Global| Jan 13 2017

Global| Jan 13 2017EMU Surpluses and Trump Trade-o-nomics; Food for thought on Friday the 13th

Summary

Every picture tells a story, don't it? Bad grammar? Yes, but a truism nonetheless. The chart on the left pictures the German and EMU current accounts as a percentage of GDP. Since late 2000, these values have been positive indicating [...]

Every picture tells a story, don't it? Bad grammar? Yes, but a truism nonetheless. The chart on the left pictures the German and EMU current accounts as a percentage of GDP. Since late 2000, these values have been positive indicating surpluses for both Germany and for the EMU as a percentage of GDP. Of course, the German surplus is a good part of the EMU surplus (and German GDP is a good part of the denominator, EMU GDP, as well).

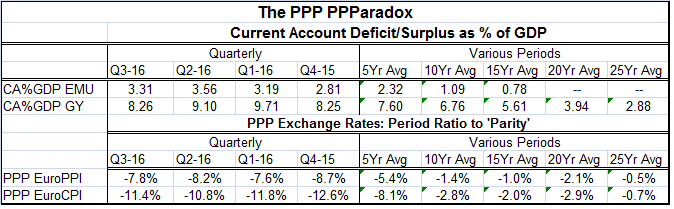

Every picture tells a story, don't it? Bad grammar? Yes, but a truism nonetheless. The chart on the left pictures the German and EMU current accounts as a percentage of GDP. Since late 2000, these values have been positive indicating surpluses for both Germany and for the EMU as a percentage of GDP. Of course, the German surplus is a good part of the EMU surplus (and German GDP is a good part of the denominator, EMU GDP, as well).

The not-good unsustainable and dangerous

The table shows various moving average views of the current account to GDP percentage for Germany and the EMU. What is clear is that the current account surplus as a percent of GDP has generally been growing for both Germany and the EMU. Individuals may have biases or preferences when looking at a series like this, but to an economist over the long haul we prefer to see the external account in balance not in either persistent surplus or deficit. The old expression 'neither a borrower nor lender be' comes to mind. Some prefer a country to run surpluses because a surplus is a sign of economic strength and of ongoing asset accumulation. But that is exactly the problem. In a global environment we need balance. One country's desire to run persistent surpluses puts the rest of the world in a position to have to run a net deficit to accommodate it. It is often thought that deficit countries are weak or have weak economies. And certainly it is the deficit country that has balance of payments problems when their deficits are too big or too protracted. But the U.S. currency is the world's principal reserve asset and the U.S. runs almost never ending deficits. Since exchange rates were set to fluctuate in the early 1970s, the U.S. current account has been in surplus only 16% of the time. And the historic surpluses are small while the deficits have come to be quite large and persist and a permanent fixture since the early 1980s. That is not good, not sustainable, and dangerous.

Beggar thy neighbor

I mention this because there is this other expression 'beggar thy neighbor.' And when countries choose to run surpluses against a particular country, they leave that particular country with deficits. So 'one man's strength breeds another's weakness.' This is what has happened to the U.S. All too many countries have 'chosen' to run surpluses against the U.S. by 'pegging' their currencies 'too-low.'

Exchange rate theory gone to pot

Exchange rate theory gone to pot

According to exchange rate theory, if exchange rates were left to fluctuate on their own (i.e., without government interference), we would expect the currency of a surplus country to appreciate (think Germany and the EMU) and the currency of a deficit country to depreciate (think the United States of America). But this is not happening. In fact, the data show that the EMU and German current account surpluses are getting even larger (relative to GDP) and at the same time the euro exchange rate has been losing value (see the chart).

Flexible rates are no panacea

This is significant because the move away from the post-war Bretton Woods system was a move away from a rigid system with fixed rules to a flexible system in which countries might choose to run very different and independent policies. Flexible exchange rates were supposed to be the grease that would allow trade to continue in this environment without causing large imbalances to crop up and to undermine it. Exchange rate theory looks for the currency of the surplus country/currency to rise. That rise increases purchasing power in that country or block stimulating imports. It also makes exports less competitive causing exports to slow. That combination of pressures should bring the surplus down and restore balance to the balance of payments. But looking at the example of the EMU, that is not happening. Instead surpluses as a percentage of GDP are getting larger and the euro exchange rate is staying weak and getting weaker.

PPP explained

The table shows an exchange rate perspective using a technique known as purchasing power parity (PPP). The idea behind this theory is that markets will act so as to equilibrate exchange rate-adjusted prices across countries over time (think of it as another a manifestation of what some call the 'the law of one price.' Within limits a good can sell at only one price in the global economy). In the table, we calculate PPP using two different price indices: a producer price index (PPI) and a consumer price index (CPI or HICP, in the EMU). While PPP has many different approaches, in the table I use the simplest one. Using the JP Morgan real effective exchange rate (JPMREER) data ('real' for inflation-adjusted, and 'effective' meaning trade-weighted), I calculate PPP using a simple assumption. That assumption is that while exchange rates (and real exchange rates) may fluctuate all over the map in the short run, over time the markets ought to get exchange rate values 'right.' Therefore, the MEAN of the series RJPMREER (plotted on the chart) is an estimator of PPP, or of the correct value for the currency. This is a simple expedient that gets us away from having to calculate the prices of the same goods in different currencies and figure out what exchange rate it would take to create pricing parity.

Perverse trends

Early in the floating rate system, this approach seemed to have value. But what we can see happening is that over time the moving averages show two common trends (1) that the German and EMU surpluses relative to GDP are rising and (2) that the PPP position of the euro is continuing to become more and more undervalued. In short, PPP is acting to make Germany and the EMU even more competitive and acting to increase German and EMU exports while fending off imports into Germany and the EMU. That, in turn, is making the German and EMU current account surpluses larger and larger. The exchange rate is the operative factor here and the expanding current account surplus is the result.

A failed exchange rate system

Exchange rates are failing to do their job. While there is a lot of focus on policing 'commercial policy' (tariffs, subsidies and trade barriers) through WTO (World Trade Organization), what is the point if countries engage in what is essentially macroeconomic price fixing? You may have been taught that 'Free Trade is good' but trade occurring in this environment is not free or fair; it is cooked and crooked. The U.S. low tariff and non-tariff barrier approach to trade coupled with the U.S. economy's relatively high income has made it a target for exporters around the world who now view it as their right to exploit demand in the U.S. A number of countries- not just in the EMU- run relentless trade surpluses vs. the U.S. The U.S. does get cheap goods out of this deal, but it also gets its net asset position eroded. Foreign governments have to continue to plow their trade surplus dollars back into the U.S. to keep the dollar so strong and this keeps the U.S. infused with liquidity. But since the dollar is so strong, the U.S. has little to offer as a production platform. Few firms want to invest and produce in the U.S. The irony is that there is surge of surplus funds in the U.S. that mostly winds up getting used to fuel various forms of consumption or fiscal deficits and that keeps this massive 'Ponzi-like' scheme going. Since the financial crisis, the fragility of this process has revealed itself since the U.S. has now lost so much investment especially in the manufacturing sector that its ability to grow is impeded. The ability to create jobs has slowed and along with it the ability to create good-paying jobs has ground to a near halt.

The rise of Donald Trump

It should be surprising to no one that Donald Trump, a candidate with a protectionist bent, has come to office. Four years ago Mitt Romney tried to run on the same international platform, but America was not as disenchanted with trade back then plus Mr. Romney had other issues. Of course, Mr. Trump has his own 'baggage', but his message on trade protectionism and job creation has been a focused clarion call to disenfranchised voters who feel they have been force-fed the snake oil of free trade for too long.

Trump as catalyst?

My view of this whole process is much more sympathetic; there should be disenchantment with the way the global exchange rate mechanism is working and with the result it has created. But apart from a few people who continue to harp about the gold standard, there is next to zero interest in anything under the rubric of international monetary reform that is moving ahead. But maybe fear or disenchantment with Trump's plans will eventually open that door? For now Trump is venting his spleen on something that will get results.

I view Trump as essentially using commercial policy to try to offset wrongs being perpetrated in the currency market where the U.S. is being systematically put at a competitive disadvantage because of unfair exchange rate policies. Ironically, perceptions of Trump's own policies have caused the dollar to get even stronger because he is talking of tax cutting especially at the corporate level. Many fiscal conservatives also are advocates of a 'strong dollar.' I find this interesting since my specialty (my Ph.D. dissertation) was in international trade and in all the courses and books I read about international economics I have yet to read one that says it is good to have the either the dollar or the current account persistently out of equilibrium. Yet, some people will speak to you on this issue as if that is something that is true and that everyone knows for a fact (and you can't debunk it on snopes).

Side effects from a strong dollar

The fact is that an overvalued dollar, one that is persistently and substantially overvalued, will lead to a lower price level (inflation persistently too low), to a higher rate of unemployment (or to an outsized proportion of disenfranchised 'discouraged' workers). It will lead to lower employment and lower investment. It will eventually lead to lower growth. So stop me any time that you see anything familiar between these characteristics and the actual circumstances of the U.S. economy.

Europe re-tools

Interestingly, Europe is using its weak currency to re-tool. And while it is not seeing 'boom-times,' it has been able to use the low euro as a way to prop up demand at a time when it has undergone a period of fiscal probity. Germany has actually fared well while other EMU nations are doing much better than they would have in the face of the fiscal corsets they have endured. Using the exchange rate to push your own adjustment costs onto your neighbor is an example of 'beggar they neighbor' policies.

Eco-nomics

It is important to understand that the 'eco' in economics has the same reference as the 'eco' in ecosystem. Our economic system with global trade is a closed system (no one-way trade with Mars). Either trade is mutually beneficial or it will be destructive. The concept 'mutually beneficial' does not mean that countries specialize with one as a producer and another as consumer, but that is what has happened in a de facto sense to the U.S. economy. The problem with that is that being a consumer nation is not sustainable even with access to strong purchasing power. Persistent current account deficits leach a county's wealth and undermine its ability to continue to spend and to run deficits even though the deficits provide credit to support deficit spending. At some point that becomes a dead end and a fool's game.

Trump the President

And that is the realization that has brought Donald Trump to office. He is not the messiah and he is not just 'any port in a storm.' He has isolated a problem and he has a plan to fix it and despite fact that the international trade intelligentsia is aghast at what he proposes. I think that in a more thought-out framework Trump's plan actually makes sense. There is little that he can do unilaterally other than to force the issue. It is an attempt to bring adjustment pressures to a global trading scheme that has become increasingly skewed and mercantilist. There is very little in global trade flows that look much like Free Trade and Fair Trade. At some point, if you have to twist a few arms to make trade freer or fairer, maybe arm twisting is a good strategy as confrontational and dangerous as it surely will be. Without it, the trends such as those we see for the EMU current account and currency are just as dangerous in and of themselves. They already are trends that are running amok. It's not like Trump is meddling with a system that is working perfectly- far from it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief