Global| Jun 04 2021

Global| Jun 04 2021EMU Retail Sales Shed Most of Last Month's Gains

Summary

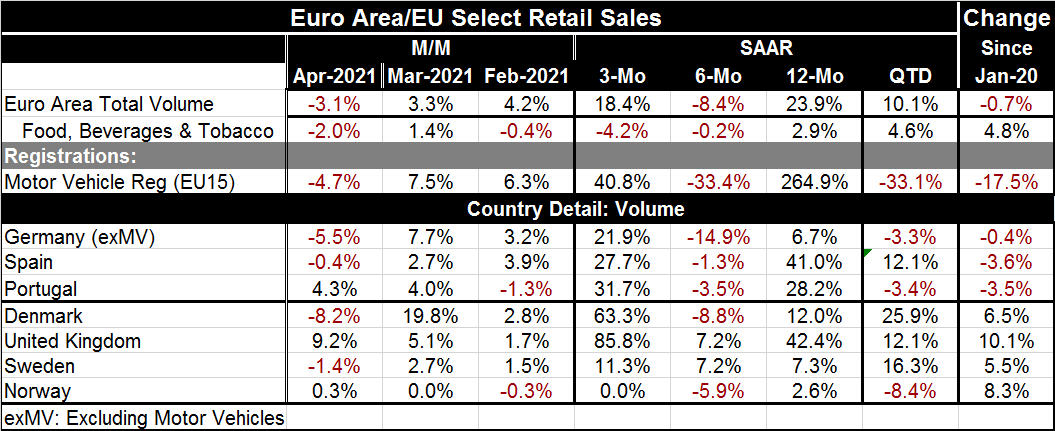

Retail sales volumes in the EMU fell by 3.1% in April, shedding most of the 3.3% gain they logged in March. Sales volumes still are advancing at an 18.4% pace over three months. But they are lower at an 8.4% pace over six months and [...]

Retail sales volumes in the EMU fell by 3.1% in April, shedding most of the 3.3% gain they logged in March. Sales volumes still are advancing at an 18.4% pace over three months. But they are lower at an 8.4% pace over six months and still higher by 23.9% over 12 months. Because these growth rates are so unstable drawing from the Covid-19 and post Covid-19 periods of infection and re-inflection, I have plotted the retail sales values and auto registration values in expenditure amounts in the period not as percentage changes as is customary. In this form, the charts actually make more sense and it is easier to see what is going on. When the news on retail sales in the current month is competing with a wildly shifting base for the percentage change calculation, all sense of direction can get lost. The chart is my rejoinder to this odd situation.

Retail sales volumes in the EMU fell by 3.1% in April, shedding most of the 3.3% gain they logged in March. Sales volumes still are advancing at an 18.4% pace over three months. But they are lower at an 8.4% pace over six months and still higher by 23.9% over 12 months. Because these growth rates are so unstable drawing from the Covid-19 and post Covid-19 periods of infection and re-inflection, I have plotted the retail sales values and auto registration values in expenditure amounts in the period not as percentage changes as is customary. In this form, the charts actually make more sense and it is easier to see what is going on. When the news on retail sales in the current month is competing with a wildly shifting base for the percentage change calculation, all sense of direction can get lost. The chart is my rejoinder to this odd situation.

The chart on retail sales volume shows the Covid-19 spike-drop, the sharp recovery and the second sharp but less deep spike lower with another sharp rebound then the latest result that is part of a drop off from that second peak. Sales volumes in April 2021 are slightly below their December 2020 and January 2019 levels. This leaves them off their secondary peaks of January and February of 2021 and below their levels of June-October of 2020 in the immediate aftermath of the rebound from the first Covid-19 wave.

The table details seven European experiences: three EMU members and four non-EMU members. In April, four of the seven show retail volume declines. This result contrasts with increases in sales volumes all-around in March. In February, Portugal and Norway logged one-month sales declines as well as the others logged increases.

However, over three months there are no countries in the table with sales volume declines except Norway showing no change in sales over three months. Over six months there are declines in five of the seven countries with the U.K. and Sweden being the exceptions. Over 12 months a calculation that moves the base to March 2020 when the virus was still impacting Europe strongly, all 12-month changes show increases from this base and some of them are quite strong.

The far right column is an attempt to avoid all the Covid-19 turbulence in the data. It is the simple percentage change in each series in the table from January 2020 before the virus struck. And the virus struck Europe all at once but with some slight timing differences then sent secondary waves of infection on timelines that were different for each country. Avoiding as much of that as possible is a good idea if we are looking for consistencies.

From January 2020 to date, sales are 0.7% lower in the EMU. For the three EMU nations Germany, Spain and Portugal, sales are lower in each case from January 2020. For the other four European countries sales increased and did so quite substantially since January 2020. The EMU did not do well in dealing with the virus. Denmark, the U.K., Sweden, and Norway averaged a sales increase of 7.6% compared to the EMU’s 0.7% drop.

European vehicle sales fell in April after rising in February and March. As a result, registrations are up strongly over three months but down substantially over six months and rising by better than 250% over 12 months but that is all Covid turbulent. When registrations in April are gauged vs. their level in January 2020, they are lower by 17.5%. Europe is still struggling to attain a real recovery although it appears that EMU members are struggling harder than non-EMU European countries.

In the quarter to date (that is for the just completed Q1 ended in March), EMU sales are up at a strong 10.1% pace. Spanish sales are rising at a 12.1% pace while German and Portuguese sales volumes shrank. For the non-EMU sales in Europe, very strong sales are reported for three of them with Norway as the exception; it has sales volumes plunging at an 8.4% annual rate.

On balance...

The retail sales profile for Europe over the past year runs a path that might be construed as too volatile a track for young children if it were a carnival ride. The twists and turns of trend were capriciously driven by the virus, a thing that is still active and affecting output, but that seems to be more tempered and should remain so as vaccination rates rise. While there is government support in Europe, it is much less than it has been in the U.S. Moreover, in Europe the headline HICP, which the ECB targets as its only policy objective, has just topped 2% and it is not clear how soon that will cause the ECB to trigger a less accommodative response. If inflation stays at the 2% mark, ECB policy objectives should have it rather quickly dismantling the various super accommodative elements of monetary policy. So in Europe, the game is changing and all bets on the future are pending.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief