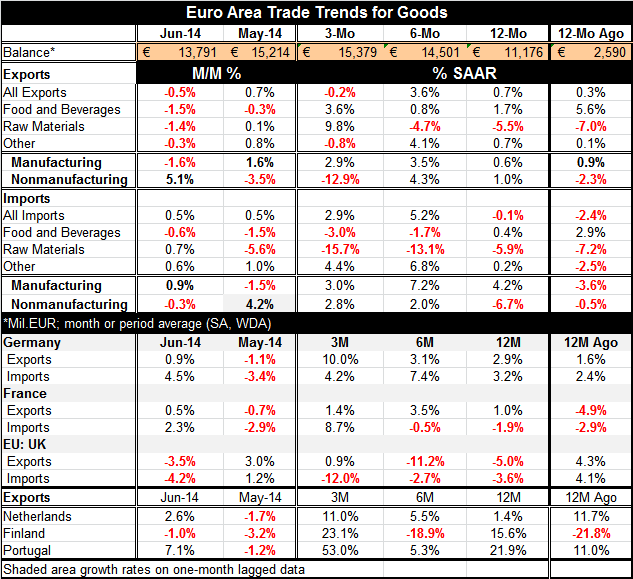

The June trade report from the EMU shows a smaller surplus at 13.791 billion euros in June, down from ?15.214 billion euros in May. Exports in June fell by 0.5% after a 0.7% rise in May. Imports in June rose by 0.5% after a 0.5% rise in May. Exports continue to outpace imports. Over 12 months, exports are growing by 0.7% and imports are falling by 0.1%. Exports are outpacing imports but neither flow is impressive.

The European Union today decided to make payments to fruit and vegetable growers who are hurt by the Russian sanctions. EU agricultural exports have been about 7% of total exports and EU agricultural exports to Russia are 10% of this (0.7 percentage points). The share of total EU exports that goes to Russia is small.

The Bundesbank today said that because of geopolitical effects on the outlook Germany may not have its formerly expected rebound in the second half of the year.

Geopolitical effects on European growth economic data are now undeniable, as the EU is paying for damages. It's still not clear how large and the disruption will get to be. However, European trade with Russia is simply not that large and should not turn into a rout on European growth. We expect the impact of sanctions on European growth to appear to be the greatest in the first two quarters after the sanctions are imposed. Part of this is because we will see the largest impacts then, and once annualized, the impacts still seem to be even larger. However, the subsequent impact on European growth rates will be less in the following quarters. Our warning is that the early view of the impact on growth should appear much bigger than it ultimately will turn out to be so try not to be spooked by that.

The detailed trade data from the euro area shows that exports are declining across all the major categories in June: food exports, raw materials exports, and other exports. Overall imports rose in June as food and beverage imports fell but there were increases in raw materials imports and other imports. Manufacturing goods exports fell by 1.6% in June as nonmanufacturing exports rose by 5.1%. For imports, manufacturing imports rose by 0.9% while nonmanufacturing imports fell by 0.3%.

The country detail at the bottom of the table shows that German exports are growing. They grew by 0.9% in June after a 1.1% decline in May. The three-month annualized growth rate is a very strong 10% compared to the 12-month growth rate of 2.9%. Still, imports outpaced exports in June and imports rose by a strong 4.5% in June. But that surge followed a 3.4% decline in May.

In France, exports rose by 0.5% in June with imports up a stronger 2.3%. French imports are showing progressively stronger growth, advancing by 8.7% at an annual rate over three months while exports are floundering and growing only at a 1.4% annual rate over three months.

The UK is not in the single currency area. In June, its imports fell by 4.2% and exports fell by 3.5%. UK sequential import growth rates show progressive weakness, falling at a 12% annual rate over three months. The UK exports are contrarily turning around from negative growth rates to post a 0.9% annual rate of growth over three months.

Exports in the Netherlands, Finland in Portugal show mixed patterns with the Netherlands exports up by 2.6% in June and Portuguese exports up by 7.1%. Finland's exports fell by 1% in June. Finland is another one of those countries that trades intensively with Russia. Its exports are down for two consecutive months. However, Finnish exports are up at a 23% annual rate over three months. Portuguese exports are up at a 53% pace over three months. In the Netherlands, exports are up at an 11% pace over three months. The Baltic countries of Lithuanian and Estonia (whose trade flows not shown in the table here) are candidates to be hit hard by sanctions, once they bite.

From the latest trade data, we see some slowdown in Europe with exports and imports more or less plugging along. The euro area trade surplus drops a little bit month-to-month but continues to expand year-over-year. The pace of the aggregate trade flows is weak. The EMU members we expect to be most affected by the sanctions are still showing firm-to-strong recent export growth. This is something to bear in mind when we begin to look for the impact of sanctions. There may be some extra exporting to try to get in under the wire in the event that sanctions were imposed (as they finally were). It is important to remember that there're other trends going on in Europe and that Europe has been fighting to increase growth for some time. The European Central Bank has a special lending program in place. We may not be able to pin down the effect of sanctions when it first shows up, but we expect the sanctions have a bigger impact on these numbers in the coming months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief