Global| Sep 05 2018

Global| Sep 05 2018EMU Retail Sales Drop in July and Risk Still Lives Here

Summary

Retail sales in the European Monetary Union (EMU) countries dropped by 0.2% in July, lowering their three-month growth rate to a 1.5% annual pace. Retail sales in the EMU are rising at just a 2.1% pace over six months and by 1.2% over [...]

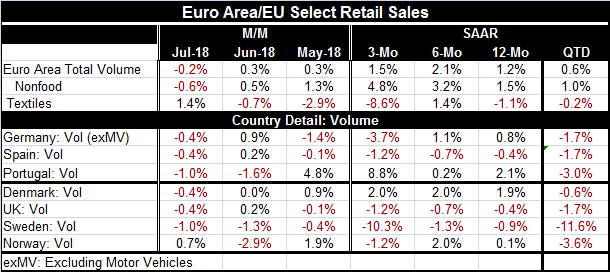

Retail sales in the European Monetary Union (EMU) countries dropped by 0.2% in July, lowering their three-month growth rate to a 1.5% annual pace. Retail sales in the EMU are rising at just a 2.1% pace over six months and by 1.2% over 12 months – no strength there and too low to be called stable despite the tight range for growth.

Retail sales in the European Monetary Union (EMU) countries dropped by 0.2% in July, lowering their three-month growth rate to a 1.5% annual pace. Retail sales in the EMU are rising at just a 2.1% pace over six months and by 1.2% over 12 months – no strength there and too low to be called stable despite the tight range for growth.

Country detail on sales shows impressively uniform weakening in sales among European economies whether in the monetary union or not. Among early sales reporting members, Germany, Spain, and Portugal report falling sales in July. Among other European countries, Denmark, the U.K., and Sweden log declines with Norway (a non-EMU and non-EU country) posting the only sales increase in July in the table.

It is July so we are only one month into the third quarter. Even so, we can calculate the growth rate of sales in July over the Q2 base and see how sales are growing in the new quarter. For the entire euro area, the QTD (quarter-to-date) growth rate is an annual pace of 0.6%, quite slow. But notice that in the table every reporter is showing sales declining in the third quarter-to-date.

The U.K., Sweden, and Spain show sales declines on all horizons and progressively weakening growth rates for retail sales volumes. Denmark shows sales steady at a 2% pace. Portugal is the only other country showing growth on all horizons and there growth is topped by accelerating performance over three months.

For the EMU as a whole, nonfood sales show sales rising on all tenors and actually accelerating from 12-months to six-months to three-months.

However, the main conclusions we draw from these data are that sales are weak in profile and weak across most European economies.

While the ECB and BOE have been making plans to end their stimulus policies and the BOE has even moved in that direction, the economic data have weakened causing central banks to put their plans on hold.

PMI data are dodgy too

The PMI data from Markit was finalized for August today and for all of the EMU. There is a slight pickup for the overall EMU PMI with manufacturing slipping a bit and services ticking higher. Neither sector is much changed on the month, but the overall effect is for a gain in the composite index. The service sector improved in Germany, France, and Spain but weakened in Italy. Both Spain and Italy post PMI readings that are exceptionally weak by the standards of the last five years while France and Germany are relatively moderate by those same standards.

It is fair to say that Europe is experiencing some unevenness in growth. In new U.S. trade data today, the U.S. experienced widespread declines in its export volumes. China logged a weak PMI along with what appears to be a lingering slowdown in Europe. Certainly, European retailing is weak. The global picture is less than secure. Still, the Markit PMIs show most global PMI composite indexes are improving in August. But the levels of the PMI gauges range from moderate to exceptionally weak. Of 13 countries or regions reporting composite PMI data, six show standings below their five-year medians. Only one country out of 13 has a standing of its composite PMI in the top 30% of all readings over the past five years. Most of the readings are in the 54th percentile to 69th percentile range which is a positive range but not a very impressive one.

Returning to Europe’s condition, we can see that the consumer is not driving growth there. Retailing is fading. Europe always has depended a lot on trade and much of that trade is within Europe among EU and EMU members on the continent. Although the U.S. trade war with Europe is at a truce stage now, it is still a worry. Meanwhile, the U.S. and China continue to go down the path to actual tariff imposition. At a time when growth is more uneven, this is a condition that becomes more threatening to economic expansion. The slip of South Africa into recession, the problems in Turkey, the spread of unsettled foreign exchange conditions to Indonesia, and of course, not to forget Argentina being Argentina, all are warnings that things can still get out of hand and that markets can recalibrate very quickly. Risk still lives here.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief