Global| Jun 02 2021

Global| Jun 02 2021EMU Reaches HICP 'Goal' Sooner Than Expected As PPI Spurts...So?

Summary

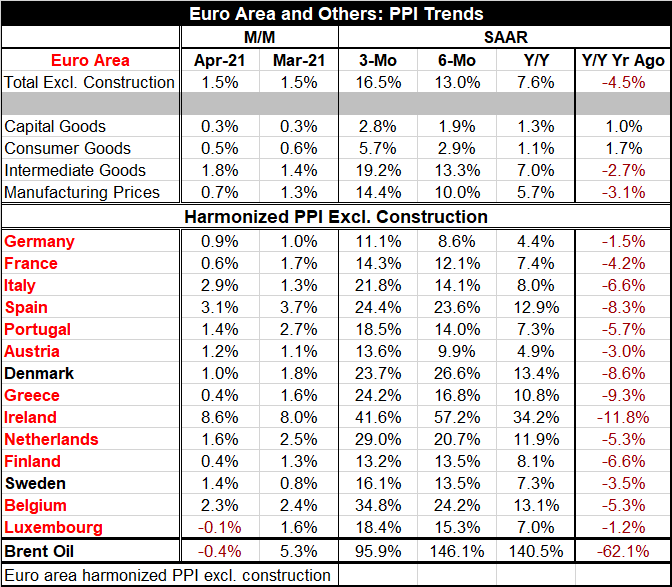

A perusal of the early reporters of PPI results in the EMU shows clear-cut broad and virulent inflation at work. Of the 14 countries in table (of which 12 are EMU members; Sweden and Denmark are not), all show price increases in April [...]

A perusal of the early reporters of PPI results in the EMU shows clear-cut broad and virulent inflation at work. Of the 14 countries in table (of which 12 are EMU members; Sweden and Denmark are not), all show price increases in April except Luxembourg. Finland and Greece at a 0.4% gain have the smallest increases on the month, followed by France at 0.6%. Nine countries in the table report month-to-month PPI increases of 1% or more. Germany checks in with a 0.9% month-to-month increase. Inflation, suddenly, is more wild than tamed.

A perusal of the early reporters of PPI results in the EMU shows clear-cut broad and virulent inflation at work. Of the 14 countries in table (of which 12 are EMU members; Sweden and Denmark are not), all show price increases in April except Luxembourg. Finland and Greece at a 0.4% gain have the smallest increases on the month, followed by France at 0.6%. Nine countries in the table report month-to-month PPI increases of 1% or more. Germany checks in with a 0.9% month-to-month increase. Inflation, suddenly, is more wild than tamed.

What happened to that quiescent, unmovable, slow, plodding, pace for prices?

The ECB is in a pickle

These results follow the HICP which topped 2% much earlier than expected. Since the ECB is a 'one-pillar' institution, it will be interesting from here on out to see how the central bank conducts its business since inflation is now at/over its objective of 'just less than 2%.' The results of this month's PPI suggest that the pressures are real – although inflation this intense rarely lasts at such a pitch. As I write this, global oil prices are topping $70/barrel implying that whatever inflation is coming from oil is not about to turn tail and run. It still has momentum.

The future of oil prices

In the U.S., President Biden has just revoked permits to drill in the Arctic that President Trump had approved. Biden had previously killed an oil pipeline from Canada that was already in progress. Fracking has also been discouraged. This kind of U.S. support for a 'green new deal' seems much more likely to help to support higher oil prices than to reverse their recent gains. OPEC and Russia will be happy even as it puts the EMU members in a fix.

Inflation by sector-what does it mean?

Inflation by sector-what does it mean?

However, the breakdown of inflation pressures in the EMU does show that the upward push to and above 2% for the PPI stems from intermediate product prices, not from capital goods prices and not from consumer goods prices (or at least not yet). This means that most of the pressure is coming from the raw goods contained in the intermediate goods categories including oil. Still, oil prices, even though they seem always to be volatile and unable to be depended upon, right now, they appear to be rather well underpinned by the combination of rising demand and constricting supply.

PPI trends

Looking at the PPI trends, the fourteen countries in the table all show larger gains over 12 months than they did over 12 months one year ago. Six-month price gains annualized exceed 12-month price gains. And for all but three countries, three-month price gains annualized exceed six-month price gains annualized. This means that the progression of inflation is well established as the rate of change in prices has been increasing steadily over these various horizons covering the last two years. While that span had been a period in which inflation had been low, the degree of acceleration is impressive and the breadth of acceleration is also very impressive. Over three months only Denmark, Ireland and Finland fail to show higher inflation rates than they have over six months – still each one of these countries has a three-month inflation rate in double digits over three months! Danish inflation is at a 23.7% pace over three months and Ireland is at 41.6% pace; yet, in each case the result marks a deceleration from the six-month pace.

It's 'be careful what you wish for' time

In sum, there is little inflation consolation to be found here. Inflation at long last is rising. Inflation at long last is no longer marginal. The debate that is 'on' over how long this inflation will last… Is this inflation simply a bounce-back from global lows created when Covid-19 swept across the global economy depressing prices as it spread? Or is there staying power in this rise and is it the kind of price push that policy has to meet head on or at least to alter its stand for?

The Mini-Max solution to policy-making

There are takers of both sides of that bet. There are strong arguments on both sides, too. However, I believe the deciding factor is arrived at in recognizing that policy-making is by its very nature always made in an environment of uncertainty. The fact that there is a policy or economic outcome debate is not new or even unique. Central bankers have to ask themselves which risks seem more authentic- as always! One way of doing this is by central bankers asking themselves this question: “If policy is wrong, what is the better error to make?” This way of thinking is called 'mini-max.' The idea is to minimize the maximum damage in the event of a mistake – the adoption of a wrong policy. It is a wholly different process than a maximizing routine. When central bankers enter this mode, they are no longer maximizing growth or minimizing inflation; they are looking for the safest policy option in difficult times.

The preferred policy framework

A mini-max frame of mind should lead central banks to policy caution about rising inflation. They do not need to ramp rates up, but they do need to address extant forces of inflation and to mitigate their own respective contributions to pushing growth and inflation higher with proactive monetary policies. Fiscal policy is less like to chill early. Monetary policy is the first responder in macroeconomic policy. However, policy does not need to act to stamp out inflation just to begin to withdraw some stimulus and to demonstrate vigilance and responsibility.

How this might work...

By becoming less expansionary, monetary policy can help to put the toothpaste back in the tube. Seeing central banks act responsibly as inflation flares will have a different impact on behavior than their sitting back and watching while doing nothing. And I think that cutting off this rise in inflation pressure – or at least pushing back against inflation psychology, is a desirable thing to do. However, I also find merit in the argument that inflation will not run wild. This is why I favor a moderate 'show the flag' response. Some point to large debt and argue that it is inflationary. Others conclude the opposite from the same observation! Not different facts but different conclusions – well, that's refreshing! So which is it? I think when debt is run up it is inflationary and after it has been run up it becomes deflationary. We have had the impact of a huge increase of debt and there has not been that much inflation since much of the debt functioned as income replacement – it was not piled on in addition to the normal flow of income. EMU data shows us that inflation there is all in intermediate goods. Unless debt issuance continues to run wild – and in the U.S. it still may- as we get to the point that the debt has to be serviced debt will become deflationary. I think monetary policymakers need to take at good close look at the debt cycle and how fiscal policy is set to act in the future as they make their policy choices. It's not a simple thing, it's not a coin-toss, and I believe the future is not yet decided and that is why the conduct of policy matters. It's a good thing that there is a debate about it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief