Global| Oct 24 2013

Global| Oct 24 2013EMU Shows Slowing But Still Growth

Summary

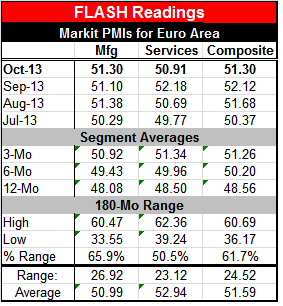

The EMU PMI from Markit this month shows a set back to the pace of improvement in the euro area. Manufacturing is doing a bit better, rising to a diffusion reading of 51.3 in October from 51.1 in September. That is an improvement, but [...]

The EMU PMI from Markit this month shows a set back to the pace of improvement in the euro area. Manufacturing is doing a bit better, rising to a diffusion reading of 51.3 in October from 51.1 in September. That is an improvement, but a pretty thin one. The services sector is looking less bright. Its reading of 52.18 in September has crumbled to 50.91 in October. This is just above the neutral reading of 50.

The EMU PMI from Markit this month shows a set back to the pace of improvement in the euro area. Manufacturing is doing a bit better, rising to a diffusion reading of 51.3 in October from 51.1 in September. That is an improvement, but a pretty thin one. The services sector is looking less bright. Its reading of 52.18 in September has crumbled to 50.91 in October. This is just above the neutral reading of 50.

The EMU-wide manufacturing reading stands in the 48.3 percentile of its historic queue. The services component stands in the 31.7 percentile of its historic queue. Thus, the manufacturing reading for EMU is near its median. But the services sector reading is only in the lower third of its range.

As for the early reporters, Germany and France, neither of them shows much change in manufacturing in October. In Germany the manufacturing reading is up to 51.4 compared to 51.12 in September. In France the October reading is 49.44 compared to 49.81 in September. The German manufacturing reading stands in the 53.9 percentile of its historic queue while the French reading stands in the 36.8 percentile of its historic queue- near the lower third of its range.

For services both Germany and France took a set-back in their October Markit readings. Germany slipped to 52.26 from 53.69 in September. In France the slippage was to 50.19 in October from 50.98 in September. The German services sector reading stands in the 50th percentile of its historic queue and is thus a median reading. For France the reading stands in the 25.7 percentile and is just above the bottom quartile of its historic queue - quite anemic.

The lagging services sector in France and in the euro area is a statement about how the EMU economy is failing to spread job growth. The services sector is the job sector because of its lower productivity. The improvement in manufacturing, were it robust enough, might help to pull the services sector out of its morass, but it does not seem to be working that way in Europe as the manufacturing sector itself is struggling.

The monthly PMI readings cannot be looked up with much satisfaction by Europeans or anyone who is bullish on the region. Spain may have technically kicked itself out of recession, but it is a technical improvement, not a very strong actual improvement. Consumers in Italy, once with rising spirits, are now seeing them crash down to earth. Europe remains in trouble. Having a new assessment of its banks on the docket is not going to make them anymore generous in making loans in the meantime. Europe is still floundering and unlikely to gain much momentum anytime soon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief