Global| Feb 04 2015

Global| Feb 04 2015EMU Total PMI Advances on Strength in Spain

Summary

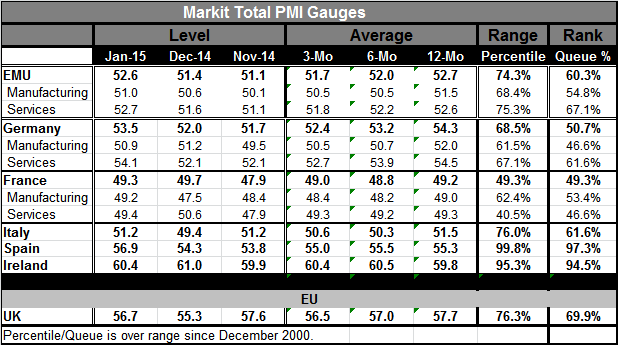

The EMU total PMI showed an advance for January but still in the context of sequential declines from its 12-month to 6-month to 3-month averages. Sequential decline also applies to the two EMU components for services and manufacturing [...]

The EMU total PMI showed an advance for January but still in the context of sequential declines from its 12-month to 6-month to 3-month averages. Sequential decline also applies to the two EMU components for services and manufacturing as well as to Germany's total PMI and its two components. France is just mostly flat with manufacturing and services readings each skimming just below 50, showing minor but enduring contraction.

The EMU total PMI showed an advance for January but still in the context of sequential declines from its 12-month to 6-month to 3-month averages. Sequential decline also applies to the two EMU components for services and manufacturing as well as to Germany's total PMI and its two components. France is just mostly flat with manufacturing and services readings each skimming just below 50, showing minor but enduring contraction.

The situation in the EMU is not unraveling; it is just in a slow decay for the most part but with the recent strength coming from outside the three largest EMU economies.

Spain has the highest ranking for its total PMI gauge among the biggest four economies. Spain's raw 56.9 diffusion reading has been higher less than 3% of the time historically. Ireland, a small economy, also shows strength with a total PMI gauge that is stronger only about 5% of the time. These strong standings compare to the EMU wide total PMI that is in its 60th percentile, a firm sort of reading. The German total PMI is at only its 50.7th percentile and the French reading is below its median with a queue standing in its 49th percentile. Italy, the third largest EMU economy, with a raw diffusion reading of only 51.2, finds it with a standing in its 61st percentile. Italy's percentile standing looks relatively firm in the 60s, but its raw reading at 51.2 has a tenuous grip on expansion. On balance for the EMU, the strong countries are the smaller ones and the large economies are the weaker ones.

Both the EMU and Germany have relatively stronger queue standings in their services sectors than in their respective manufacturing sectors. With the euro exchange rate falling so consistently, that should shift strength to manufacturing. Perhaps the period in which Russian sanctions were imposed hit hard in Europe. But now time has passed and the lower euro exchange rate should help to stimulate manufacturing- tradable goods- across the euro area, at least in terms of trade with regions outside the EA. That part of trade should improve.

So these are some of the themes we will be watching. Will the smaller countries continue to be the stronger ones? Will the goods sector begin to take over and dominate the services sector? Will the euro continue to weaken? We expect so.

Looking ahead, we also are concerned with how the Greek situation plays out. The Greek first approach was stone walled by EMU members and official organizations. Now the Greeks are sending teams around to talk. We don't know what their message is. The EMU - Germany especially- is in no mood of cutting Greece any slack if it does not stick with the austerity program. But the Greek election was won on a promise to end them. So there is an impasse.

There is also the question of how the ECB's QE program will unfold and work. QE tends to have subtle effects. There has been some late stirring in EMU money and credit growth ahead of the QE adoption, but it is too soon to know if that is real and if QE has any sort of base or trend to build upon since money and credit growth in the EMU have been weak for so long. Moreover, we continue to think that Europe's dependence on universal banks, coupled with their troubles and the ECB's pushing them to raise more capital, will keep the ECB's message more mixed than true. The ECB and Mario Draghi in public mostly talk of stimulus and QE. Draghi is famous for saying he will do whatever it takes, but at the same time, he is doing what makes banks ache. He is forcing them to raise more capital and that will not make them want to lend more to riskier credits as the ECB's agent regional banks scoop the high-rated credits (sovereign bonds- at least in some cases) out of the market. QE simply has flawed mechanics in Europe. It will not work as well as it did in the United States. Still, we are waiting to see what it does, not just to prejudge it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief