Global| Nov 17 2009

Global| Nov 17 2009EMU Trade Balance Improves

Summary

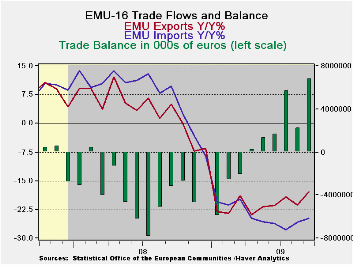

The EMU trade surplus continued to grow as exports rebounded strongly from a lackluster August that saw them fall by 4%. In September exports are back up, and off to the races. Exports contribute to growth overallEMU exports now are [...]

The EMU trade surplus continued to grow as exports rebounded strongly from a lackluster August that saw them fall by 4%. In September exports are back up, and off to the races.

Exports contribute to growth overallEMU exports now are off by 17.8% Yr/Yr, better than the 24.8% drop for imports. To this point the larger relative drop in imports makes the EMU trade sector a contributor to growth.

Exports are looking solid again Over recent months the contribution of exports to growth is looking even stronger- like a real force instead of a bit of subtle arithmetic. Over six months exports are rising at an 8.3% pace and over 3-months the growth rate is 25.6%. These metrics compare to import annual ‘growth’ rates of -8.5% over six months and of +3.4% over three months. Obviously EMU-region domestic demand is lagging in its developing as imports are still falling rapidly or barely heading higher depending on the period for that calculation. Meanwhile EMU exports are exploiting demand revival elsewhere.

Category-wide rebound in exportsAfter seeing declines across most key categories in August exports showed strong sharp category-wide improvements in September. Imports had a less widespread drop in August but are experiencing some revival in September as well.

Déjá vu all over again?EMU, like China and like Japan, is seeing a revival of export led growth. While China is being lauded for its huge domestic stimulus program at the end of the day it is a net exporter, its surplus is growing, so it is getting stimulus from overseas. Meanwhile the US trade deficit popped up in the wake of surging oil imports and auto imports that came on the heels of its cash for clunkers auto sector stimulus program. Even though the US consumer is late to revive in this cycle foreigners have been quick to glean whatever spoils there are in the US market. All this smacks of business as usual. If the global economy is to be made safer, business as usual will have to change its stripes. Europe, Japan and China if they are to hold their exports focus will have to find markets other than the US to exploit or it will be déjá vu all over again, as that sage Yogi Berra once said.

Ezone Trade Trends For Goods| m/m% | % Saar | |||||

| Sep-09 | Aug-09 | 3M | 6M | 12M | 12M Ago | |

| Balance* | € 6,801 | € 2,235 | € (6,433) | € 2,976 | €(3,092) | € 1,842 |

| Exports | ||||||

| All Exp | 5.5% | -4.1% | 25.6% | 8.3% | -17.8% | 4.9% |

| Food and Drinks | 2.8% | -5.1% | 3.9% | 0.3% | -10.2% | 11.6% |

| Raw materials | 1.7% | -5.0% | 12.6% | 9.1% | -14.7% | 2.2% |

| Other | 5.8% | -4.0% | 27.8% | 9.0% | -18.5% | 4.6% |

| MFG | 2.6% | -6.4% | 13.5% | -5.4% | -21.7% | 1.6% |

| IMPORTS | ||||||

| All IMP | 1.1% | -1.0% | 3.4% | -8.5% | -24.8% | 9.7% |

| Food and Drinks | 1.2% | -2.6% | -1.5% | -17.1% | -10.7% | 1.5% |

| Raw materials | -1.2% | 3.9% | 19.8% | -7.4% | -39.4% | 14.5% |

| Other | 1.2% | -1.0% | 3.2% | -7.9% | -24.9% | 10.0% |

| MFG | 1.3% | -1.4% | 3.3% | -12.7% | -20.4% | 0.5% |

| *Eur mlns; mo or period average | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief