Global| Feb 20 2015

Global| Feb 20 2015EMU Recovery Strengthens: Builds on Domestic Conditions

Summary

The chart tells a clear story of what is going on in the EMU. The domestically oriented services portion of the economy is engaged in a rapid recovery and closing in on its cycle high reading, but the manufacturing sector in the EMU [...]

The chart tells a clear story of what is going on in the EMU. The domestically oriented services portion of the economy is engaged in a rapid recovery and closing in on its cycle high reading, but the manufacturing sector in the EMU is only stabilizing and marking a very slow nearly undetectable move higher. While there is all this TALK about foreign exchange rate wars and such, it is the domestic portion of the economy that is actually benefitting. And this is only after the announcement of a planned QE program ahead of any actual QE purchases themselves.

The chart tells a clear story of what is going on in the EMU. The domestically oriented services portion of the economy is engaged in a rapid recovery and closing in on its cycle high reading, but the manufacturing sector in the EMU is only stabilizing and marking a very slow nearly undetectable move higher. While there is all this TALK about foreign exchange rate wars and such, it is the domestic portion of the economy that is actually benefitting. And this is only after the announcement of a planned QE program ahead of any actual QE purchases themselves.

The sequential historic averages over three-months, six-months and 12-months continue to show weakness in train, but we know from the flash data that deceleration is coming to an end. But it's a sudden end that has not been tipped off in the readings of even one month ago. France has its highest private sector reading in 42 months; an alarmingly strong-sounding reading yet, the raw score is only 52.2 on the PMI scale and that is only a queue standing in the 66th percentile, barely in the top third of its historic range of values.

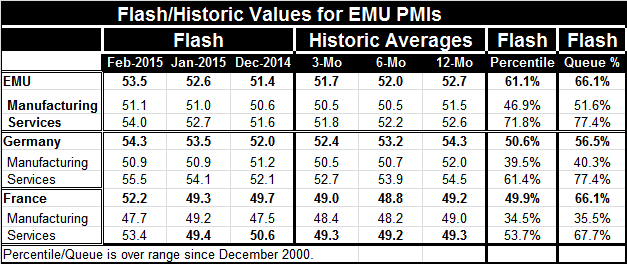

EMU reading shows the overall PMI up to 53.5 in February from 52.6 in January and residing in its 66th queue percentile. Manufacturing has crept up by 0.1 points to 51.1 to stand in its 51st percentile with the services metric bouncing to 54 from 52.7 to reside in its 77th percentile, now perched in the top 25 percentile of its historic queue.

Germany and France each have stark stories to tell with manufacturing either flat or weaker on the month but each with a stronger services sector; France's services sector popped by four full points from last month's preliminary reading. Still there is a huge gap between the services and manufacturing standings. Germany's manufacturing standing is in its 40th percentile while France's is in its 35th percentile. The German services standing is in its 77th percentile while for France services reside in their 67th percentile. Germany and France show a larger manufacturing-services gap queue standing gap than for the EMU as a whole, despite their combined large weight in the assembly of the euro-weighted average.

The upshot is that for the rest of EMU manufacturing is doing much better in relative terms than in either France or Germany since the EMU reading for manufacturing stands in its 51st percentile, well above Germany's 40th percentile standing and France's 35th percentile standing. The EMU standing for services matches the high for the German-France pair at Germany's 77th percentile, underpinning the notion that for the EMU as a whole the services sector has become some sort of a driving force.

While the plunging euro exchange rate should be lighting a fire in the EMU and it does appear to be lifting the manufacturing readings in the rest of the EMU, it is not the driving force. The real story is of gains in the relatively more insulated services sector s of EMU members. This is not the way the story has been told of late. Spain has been showing substantial improvement, but unemployment rates have not been driven down substantially there or the EMU as a whole (Spain's unemployment rate is lower by 1.9% over 12-months, on balance, and still stands at 23.7%). The services sector is notorious for its dependency on labor and for its low productivity.

On data through December the three-month changes show seven of 11 EMU nations with SOME declines in their unemployment rates. And only three (Finland, Portugal and the Netherlands) show higher unemployment rates over three months. Still, for the EMU as a whole, the aggregate unemployment rate is down by only 0.1 percentage point over the recent three months. That is still pretty bare-bones progress despite the breadth of the decline it across EMU members. The aggregate unemployment rate in the EMU still ranks just 21 percentile points off its cycle high. And unemployment rates in the EMU among 11 reporting countries show lower rates in seven of 11 of them with rates lower year-on-year by 0.4 percentage points and the number unemployed lower by 3.7%. There is progress being made. And the polar ice cap is melting (the one is the south is gaining mass to compensate). Not all change goes to the bottom line.

Greece: An Update on Circumstances

As I write this, we await word of Greece's fate. Will the Germans find a way to compromise and how much? There is evidence of a softening in German rhetoric. Or is it finally lesson-time for Greece and will it have its feet kept to the fire? Will this be an historic decision moment for the EMU where Greece decides, `should I stay or should I go?' Or will the other forces within the EMU convince the Germans to kick the can down the road and get more slop on their shoes?

As you can tell, I am increasing compelled by the argument that Greece needs to bend to rules instead of bending the rules to Greece. Greece needs to keep its promise and show it can stand on its own two feet in the EMU. The constant propping up of a drunk while buying him drink is not proof that all is well with him or that he can hold his liquor. At some point, he must kick the habit and stand unaided. Greece has been set a stern task and the euro area waited far too long to lay down the law. But once done, there is no going back and no backsliding. The Greek voters appealed to a small rogue political party to elect it to initiate backsliding. It is the sort of thing that cannot be rewarded. It sets the wrong incentive for Italy, Spain Portugal and maybe even France.

While Germany may be too stern a task master, it is true that what does not destroy you makes you stronger. The Irish are an example. If the Greeks survive, they will be much stronger. Or they can kick out, kick back, re-launch the drachma, deal with crisis and hyper-inflation, then reset their old lifestyle cycle. Either way there is a lot of pain in store before a stable equilibrium will ensue. There is no easy path for Greece from here on out. Europe could be better off either way. As long as Greece does not get the signal of ongoing appeasement, this could be euro-learning and defining moment.

The fact that despite all the austerity and ahead of the impact of the FX stimulus and QE stimulus Europe is doing better is a remarkable result. But it is the result of only one month's data. Still, it is far more than I had expected. It is very hopeful. If anything, it's a reason to appeal to Greece to stay the course. And this is a position I have generally not thought to be the best. But things change. As they do so must opinion. Sometime hope does spring eternal. And sometimes hope is unrequited by fact.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief