Global| Apr 17 2009

Global| Apr 17 2009EMU Trade Deficit Improves But Picture Does Not

Summary

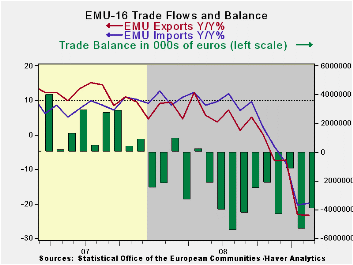

Trends are getting worse. The EMU trade deficit improved in February on a tiny rise in exports as imports continued to drop. Even though both exports and imports put in an ‘improved performance’ in February compared to January the [...]

Trends are getting worse. The EMU trade deficit improved in February on a tiny rise in exports as imports continued to drop. Even though both exports and imports put in an ‘improved performance’ in February compared to January the trends in trade for exports and imports are still deteriorating and nearly in step. Export and import annual growth rates are accelerating in a downward direction as three-month growth rates show faster decline than six-month rates and six-month growth rates are declining faster than the 12-month rates. The pace of decline over three months for both exports and imports is over 40%. It is far from clear that the abatement in the pace of decline for exports and imports in February is for real. It may simply be a partial recovery from the deep decline in January.

A balanced blow. The chart shows how rapidly trade flows decelerated after September of last year. But that impact was BALANCED, hitting exports and imports nearly equally. Deficit deterioration had already reached its then-worst level in July of 2008. The slowdown is global in nature; it has hit growth within the e-Zone as well as outside of it more or less equally. Trade trends show that. The monthly growth rates show a hint of slowing. The year/year rates of growth have improved, but the sequential growth rates are still deteriorating for both exports and imports. It will take a few more months to see if we have reached low enough levels that export and imports can begin to build a base for improved future growth.

No improvement in the fundamentals. Certainly there are no economic signs

yet that point to improvement. PMI surveys have made very modest

improvements from their worst levels but even they continue to signal

contraction. Industrial production and orders continue to show sharp

deterioration. Unemployment is still rising. Retail spending remains

weak. There is no grass-roots European growth. European fiscal plans

have been less ambitious than in the US . So, there is little basis for

optimism. For now we are left to watch the trends in the trade flows

themselves.

| E- Area 16-Trade trends for goods | ||||||

|---|---|---|---|---|---|---|

| m/m% | % Saar | |||||

| Feb-09 | Jan-09 | 3M | 6M | 12M | 12M Ago | |

| Balance* | €€ (3,961) | €€ (5,356) | €€ (3,507) | €€ (3,265) | €€ 1,010 | €€ (1,119) |

| Exports | ||||||

| All Exp | 0.5% | -11.9% | -44.3% | -37.6% | -23.3% | 9.4% |

| Food and Drinks | -2.9% | -5.2% | -28.1% | -19.4% | -13.8% | 13.0% |

| Raw materials | -2.8% | -6.9% | -34.3% | -53.1% | -33.8% | 18.3% |

| Other | 0.8% | -12.5% | -45.6% | -38.4% | -23.7% | 9.0% |

| MFG | 0.7% | -12.9% | -42.6% | -37.6% | -25.2% | 7.9% |

| IMPORTS | ||||||

| All IMP | -0.8% | -8.3% | -43.9% | -36.9% | -19.8% | 8.7% |

| Food and Drinks | -0.2% | -5.7% | -18.8% | -17.3% | -9.6% | 8.4% |

| Raw materials | -5.3% | -26.2% | -81.1% | -60.8% | -35.1% | 1.3% |

| Other | -0.7% | -7.4% | -42.3% | -36.6% | -19.7% | 9.1% |

| MFG | -3.5% | -6.1% | -42.0% | -33.6% | -20.3% | -0.5% |

| *Eur mlns; mo or period average | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief