Global| Aug 12 2015

Global| Aug 12 2015EMU's Industrial Sector Weakens

Summary

Industrial output (excluding construction) fell in the EMU in June, dropping by 0.4%. This is the second consecutive monthly drop. These drops follow a monthly gain of just 0.1% in April. IP in the EMU has been steadily decelerating [...]

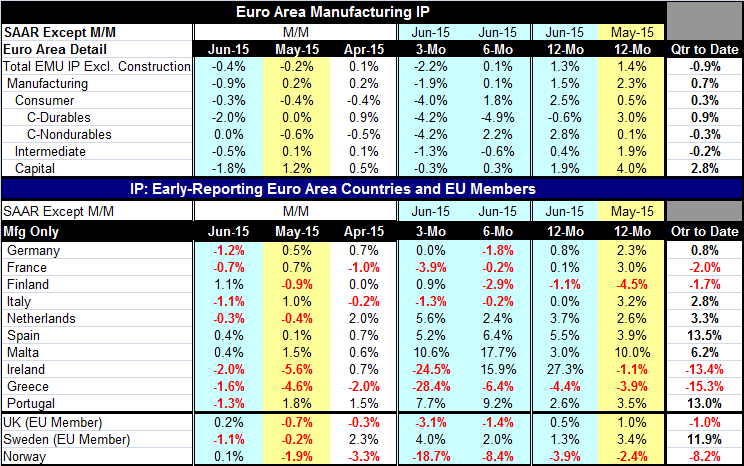

Industrial output (excluding construction) fell in the EMU in June, dropping by 0.4%. This is the second consecutive monthly drop. These drops follow a monthly gain of just 0.1% in April. IP in the EMU has been steadily decelerating as it rose by 1.3% over 12 months, at a 0.1% annual rate over six months but now is falling over three months at a 2.2% annual rate.

Industrial output (excluding construction) fell in the EMU in June, dropping by 0.4%. This is the second consecutive monthly drop. These drops follow a monthly gain of just 0.1% in April. IP in the EMU has been steadily decelerating as it rose by 1.3% over 12 months, at a 0.1% annual rate over six months but now is falling over three months at a 2.2% annual rate.

All three major categories of manufacturing output show a steady deceleration in output over these same horizons: consumer goods output, intermediate goods output and capital goods output. However, the chart of year-over-year growth rates looks more equivocal since the year-over-year growth rates have been far from stable.

In the quarter to date (which is the recently completed second quarter), trends are more tangled. Overall IP is lower with output falling at a 0.9% annual rate. But manufacturing IP is up at a 0.7% annual rate. Sector growth rates are positive for capital goods and consumer goods, but output is falling for intermediate goods.

Country level detail shows IP falling in seven of the 10 EMU member countries in the table. This number is up sharply from the past two months when IP fell in just three or four of the member countries in the table.

The drop in German IP was the first surprise for this month. But the next two largest EMU members, France and Italy, joined Germany to report IP declines. In June only Finland, where the industrial sector has been troubled, Spain and tiny Malta show output increases.

The global economy continued to sputter during this period. China was showing signs of slowing and of weaker global demand. Now China has dropped its currency sharply in a bid to get a larger share of the already slow-growing global pie. China's currency depreciation will put more pressure on its trading partners that already are struggling. China's domestic demand weakness has already hit the German economy hard. Now there is more to come.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief