Global| Aug 22 2013

Global| Aug 22 2013EMU Recovery Continues as Does Bifurcation

Summary

The Markit 'flash' indicators for the euro-Zone show continued improvement in the manufacturing and services sectors in August. The euro-Area manufacturing index is up to 51.3 from a level of 50.3 in July. The services sector made a [...]

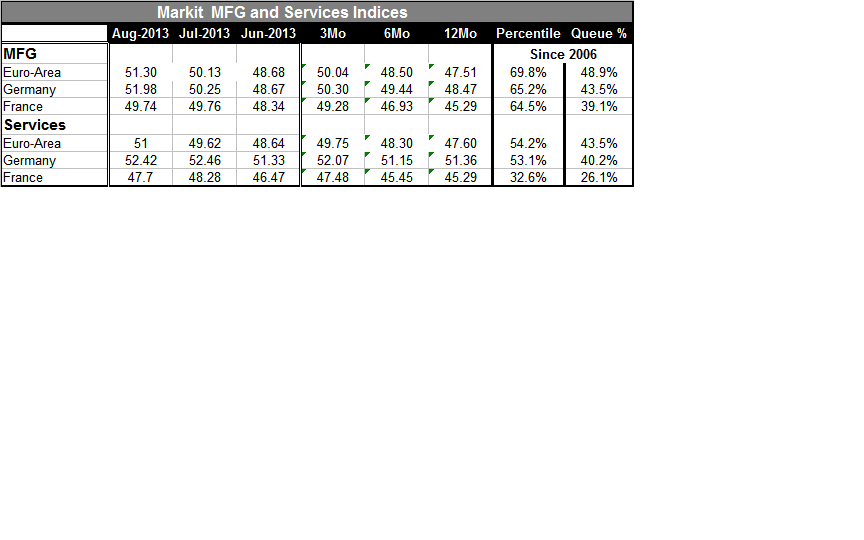

The Markit 'flash' indicators for the euro-Zone show continued improvement in the manufacturing and services sectors in August. The euro-Area manufacturing index is up to 51.3 from a level of 50.3 in July. The services sector made a sharper gain but to a slightly slower pace with its index at 51.0 compared to 49.62 in July.

The Markit 'flash' indicators for the euro-Zone show continued improvement in the manufacturing and services sectors in August. The euro-Area manufacturing index is up to 51.3 from a level of 50.3 in July. The services sector made a sharper gain but to a slightly slower pace with its index at 51.0 compared to 49.62 in July.

Both sectors in the Eurozone show steady progress from 12 months to six months to three months. The manufacturing index is higher in relative terms as it stands at the 48.9 percentile of its historic queue since 2006. The services index sits only at its 43.5th percentile since 2006, in the middle of its 43rd percentile.

In August, Germany shows continuing increases in its manufacturing PMI. It has moved up from 48.67 in June to 50.25 in July and is at the 51.98 level in August 2013. By comparison France, the second-largest country in the Monetary Union, flattened out in August at 49.74 just slightly weaker than its 49.76 reading in July but up from its 48.34 reading in June. The shortfall of the French index relative to the neutral value of '50' indicates that output in MFG is still contracting. Both France and Germany show substantial progress from 12 months to six months to three months but France is now hesitating to continue in August and output is still declining.

On the services side of the equation, Germany is showing expansion but not any increase in it pace in August as its level of 52.42 is slightly below its 52.46 reading for July. In France the service sector backtracked in August. It had improved fairly sharply to 48.28 in July from 46.47 in June. However, in August, it has fallen back to 47.7. Since it's below the level of 50, it shows that the sector is contracting and contracting in a slightly faster pace than it was in July.

Both the French services and manufacturing sectors are still shrinking.

Putting aside the changes in the diffusion levels for the manufacturing readings in Germany and France the position of those manufacturing readings in their historic queues remain low. Even though Germany shows a diffusion index that indicates expansion, the German index only sits at the 43rd percentile of its historic queue, still 6.5 percentage points below what has been its median. For France the relative position is somewhat worse as its manufacturing index sits at the 39th percentile level indicating a nearly 11 percentage point shortfall from its historic median since 2006.

Viewing the service sector from a percentile standing basis, the German index, while showing expansion, is relatively lower in its historic profile than even its manufacturing index, sitting at the 40th percentile of its historic queue. However, France's service sector is shrinking and shrinking faster in August and is much weaker than Germany, sitting only in the 26th percentile of its historic queue barely above the lower quartile of its historic queue of values since the year 2006.

While there is some optimism about the Monetary Union because of these improved PMI levels in August (and earlier) much of the improvement owes to Germany and the strong weight it bears in the Monetary Union. Since Germany has an economy based on export-led growth the improvement in Germany doesn't have the same kind of transmission or 'locomotive' effect that you might think. Its main impact on the EMU index is through the high weighted value that it contributes to the overall EMU standing. The weakness in France is illustrative as it is another important EMU economy that is adjacent to the German economy and it is not being pulled up very strongly by the German revival. The same is true of many other European Monetary Union economies that are still struggling and that still have issues.

To have confidence in the Monetary Union's revival we need to look beyond what the euro-Area index is doing to see what a substantial number of the countries in the Union are doing. The large weight for Germany in the EMU index, while perhaps correct for some methods of analysis, obfuscates the underlying trends and smothers intra-union divergences. We remain circumspect about what's really going on in the Monetary Union and somewhat wary of future prospects simply because the underlying circumstances in so many European economies still have some holes, question marks, and needs. We would like to see the improvement from the micro-economic ground up instead of from the macro-economic data down. That is not happening.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief