Global| May 06 2019

Global| May 06 2019EMU Retail Sales Go Flat in March, Still Carry Momentum

Summary

Retail sales volumes in the EMU are slightly elevated but remain on a moderate growth path after going flat month-to-month in March. Sales volume is up by 1.8% over 12 months, accelerating over six months and accelerating also over [...]

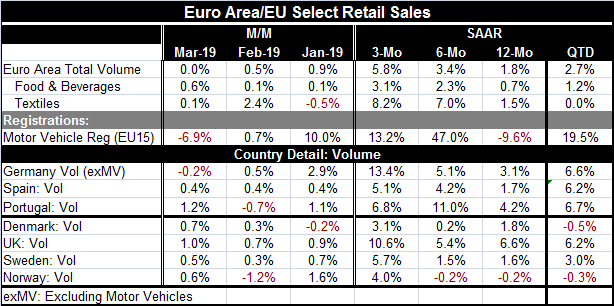

Retail sales volumes in the EMU are slightly elevated but remain on a moderate growth path after going flat month-to-month in March. Sales volume is up by 1.8% over 12 months, accelerating over six months and accelerating also over three months. However the year-to-date selling pace for the just completed first quarter is at a more modest 2.7% pace, below its three-month, and six-month pace.

Retail sales volumes in the EMU are slightly elevated but remain on a moderate growth path after going flat month-to-month in March. Sales volume is up by 1.8% over 12 months, accelerating over six months and accelerating also over three months. However the year-to-date selling pace for the just completed first quarter is at a more modest 2.7% pace, below its three-month, and six-month pace.

Component sales

Both food & beverage and textile sales show sales volume expansion and acceleration from 12-months to six-months to three-months. Likewise, sales for the quarter-to-date for each of these categories reveals a sales pace that is more subdued.

Motor vehicles sales

Motor vehicle sales fell sharply in March, but those sales are volatile and they had surged by a strong 10% month-to-month in January. As a result, auto registrations are still rising at a 13.2% annual rate over three months and by a much stronger rate over six months, but they are falling by 9.6% year-over-year. The auto registrations data do not paint a clear picture of consumer conditions in Europe.

Sales history

One thing that both retail sales and auto registrations tell us is that European sales are not strong over 12 months but that there has been some pickup from earlier weakness. Retail sales growth rates peaked in July 2017 after peaking and slowing at a higher pace in 2015. Sales decelerated through October 2018 after which they become volatile and swung more widely. In March, the pace of sales has cooled a bit at 1.8%. Over the previous two months, sales volumes in the EMU had struck a year-over-year pace at 2.7%. That is where the quarter-to-date pace continues to hover.

Country by country sales

Sales by country are firm with seven sample early reporting European countries shown in the table; only three of them are EMU members. Still, only Germany shows a real sales decline in March. All of these countries show a gain over three months with the slowest pace at 3.1% (annualized). Over six months and 12 months, only Norway shows sales declines. Germany and Spain, the largest and fourth largest EMU economies, show the pace of sales accelerating from 12-months to six-months to three-months. The three EMU reporting economies (including Portugal) each have real retail sales up at a 6% pace over 12 months one year ago and then all three show sales slowing from that pace over the most recent 12 months. Even though Portuguese sales are not accelerating within the more recent 12-month span (sales decelerate from six-months to three-months), their growth is solid.

On balance, the euro-consumer is doing well

Interestingly, with all the concerns about growth and central bank policies, the Sentix index of investor sentiment in the EMU rose in May to its highest level since November. While various Markit indexes and country-level indicators remain weak, the conventional adding up of actual retail spending leaves Europe in a much more solid place than expected. The March retail sales report is a welcome respite from past industrial barometers that have flagged economic slowing. Still, economic performance will be a blend of the two. Right now the consumer is looking a bit stronger than the producer.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief