Global| Mar 04 2009

Global| Mar 04 2009EMU Services Contract as UK Sector Cuts Losses

Summary

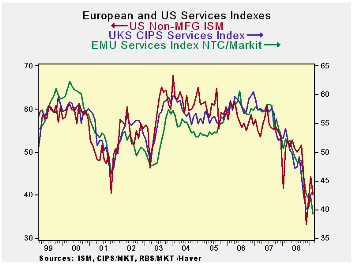

This trend is not a friend - In our select group of EMU members (see table) all show month-to-month deterioration in services activity. Meanwhile, the UK continues to cut losses relative to its November low. The US follows a pattern [...]

This trend is not a friend - In our select

group of EMU members (see table) all show month-to-month deterioration

in services activity. Meanwhile, the UK continues to cut losses

relative to its November low. The US follows a pattern somewhat like

the UK with its non-MFG index doing some backtracking in February but

still forming a series of months with a rising profile from a November

(2008) low.

Fate as her mistress - Europe is still slipping

lower, having just reached its cycle low in February. The tentative

evidence suggests that the US and UK are turning (or trying to turn a

corner) on the worst of times at least for their ‘Service’ sector. In

the US the situation is complicated by lumping the troubled housing

sector in with services as ‘non-MFG’.

The essential point here is that Europe is - as it usually is --

trailing the US by a few months. Typically it’s trailing by about six

months.

Masters of illusion - There was a brief period in

2006 when the US seemed to be lagging and Europe seemed to growing. At

that time Euro-pride was at its zenith. For a time the euro currency

ran to unprecedented heights on the view that Europe was special and

perhaps even bullet-proof. In time, that fallacy revealed itself as

sub-prime became the catalyst to expose all sorts of bad market

practices including excess lending to Eastern Europe explaining in part

the brief suspended animation for Europe from incipient US weakness.

But now it’s all out in the open and Europe and the US are part of the

same cyclical downturn. Notions of de-coupling are colder and deader

than Iceland’s balance sheet.

Europe continues to be beset with weakness from manufacturing

transmitted to services. The banking problems that Europe was initially

in denial about have simply taken a bit longer to emerge there, at

least in some respects. Remedy’s are in train, but so is more damage.

Old fashioned, anyone?

I find interesting the notion that the old fashioned business cycle is

back in play. The US is leading the cycle and Europe is following.

While some want to paint a picture of this cycle was something

unprecedented it is more like the 1973-75 and the 1981-82 cycles that

previously gripped the global economy. In 1977 the Economic Summit in

London failed to embrace a US-sponsored notion of a locomotive in which

stimulus across the G-7 would help bring world growth. By the Bonn

Summit in 1978 the G-7 was ready for this, but by then recovery had

started and Bonn only helped to inflation the recovery balloon beyond

its need. Against that patch of history this cycle is a bit more

understandable. Without any formal coordination we have a locomotive

process in train involving a US stimulus package various European

packages and large effort from a G-7 outsider, China. This is a

different version but it is more timely than what had been attempted in

1977/78. It is a good example of global enlightened self-interest.

The Bonn summit in 1978 declared:

‘We agreed on a comprehensive strategy covering growth, employment and

inflation, international monetary policy, energy, trade and other

issues of particular interest to developing countries. We must create

more jobs and fight inflation, strengthen international trading, reduce

payments imbalances, and achieve greater stability in exchange markets.

We are dealing with long term problems, which will only yield to

sustained efforts. This strategy is a coherent whole, whose parts are

interdependent. To this strategy, each of our countries can contribute;

from it, each can benefit.’

Not depression neglect but hybrid recession forces at work

- The actions this time around are not much different except that they

include a lot of help to a very battered global financial system. If

the efforts to patch up the financial system bear fruit I expect the

various efforts at stimulus to be successful. For the moment I see a

lot more comparisons with 1973-75 and 81-82 than with the great

depression everyone is so fond of speaking about. Without timely action

on the financial sector, a key part of the service sector, I might be

compelled to change my mind. But having the financial patches in play

is crucial to the outlook. Having them, it strikes me that the

developing recovery processes are much better understood in terms of

the recent history of economic summitry than by dredging up the

horrible depressing dillies from the days of Depression when various

federal safety nets were not available and the lessons from our

then-current folly had not been learned. This recession has late cycle

weakness as did 1973-75. But it also has the financial chaos

characteristic of 1981-82. (It is worse than that this time, but

similar to 1981-82.) Like 1973-75 it also has an oil trigger.

Bad summit/good summit - We may still employ summits

to try and get global attention to bear on this crisis. But what is

different this time is the willingness of countries to act

independently, yet in concert, without the need for a formal summit.

Yes, a summit still is coming. But it will likely not be that

successful. And this is because the leaders have learned to work

separately and with common purpose at the same time with a good measure

of success, taking pressure from the summit. Summits are too-grand and

too high-stakes, those factors ultimately constrain world economic

summit achievement. But summitry has undoubtedly brought the world

leaders closer, allowing them to think more alike as a global problem

emerges such as the one we are in the midst of trying to solve.

| NTC Services Indices for EU/EMU | |||||||

|---|---|---|---|---|---|---|---|

| Feb-09 | Jan-09 | Dec-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 39.24 | 42.16 | 42.06 | 41.15 | 43.36 | 46.69 | 0.0% |

| Germany | 41.32 | 45.20 | 46.57 | 44.36 | 46.13 | 49.49 | 0.0% |

| France | 40.18 | 42.56 | 40.57 | 41.10 | 44.53 | 47.77 | 0.0% |

| Italy | 37.85 | 41.10 | 40.30 | 39.75 | 42.30 | 45.26 | 0.0% |

| Spain | 31.73 | 31.84 | 32.10 | 31.89 | 32.04 | 35.97 | 10.9% |

| Ireland | 31.78 | 33.94 | 34.14 | 33.29 | 34.89 | 39.14 | 0.0% |

| EU only | |||||||

| UK (CIPs) | 43.24 | 42.48 | 40.21 | 41.98 | 42.39 | 45.86 | 15.5% |

| US NONFMG ISM | 41.60 | 42.90 | 40.10 | 41.53 | 42.77 | 46.53 | 17.5% |

| EU Commission Indices for EU and EMU | |||||||

| EU Index | Feb-09 | Jan-09 | Dec-08 | 3Mo | 6Mo | 12Mo | Percentile |

| EU Services | -29 | -28 | -23 | -31.33 | -27.00 | -21.42 | 0.0% |

| EMU | Feb-09 | Jan-09 | Dec-08 | 3Mo | 6Mo | 12Mo | Percentile |

| Services | -23 | -22 | -17 | -20.67 | -13.50 | -5.42 | 0.0% |

| Cons Confidence | -33 | -31 | -30 | -31.33 | -27.00 | -10.75 | 0.0% |

| Consumer confidence by country | |||||||

| Germany | -29 | -27 | -22 | -26.00 | -19.00 | -11.67 | 0.0% |

| France | -36 | -35 | -34 | -35.00 | -31.67 | -25.58 | 0.0% |

| Ital | -28 | -26 | -30 | -28.00 | -25.83 | -24.58 | 6.3% |

| Spain | -48 | -44 | -46 | -46.00 | -44.17 | -37.83 | 0.0% |

| UK | -32 | -35 | -29 | -32.00 | -28.83 | -23.42 | 7.9% |

| percentile is over range since May 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief