Global| Aug 05 2014

Global| Aug 05 2014EMU Total PMIs Edge Higher

Summary

In July the composite PMI for the European Monetary Union rose to 53.8 from June's 52.8. This represents a slight backtracking from the preliminary value. Moving averages over 12 months, six months and three months show progress from [...]

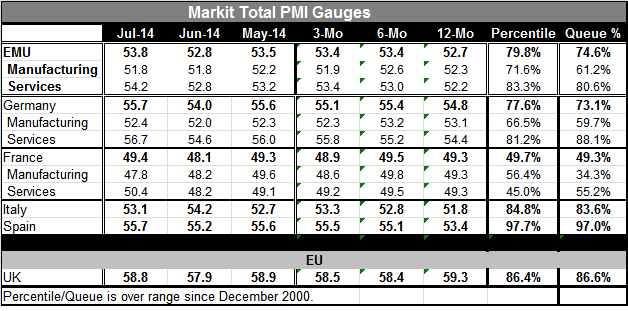

In July the composite PMI for the European Monetary Union rose to 53.8 from June's 52.8. This represents a slight backtracking from the preliminary value. Moving averages over 12 months, six months and three months show progress from 12 months to six months and then a flattening in the PMI values over three months. The overall queue standing of the EMU PMI is in its 74th percentile. Manufacturing stands in its 61st percentile and services stand in their 80th percentile. As the chart shows, the manufacturing sector has been backtracking while services have been carrying the gains for a number of months. For the EMU, Germany and France, services have become the leading sector.

In July the composite PMI for the European Monetary Union rose to 53.8 from June's 52.8. This represents a slight backtracking from the preliminary value. Moving averages over 12 months, six months and three months show progress from 12 months to six months and then a flattening in the PMI values over three months. The overall queue standing of the EMU PMI is in its 74th percentile. Manufacturing stands in its 61st percentile and services stand in their 80th percentile. As the chart shows, the manufacturing sector has been backtracking while services have been carrying the gains for a number of months. For the EMU, Germany and France, services have become the leading sector.

Germany saw its overall PMI value rise to 55.7 in July from 54 in June. The moving averages in Germany's PMI show a backtracking from six months to three months; Germany's PMI did advance from six months compared 12 months. The overall German PMI sits in the 73rd percentile of its historic queue. In July, Germany's manufacturing and services PMIs both advanced compared to June values. Manufacturing, however, shows a setback in its three-month moving average compared with its six-month average. Meanwhile the German services PMI shows steadily improving averages over 12 months, six months and three months. As is the case for overall EMU, services are leading Germany to better growth. Germany's manufacturing standing is in its 59th percentile while its services standing is much stronger in its 88th percentile.

France saw a rebound in its composite PMI in July compared to June; it rose to 49.4 from 48.1. France's PMIs are below breakeven for its three-month, six-month and 12-month averages. Although France has a small improvement in its PMI from 12 months to six months, it also experiences a sharper decline from six months to three months. The queue standing of France's overall PMI is in its 49th percentile. France's manufacturing PMI fell in July while its services PMI improved significantly and even showed expansion. France's manufacturing PMI stands in the 34th percentile of its historic queue while services stand in the 55th percentile.

Italy registered a backtracking in its composite PMI in July as it fell to 53.1 from June's 54.2. Still, Italy's PMI averages improve from 12 months to six months to three months. Its composite PMI sits in its 83rd percentile of its historic queue.

Spain shows an improvement in July relative to June and it shows the sequence of rising PMI averages from 12 months to six months to three months. Spain's composite PMI stands at a strong 97th percentile of its historic queue.

The U.K. is not part of the single currency mechanism, but its composite PMI improved in July compared to June although it still stands a tick below its May value. The U.K.'s moving averages of its composite PMI register a decline from 12 months to six months. There is a very small increase in three-month PMI compared to the six-month average. The U.K. has little momentum; however, its composite PMI sits in the 86th percentile of its historic queue, a relatively strong value.

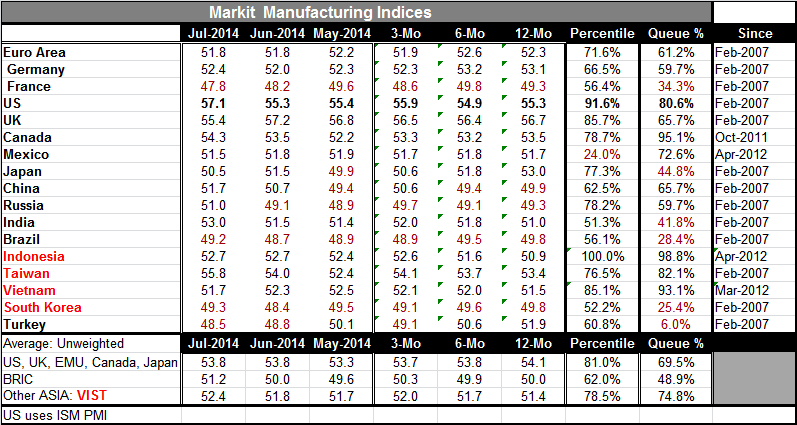

In addition to the finalized July readings for the EMU, it's interesting to look at the global readings for manufacturing from Markit for the month of July. Of the 17 countries in the table, 9 show month-to-month improvement in their three-month averages compared to their respective six-month averages. Eight show improvement in their three-month averages compared to their respective 12-month averages. Clearly this has been a time when the global recovery has been slowing. However, it doesn't look like recovery is stalling, since only five countries have PMI readings below 50 over three months and only four have PMI readings below 50 in July. What we are experiencing is a slowdown rather than a backtracking.

At the bottom of the second table below, I've created three groups of countries, one including the U.S., U.K., EMU members, Canada and Japan. The second consists of the members known as the BRICs. The third group includes other Asia, a unit all identified by the acronym VIST (Vietnam, Indonesia, South Korea, and Taiwan).

The group including the U.S. and EMU shows a small erosion in its manufacturing PMIs from 12 months to six months to three months. The BRIC group shows manufacturing values of below 50 for six-month and 12-month averages and then experiences a creep up to just above 50 for its three-month average. The VIST group shows a very slow expansion in its moving averages that starts at 51.4 over 12 months and edges up to 52 over three months. However, when we look at the queue standings we get this picture: the BRIC countries in the 48th percentile of their historic queue, a weak standing. The group of the U.S. and EMU posts a 69th percentile queue standing which is moderately strong. The VIST group has a queue standing in the 74th percentile, also a moderately strong reading. None of these groups, however, shows much momentum.

These results basically confirm the view that we have of the U.S. and Europe still struggling. However, some U.S. data have turned a bit more upbeat while Europe has logged a 12-month rise in retail sales volume of just 0.6%, a very moderate gain, and with inflation still sinking. Japan is still trying to shake off its period of deflation. The BRICs are still in a period of struggling. Russia is grinding but not deteriorating in the face of sanctions. China continues to wrestle with its attempt to stimulate domestic demand to supplant its aggressive export strategy. While Indonesia seems to have the highest PMI standing, it today just announced its weakest GDP quarter since 2009.

It seems to be a time when the world economy doesn't have any real growth leadership. Meanwhile, the U.S. is getting ready to transition from a period of extra monetary assistance to one in which monetary policy will become less accommodative. The U.K may be hot on its heels. But the European Central Bank has just stepped up its monetary accommodation. It is on balance a difficult time for the global economy made worse by heated up geopolitical considerations and by monetary policies that are flirting with excesses.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief