Global| Mar 17 2016

Global| Mar 17 2016EMU Trade Balance Withers As Do Exports and Imports

Summary

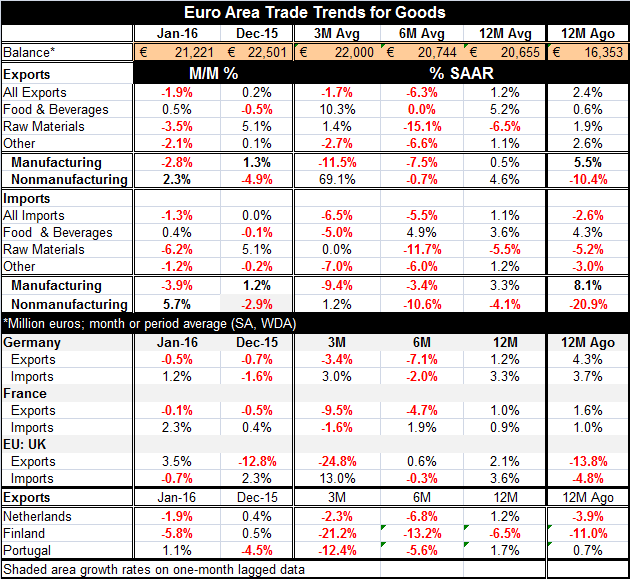

The EMU trade balance shrank in January and stands a tick below its three-month average. Exports have fallen in January and are lower over three months and six months but higher by 1.2% over 12 months. Imports are lower in January, [...]

The EMU trade balance shrank in January and stands a tick below its three-month average. Exports have fallen in January and are lower over three months and six months but higher by 1.2% over 12 months. Imports are lower in January, also lower over three months and six months, but higher over 12 months. Both exports and imports show progressive deterioration in their 12-month to six-month to three-month rates of growth. This is double-barreled trouble.

The EMU trade balance shrank in January and stands a tick below its three-month average. Exports have fallen in January and are lower over three months and six months but higher by 1.2% over 12 months. Imports are lower in January, also lower over three months and six months, but higher over 12 months. Both exports and imports show progressive deterioration in their 12-month to six-month to three-month rates of growth. This is double-barreled trouble.

This progressive export and import shrinkage speaks of weakening global growth as well as a weakening of growth within the euro area itself. Of course, on the import side, there is a downward distortion because these are nominal flows and oil prices are falling. But EMU exports and imports of manufactured goods alone show the same progressively deteriorating trends with negative growth rates over both three-month and six-month. Exports post a tiny 0.5% rise over 12 months, while manufactured imports are up a more robust 3.3% over 12 months. Still, the patterns are weak. The flows are weakening. Those trends also are made clear in the chart. There simply is not much room for prevarication here.

Some country patterns

Germany, France, the U.K., the Netherlands, Finland and Portugal, all early trade reporters in the table, show exports dropping over three months. All of these except the U.K. (+0.6%) show exports falling over six months as well. Year-over year growth is at or under 2% over 12 months (2.1% for the U.K.). These are impressively weak and uniform patterns. And all of this is from an area that continued to have a weak exchange rate that should cause its EMU members (Germany, France, the Netherlands, Finland and Portugal) to benefit from exchange rate competitiveness. The British pound sterling has been separately weak too.

The meaning of an easier Fed policy path

Markets today are walking on eggshells in the wake of an unexpected pullback from the tightening path announced by the Federal Reserve in the U.S. at yesterday's FOMC meeting. The pullback was much more severe than expected and it shocked many in markets. It is causing some reappraisal about what the Fed might be looking at. There have been reverberations in global markets from the Fed move. But with inflation in the U.S. finally showing some life (core inflation, not headline), the Fed did not take the step to reinforce its direction it backed off. And since all the conditions seemed right for that next step, there is a quandary among market watchers about what exactly the Fed has seen. Was it a ghost?

Second guessing why the Fed moved

Is there weakness that we have not yet seen publically? Or has the Fed suddenly discovered that U.S. data outside of head-count job data have been weakening for some time? The Fed manufacturing surveys for March from NY and Philadelphia actually improved month-to-month. Is there something on the international front? The European trade data show this shrinking in global trade growth trend and that is disturbing right there. The Baltic dry index has been anemic for some time. Oddly, oil prices are getting a bid despite the ongoing glut of oil and Iran's clear opposition to being part of any output restricting deal. Still, OPEC has a meeting scheduled and markets are wary of OPEC and `friends'. In the wake of the Fed meeting yesterday, gold prices absolutely soared. Markets think where there is smoke there is fire. Is there? If so, who or what is `on fire?' And by that, I do not mean who has a hot economy; I mean where is somebody's house burning down?

Dealing with Fed-inspired anxiety

When a central bank that had thrown caution to the wind and had gone its own way suddenly pulls back into its shell markets sit up and take notice. Did the Fed simply take a detour to prudence and away from aggression? Was its hand forced by the recent BOJ and ECB policy actions? Fed Chair Yellen says `no.' But would she really tell us? Markets will be scouring incoming data across the globe for a clue. So far nothing (new) that is obvious has emerged. But it is worth staying alert. The sudden shift by the Fed, the impact on the dollar, the surge in gold and the odd firmness in oil prices are all newsworthy events. Now if we could really nail down the cause, we would be in business. Instead, we are in a state of anxiety.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief