Global| Sep 02 2015

Global| Sep 02 2015EMU Producer Prices Continue to Fall

Summary

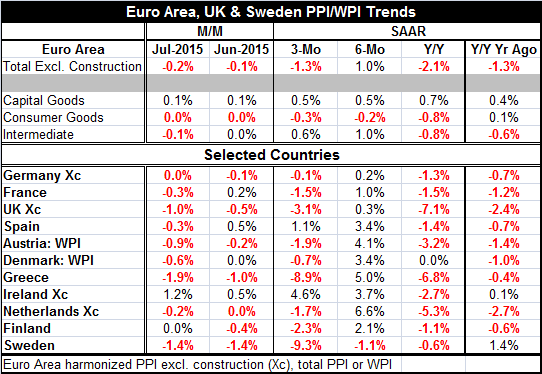

The PPI headline shows a monthly drop of 0.2% in July and a year-over-year decline of 2.1%. Two of the three PPI components are declining year-over-year. Those two are consumer goods and intermediate goods. Capital goods prices are up [...]

The PPI headline shows a monthly drop of 0.2% in July and a year-over-year decline of 2.1%. Two of the three PPI components are declining year-over-year. Those two are consumer goods and intermediate goods. Capital goods prices are up by 0.7% year-over-year.

The PPI headline shows a monthly drop of 0.2% in July and a year-over-year decline of 2.1%. Two of the three PPI components are declining year-over-year. Those two are consumer goods and intermediate goods. Capital goods prices are up by 0.7% year-over-year.

However, capital goods prices are not accelerating as their three-month pace is slower than the pace of their year-over-year rise. Intermediate goods, however, have transitioned to increases over three-month and six-month, but without consistent acceleration evidence. Consumer goods prices, while falling on all horizons, are falling more slowly over three-month and six-month than over 12-month. On balance, there is a hint that the deflationary cycle may be easing, but it is only a hint. There are opposite hints elsewhere. A new wave of weak oil price and commodity price weakness definitely could bring back the downward pressures.

Moreover, countries continue to show PPI price declines. Ten of 11 countries show declines in PPI prices over 12 months (one is unchanged). Then, over six months, 10 of 11 countries show prices increasing! However, again, over three months we see a return to price declines as 9 countries show net declines over three months with two showing increases (Spain and Ireland).

Obviously, there is still great deal of price weakness in play. Global growth conditions are weak with China still touch and go. Equity markets have returned to their ways of volatility this week and wealth losses continue. Such pressures hint at continuing weak economic times and the ongoing postponement of price pressures.

The ECB, of course, targets consumer prices using the HICP measure. But producer prices also give an important signal. Japan is once again telling us it is not clear that it has thrown off deflation risk despite the BOJ explicitly targeting 2% inflation. In the U.S., inflation is stuck low. The price lethargy in Europe is its own of making, but there are still important international dimensions that continue to spread deflationary pressures.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief