Global| Apr 03 2014

Global| Apr 03 2014EMU Services Sector Backtracks in March: Is That All There Is?

Summary

The services sector in the European Monetary Union edged lower in March to a level of 52.2 from a standing of 52.6 in February. The step back was small but interrupts an ongoing trend toward improvement at a time that recovery in the [...]

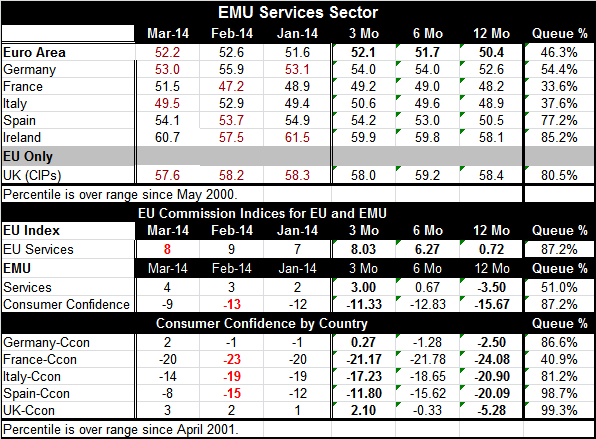

The services sector in the European Monetary Union edged lower in March to a level of 52.2 from a standing of 52.6 in February. The step back was small but interrupts an ongoing trend toward improvement at a time that recovery in the Union is in its early stages. We have five countries as early reporters into the system; among these countries Germany and Italy saw their services sectors take a step backward in March. The Italian services sector actually dipped below the breakeven level of 50 to stand at 49.5, a substantial drop from February's 52.9 level.

The services sector in the European Monetary Union edged lower in March to a level of 52.2 from a standing of 52.6 in February. The step back was small but interrupts an ongoing trend toward improvement at a time that recovery in the Union is in its early stages. We have five countries as early reporters into the system; among these countries Germany and Italy saw their services sectors take a step backward in March. The Italian services sector actually dipped below the breakeven level of 50 to stand at 49.5, a substantial drop from February's 52.9 level.

Germany is the country with the largest weight in the EMU. Its index is at a raw diffusion level of 53.0 in March. However, its queue standing is in the 54.4th percentile. What that means is that the German index is higher than this about 46% of the time and lower approximately 54% of the time. The weakest queue standing or relative standing among the separately reporting countries is France; its queue standing is at 33.6%. This means that the French services sector is stronger than this about two thirds of the time and weaker about one third of the time. While Italy has a lower raw standing than France, its queue standing is slightly higher, in the 37th percentile, but still that's not much different from the French reading. Spain and Ireland have the highest queue standings. Spain's is at the 77th percentile and Ireland's is at the 85th percentile. Ireland's raw reading at 60.7 is strong and is part of an ongoing string of strong numbers from Ireland.

The UK is part of the European Union but does not share in the common currency. Its services sector backed off to 57.6 in March from 58.2 in February. While this is one of the weaker service sector readings from the UK (weakest since June 2013), it still has a standing in the 80th percentile of its historic queue.

Countries of the European Union that are not part of the Monetary Union show stronger performance in their services sectors.

The EU Commission service sector metric is at a queue standing at the 87th percentile over the same time that the European Monetary Union index reading from the European Commission show an EMU standing at the 51st percentile. Because of the difference between those two aggregated measures, this adverse comparison suggests that being in the Monetary Union has held back recovery in the services sector. That's not at all that surprising considering that the weaker members of the Monetary Union we put through a rigorous course of austerity and they are still in the process of trying to recover from that.

Additionally, we look at consumer confidence by country also using the measures from the European Commission. By these measures, the UK and Spain have the strongest consumer confidence with Germany and Italy relatively close behind and France at the bottom of the pack. France is having a very hard time getting its economy in gear with the sluggish services sector and very weak consumer confidence; however, French manufacturing did better this month, a lot better.

The standing for the European Monetary Union services sector as a whole at 52.2 is just slightly ahead of its three-month average at 52.1. Yet, the current 52.2 standing is only in the 46th percentile of its historic queue meaning that even though 52 signals that this is expansion in the services sector, the sector is higher than this more than half of the time. The median for the queue stands above the level that the diffusion index sets for neutrality. This tells us that the services sector tends to expand most of the time. That's not surprising. It's important to recognize even though the services sector is expanding to the level of 52.2, it's still below its historic median and therefore 52.2 is a poor reading.

In the case of France, its 51st percentile standing is well below its historic median and the queue standing tells us it's a very poor level. In the case of Italy, the diffusion value itself at 49.5 tells us that the sector is contracting, but the diffusion reading stance at the 37th percentile tells us that the Italian reading is not often this weak and therefore a very poor reading.

In putting the level of the diffusion indexes together along with the queue standings, we get a much better perspective on how the euro area services sector is performing. The picture that we get from this month is that it's performing poorly. There are only two of five early reporting countries that saw setbacks to their services sectors in March; however, three countries saw setbacks in February. Among the large countries, only Spain, the fourth-largest country in the euro area, has what we would consider a relatively strong services sector. Even Germany's services sector is only in the 54th percentile of its queue. Clearly the euro area has a long way to go before we will be able to agree its recovery seems stable. It is still fiddling around at or below the 50.0 mark for diffusion and the 50th percentile queue standing. That's too low a level to be impressive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief