Global| Sep 23 2014

Global| Sep 23 2014EMU Private Sector PMI Hits Lowest Flash Value Since December

Summary

The euro area continues to struggle in September with its flash private sector gauge falling to 52.3 from 52.8 August. This is the lowest flash value for the index since December 2013. While the six-month average is still above the [...]

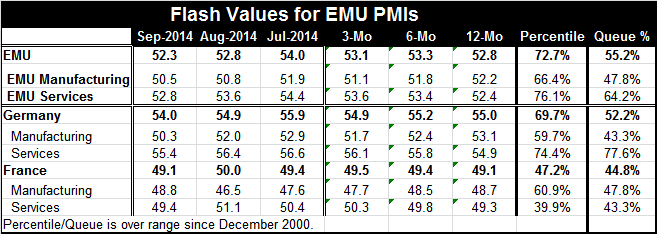

The euro area continues to struggle in September with its flash private sector gauge falling to 52.3 from 52.8 August. This is the lowest flash value for the index since December 2013. While the six-month average is still above the 12-month average, the three-month average with this report is now below the six-month average for the PMI value for the EMU as a whole. We take this value and place it in the history of all PMI values; the current value sits in the 55th percentile of its queue of historic data. That means that the PMI is higher about 45% of the time and lower about 55% of the time.

The euro area continues to struggle in September with its flash private sector gauge falling to 52.3 from 52.8 August. This is the lowest flash value for the index since December 2013. While the six-month average is still above the 12-month average, the three-month average with this report is now below the six-month average for the PMI value for the EMU as a whole. We take this value and place it in the history of all PMI values; the current value sits in the 55th percentile of its queue of historic data. That means that the PMI is higher about 45% of the time and lower about 55% of the time.

Manufacturing and services gauges in the EMU both eased to lower levels in September. The three-month, six-month and 12-month moving averages for manufacturing continued to decline, while the moving averages for services continued to edge slightly higher from period to period.

The manufacturing gauge for the EMU sits in the 47.8 percentile of its historic queue. It is below its midpoint, which occurs at the 50th percentile level. Services are stronger in broad terms and substantially stronger in queue percentile terms as they sit in the 64th percentile of their historic queue, still a very moderate reading but more comfortable.

Germany's private sector index slipped in September and also slipped in August. Germany's three-month average has slipped below the six-month average for the private sector gauge. And its private sector gauge sits only in the 52nd percentile of its historic queue, a week reading. Germany's manufacturing gauge continued to slip, falling relatively sharply to 50.3 in September from 52 in August. Germany's manufacturing averages continue to fall from 12 months to six months to three months. Germany's manufacturing gauge sits only in the 43rd percentile of its historic queue, quite a weak reading. Germany's services sector also eroded in September and also fell in August. But it's 12-month, six-month and three-month averages show some steady improvement. The services sector queue percentile standing is also relatively firm in its 77.6 percentile. Right now it is the lifeblood of the German economy.

Turning to France, we see its private sector gauge began slipping back below 50, falling to 49.1 in September. France's overall gauge shows declines in output (values below 50) over three months, six months and 12 months, but over that period there is a very slight tendency for the private sector PMI to strengthen. France's overall PMI stands in the 44.8 percentile of its historic queue, a very weak reading. France's manufacturing reading rose in September to 48.8 from 46.5. The index is still below 50, signaling the manufacturing sector is still contracting. The moving averages for the manufacturing PMI show continued weakness from 12 months to six months to three months. The manufacturing sector's queue percentile standing is in the 47.8 percentile, below its median which resides at the 50th percentile. France's services sector continues to be stronger than its manufacturing sector, although its services sector gauge fell to 49.4 in September from 51.1 in August. From 12 months to six months to three months, the French services sector is posting slightly firmer services readings. The three-month average is above 50, at 50.3. Still the queue standing for the services sector is in the 43rd percentile of its historic queue, a very weak reading, weaker than the queue standing for manufacturing.

The manufacturing sector is the part of the economy that is most directly affected by external events. The services sector is relatively buffered. By that analysis, we see Germany with its much stronger services sector is being held aloft by its domestic economy while external forces batter its manufacturing sector. But for France, both manufacturing and services are being battered. The services sector is relatively weaker than manufacturing in percentile standing terms. France does not have the same backbone to fall back on domestically as Germany.

Other metrics released today showed that China's manufacturing index bumped up slightly in September. It still posts a very weak move and a low reading. A separate report in France on business confidence showed that the business climate was weakening in September.

The general landscape indicates a continued depressed world economic environment. For the EMU as a whole, this month conditions continued to slip and remain at extremely moderate levels. The German and French economies are both still under pressure and appear to be weakening although the slippage is at a slow pace. For Germany, it means slower growth; for France, it means continued contraction. There is no silver lining in today's data. Yesterday EMU confidence slipped to a seven-year low. Today the PMI erosion puts private sector activity is in the same boat.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief