Global| Mar 18 2021

Global| Mar 18 2021EMU Trade Balance Erodes in January

Summary

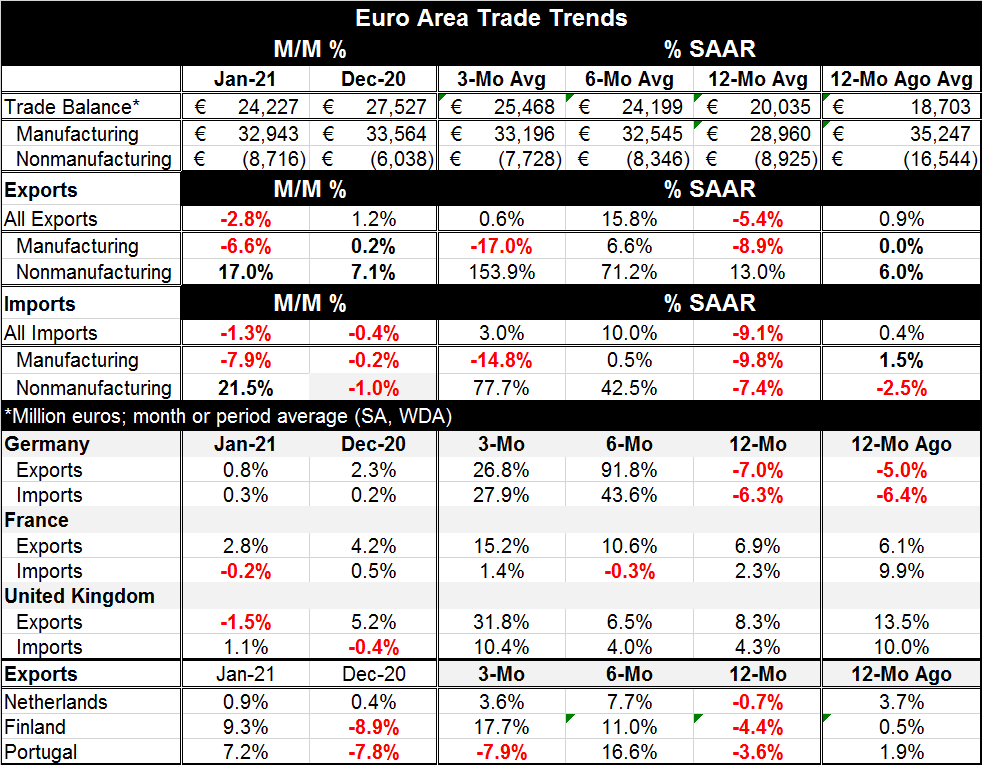

The EMU trade balance saw its surplus erode in January, falling to €24.2bln in January from €27.5bln in December. Exports fell harder than imports to drive this result. Exports fell by 2.8% while imports fell by 1.3% (both month-to- [...]

The EMU trade balance saw its surplus erode in January, falling to €24.2bln in January from €27.5bln in December. Exports fell harder than imports to drive this result. Exports fell by 2.8% while imports fell by 1.3% (both month-to-month) in January. Both flows showed weakness in manufacturing as exports of manufactures fell by a large 6.6% compared to imports where manufactures imports fell even faster by 7.9%. However, it was the greater import surge in nonmanufacturing that kept overall imports stronger than exports in January as nonmanufactures rose by 21.5% compared to exports where they rose by 17.0%.

The EMU trade balance saw its surplus erode in January, falling to €24.2bln in January from €27.5bln in December. Exports fell harder than imports to drive this result. Exports fell by 2.8% while imports fell by 1.3% (both month-to-month) in January. Both flows showed weakness in manufacturing as exports of manufactures fell by a large 6.6% compared to imports where manufactures imports fell even faster by 7.9%. However, it was the greater import surge in nonmanufacturing that kept overall imports stronger than exports in January as nonmanufactures rose by 21.5% compared to exports where they rose by 17.0%.

EMU trade flows are not showing much trend at the moment. The graphic shows that both exports and imports have been improving their year-on-year performance by cutting their percentage rates of decline steadily, but that trend peaked and now both flows are slowing and falling at a faster pace. Sequential growth rates for trends of one year and less fail to reveal any meaningful patterns in manufacturing trends. Overall exports fall over 12 months, rise strongly over six months then barely make any gain at all over three months. Imports follow roughly the same pattern. Manufactures trade shows both exports and imports falling over 12 months rising, over six months then falling over three months. Contrarily, nonmanufactures do show a pattern of acceleration for both exports and imports, with exports outpacing nonmanufacturing imports on all three horizons. These nominal flow growth rates are dominated by spurting oil and commodity prices.

Germany and France also show mixed trends over 12 months, six months and three months. For Germany exports fall over 12 months then post two months of gains but the gains slow over three months. The same pattern holds for German imports. In France, export growth steadily accelerates culminating in a 15.2% growth rate over three months while over the same period French imports remain weak; they oscillate between growing and shrinking.

Adding other EMU countries, the Netherlands, Finland and Portugal, into the mix shows uneven trends. Two (the Netherlands and Finland) show patterns similar to Germany's with exports falling over 12 months then growing over six months and three months. The Netherlands' pattern mimics Germany's, with exports weakening over three months (compared to six months) while in Finland exports accelerate over three months compared to six months. Portugal shows two declines on the three horizons, posting a drop in exports over 12 months and again over three months. Overall, the patterns are messy; meaningful trends are nonexistent.

The United Kingdom is no longer an EU member; it displays growth on all horizons for both exports and imports. Sequential growth rates do not technically accelerate in the U.K., but export and import growth rates do not slow much over six months and then three-month growth for both exports and imports is higher than the two previous horizons. U.K. trade flows seem reasonably healthy despite what are reported border issues in the wake of Brexit and its new trading relations with the EMU. However, U.K. exports did fall in January as imports rose.

The EMU is not showing very clear trends. The year-on-year trend in the past was relatively smooth and clear as both exports and imports steadily reduced their negative growth rates. But in the last few months, that process seems to have played out. It is no longer clear that forward momentum is present or not. EMU imports show some pronounced weaknesses in December and January. Exports log only one month of decline and that was confined to manufacturing goods. The virus continues to be a factor in Europe, but trade and manufacturing has been resistant to the the virus which has had its greatest negative impact on the service sector. Still, when services are impacted so are jobs and aggregate demand creating collateral damage the manufacturing sector cannot fully escape. However, the news and trends in trade are worth keeping an eye on since vaccination progress in the EMU has been slow. In contrast, the U.K. vaccine program has been expedited because of its fear of its circulating and dangerous variant.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief