Global| Apr 27 2017

Global| Apr 27 2017EMU Sentiment Index Regains Its 2007 Level

Summary

The European monetary area continues to show progress. This month each one of the five indicators rose month-to-month and for the 16 reporting members of EMU all but Slovenia and Cyprus reported month-to-month gains in their overall [...]

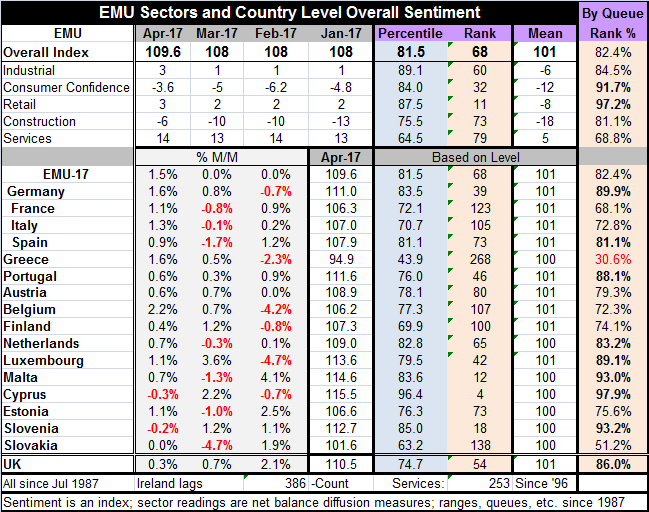

The European monetary area continues to show progress. This month each one of the five indicators rose month-to-month and for the 16 reporting members of EMU all but Slovenia and Cyprus reported month-to-month gains in their overall country sentiment indicators. The overall EMU indicator moved up to 109.6 in April from 108 in March and holds an 82nd percentile standing among all its historic values- a quite firm to strong reading.

The European monetary area continues to show progress. This month each one of the five indicators rose month-to-month and for the 16 reporting members of EMU all but Slovenia and Cyprus reported month-to-month gains in their overall country sentiment indicators. The overall EMU indicator moved up to 109.6 in April from 108 in March and holds an 82nd percentile standing among all its historic values- a quite firm to strong reading.

Strongest sector in context

Looking at the five indicators, the two strongest components are consumer confidence and retailing, each with a rank standing in their respective 90th percentile ranges. Industry and construction have standings in their respective 80th percentile ranges. Services have the most modest reading with a 68th percentile reading and while it is a more moderate mark, it is still a relatively firm reading standing well above its median which occurs at a standing at the 50th percentile.

12-month gains

Over the past 12 months construction has made the strongest gains and it also has the strongest gains over the last three months. The industrial sector, which lags behind retailing and consumer confidence in terms of its rank standing, has charged hard over 12 months with a net gain on its reading of seven points. The consumer sector has gained 5.7 points over 12 months while retailing, despite its strong standing, has gained the least rising by only two points as services, with a weak standing, also has weak momentum having gained only three points in 12 months.

The strength is not among the Big Four

Strength in the EMU seems to have shifted largely outside the Big Four members. Germany is the exception (as always). Among the reporting 16 of 17 members (Ireland is always late), the countries that consistently lag the most over the last three months, six months and 12 months are Spain, Greece and Slovakia. These I rank based on the changes in their sentiment indexes. Italy also is a bit of a laggard ranking 12th over three months and 16th over 12 months (out of 16) but rallying to a rank of 6th best over three months. France ranks 9th over three months and 12 months but manages to rank as the third strongest over six months. Among the Big Four economies, out of 12 possible rankings (four countries over three periods) the Big Four economies rank in the top tier only five times. Their average ranking is 9.7 out 12 16 where 1 is best and 16 is worst.

Strength has migrated to the periphery

Some of the smallest countries have the best recent performance. Malta ranks number one over three months with Estonia at number two, Slovenia at number 3; Portugal ranks fourth. Over six months the strongest gains are by Luxembourg (1), Austria (2), France (3), Cyprus (30), and Belgium (5). Over 12 months the strongest gains are from Austria (1), Finland (2), Estonia (3), Germany (4), Malta (5), and Luxembourg (6).

The overall EMU rating and its historic rankings are based on an index that is weighted. But these country by country rankings are telling about where the growth is and isn't. Germany is responsible for most of the strength in the top four economies especially over 12 months and three months.

More concentrated weakness than strength

What is clear from these rankings is that there is no country that is consistently strong, but three, Spain, Greece and Slovakia, emerge as consistent laggards. Slovakia has an average ranking over the three periods (three-month, six-month and 12-month) of 15.3. Spain is at 13.7 and Greece is at 12.7. While there are such clear laggards, the strongest three-month average ranking based on these sequential gains is Austria at 3.3. That is followed by Estonia that averages a ranking of five followed by Slovenia at 6, Malta at 6 and Finland at 6.

Momentum is more mixed than are standings

Of course, I am ranking them on changes in their indexes alone and we previously looked at percentile standings for the EMU and for sectors where the rankings are quite high. Apart from momentum, there are three EMU members with sentiment index rankings based on the level of the index that are in their top 10 percentile (90% or higher): Cyprus, Malta and Slovenian. And there are six more with rank standing in the next decile (top 20% to 10% of their respective histories): Germany, France, Spain, Portugal, the Netherlands, and Luxembourg. However, many of these are not on the top countries in a momentum list, raising questions about whether they are really prepared to hold these rankings.

The ECB...well met

On balance, as the ECB met today, Mario Draghi declared that conditions had improved across the zone. He also cautioned that there we no signs of inflation and that stimulus may still have a long time to run. His remarks in many ways echoed the statement from the BOJ today that similarly found improvement but cautioned that Japan was still well behind in getting its economy on firm footing noting that stimulus still probably was going to be in place for some time to come. Only in the U.S. are the authorities ready to make rapid fire rate hikes this year at least in comparison to the rest of the world.

The global scene: reemergence of divergence

There was a time that markets were getting somewhat restless with current policy. They were seeing that Europe was recovering and began to expect a policy shift. But today Draghi seems to have pushed that toothpaste back into the tube. While Kuroda and the BOJ are more upbeat on their economy, they are also cautious. The Fed, however, is shedding its caution and markets do not seem to have really reflected the reemergence of that divergence. Fed members are getting bolder in their expectation for the economy even though the U.S. inflation revival has been mostly in oil. And while many U.S. labor market metrics scream tightness, one very important one does not, and that is wages. I view all these economies as still in transitional periods. I do not think the baton has yet passed to normalcy. I continue to be wary of those who want normalcy so much that they have adopted relative standards for growth and become pessimistic about prospects and about inflation despite ongoing evidence to the contrary. I'm not sure if the U.S. has a new growth boundary at 1.8% or not. It will depend on a lot of things as we have a president who is trying to remove many of the constraints that have limited U.S. growth. Just because the Fed thinks that the U.S. growth limit is 1.8% does not make it so. Anyone following the Fed's analytics for the past decade knows who you need to take Fed analysis with grain or two of salt these days. After all this stimulus, it is not surprising that the Fed is more cautionary than bold in interpreting the 'facts.' We need to keep an eye on our central bankers everywhere, who still face challenges and will face even more push back against policies of continued accommodation since growth is not as weak as it was. But that does not make it 'normal.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief