Global| Dec 17 2014

Global| Dec 17 2014EMU's HICP Stays 1.7% Below Targeted Pace

Summary

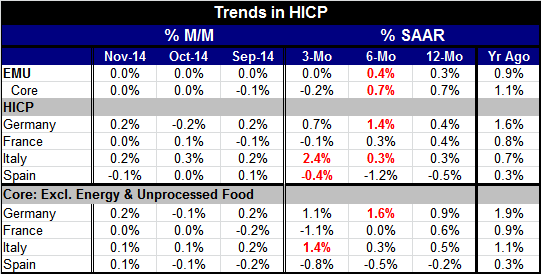

The euro area's HICP inflation is up by 0.3% year over year. The core is up by 0.7% on that horizon. Inflation in the four largest EMU economics is at an annual rate of 0.4% or less; Spain's price level is falling. Core prices among [...]

The euro area's HICP inflation is up by 0.3% year over year. The core is up by 0.7% on that horizon. Inflation in the four largest EMU economics is at an annual rate of 0.4% or less; Spain's price level is falling. Core prices among the four largest EMU members range from 0.9% in Germany to -0.2% in Spain. The European Central Bank is nowhere close to hitting - or even to making progress on hitting- its target of 2%.

The euro area's HICP inflation is up by 0.3% year over year. The core is up by 0.7% on that horizon. Inflation in the four largest EMU economics is at an annual rate of 0.4% or less; Spain's price level is falling. Core prices among the four largest EMU members range from 0.9% in Germany to -0.2% in Spain. The European Central Bank is nowhere close to hitting - or even to making progress on hitting- its target of 2%.

Inflation in the euro area is simply low. It is simply too low. And the EMU members are conflicted about what to do. How about this for a suggestion: hit your target!

Inflation is not showing any clear trend to accelerate or to decelerate. And over three months inflation's pace is not even usually lower than the 12-month pace across EMU, for its headline or for its core or for those measures applied to its four largest members. But with global energy prices falling - plunging - the risk has to be that inflation is poised to go lower before it turns higher. Lower means a move even farther away from its target.

The euro area simply cannot come to grips with the fact of its potentially fatal flaw. The ECB and the euro area were each constructed with the idea that there would be rogue countries and pressures for the ECB to reflate and the strongest possible steps were taken to construct institutions and rules that would prevent that. But in hind sight the euro area was established with only one set of tools and fears. It was not well constructed and it was not constructed with the flexibility to meet the demands of the times.

In the case of the EMU fiscal constraints, the plans did not work as expected. Shortly after he left the ECB presidency, Wim Duisenberg was in New York and I spoke to him about some of the EMU's fiscal problems. He noted that the hard money countries of the EMU had set a trap for the high-inflation countries with profligate fiscal spending. But the fiscal rules that the EMU adopted was a trap that was fallen into by the countries that set it. Germany and France, not Spain, Italy or Greece, were the first to violate the fiscal rules in the EMU. And they were given a pass rather than made to toe the line. This was the first undermining of the fiscal rules and it set in motion more violations by other members down the road.

Similarly, the ECB was constructed to make it impossible to overly reflate. It was set up to be a central bank operating in an inflationary world with a number of pro-inflation countries on its very board. Its charter was its safeguard against these temptations.

But things have not turned out as expected on the monetary front either. We do not live in an inflation-prone world. Deflation seems to a much larger risk. Yes, some euro-members want to reflate using more than the ECB's normal mandate, but that is because they are suffering weak growth, under employment and, in some cases, deflation. This is just the set of circumstances to call for some special departure from normal operating procedures. We have seen the Federal Reserve, the Bank of England and the Bank of Japan each implement special operations to try to stimulate their respective economics. Yet, just yesterday, Jens Weidmann, ECB member and President of the influential Bundesbank said even if there were deflation he would not be in favor of a move to special stimulus. Needless to say, this is not a very open minded approach.

These circumstances are why I say that Europe has succeeded in forming a fiat currency that has many of the same inflexibilities of a gold standard. Weidmann, Germany, and the Bundesbank do not want to engage in any special stimulus at all. Should there be worry about setting a precedent that might be misused in the future? Yes! But the uniqueness of these times would seem to be reason enough to set the stage for a special deviation in the ECBs practices- one that might not be a precedent in the future except in similar circumstances that would call for it. Basically, the Bundesbank is afraid of the dark. I don't think it is arguing that special stimulus is not warranted as much as it is afraid of what might happen once the precedent is set.

So the question is really about how special these times are and how long economic adjustment might be dragged out if the ECB can't take special steps to implement a program like QE. No one knows the answer. But countries that have employed QE promptly (the U.S. and the U.K.) have done better than those countries or regions that have not (Japan and the EMU). One added problem that makes Germany's dissent even more of a glaring issue is that in this environment the German economy is still doing relatively well. Its growth is slower but it is still one of the very best-performing economies in Europe. Its opposition is to measures that could help fellow members who are much more in need. And this is at a time when fiscal austerity is still being implemented around the euro area. Monetary stimulus is the last game in town and the Germans are opposed to using it. The Germans seem to think that good fences make good neighbors and that is the end of it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief