Global| Mar 24 2015

Global| Mar 24 2015EMU Services Hold on to Strong Recovery

Summary

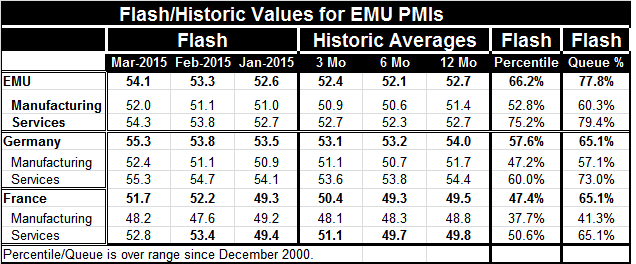

The euro area economic recovery continues to be led by the services sector recovery. Not only are the PMI diffusion values higher for services than for manufacturing, but the queue standings show that they are relatively much stronger [...]

The euro area economic recovery continues to be led by the services sector recovery. Not only are the PMI diffusion values higher for services than for manufacturing, but the queue standings show that they are relatively much stronger than manufacturing as well.

The euro area economic recovery continues to be led by the services sector recovery. Not only are the PMI diffusion values higher for services than for manufacturing, but the queue standings show that they are relatively much stronger than manufacturing as well.

The EMU services sector diffusion readings are steadily higher in each of the last three months. This sort of recovery progression, however, is not yet entrenched enough to be reflected in sequential strength for 12-month to six-month to three-month PMI averages. Over those horizons, however, the services readings are stable and lower than what they have become for the last three months as the sector has accelerated.

Germany also shows a strong progression higher in the last three months for its services sector against background of a minor sequential weakening from 12 months to six months to three months. Once again we find that the last three months show the German services sector strong than for its broader averages. France fails to follow this theme because of a drop back in its services sector in March; but its March reading is still better than its January reading and it's better than its three-month and six-month and 12-month averages. Despite some prevarication, France is also showing some tendency to improve.

The manufacturing sector shows a minor improving trend in the EMU in each of the last three months. Germany joins that pattern of improvement. But for the broader EMU horizon manufacturing, out to 12 months, it is still trendless and holding just above the 50 mark for diffusion (which is the neutral reading). France's manufacturing sector has weak readings with manufacturing sequential averages below 50 and with its recent three-month also stuck below 50 and showing no sign of improvement.

Despite the differences between the EMU as a whole, Germany and France, the theme that is invariant is that the services sector has a higher absolute diffusion value and a higher queue percentile standing than manufacturing. This makes it clear that the services sector is holding these economies up. Despite the impact of austerity in the EMU which has depressed domestic demand and despite the recent stimulus from the dropping euro which should act to create stimulus that will work through trade and the manufacturing sector, it is the services sector that is driving growth in the EMU.

Since the euro exchange rate has fallen and is falling so hard, we should expect to see the manufacturing sector revive. With manufacturing standing on in its 60th historic queue percentile compared to services at their 79th percentile, there is ample room for manufacturing to kick in and send the EMU economy into a stronger growth trajectory. With the ECB engaged in a complimentary program to enhance financial markets performance, the EMU seems to have quite a number of factors pushing it on to stronger growth rates. Our concern is that all this stimulus will prove to be too much for Germany which is reviving quickly and should benefit the most from the lower euro exchange rate. But so far evidence of a German manufacturing revival is scant and the rest of the EMU is still slow in reviving its manufacturing sector. Services continue to carry the EMU ahead and to drive momentum for overall private sector.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief