Global| Mar 22 2016

Global| Mar 22 2016EMU Private Sector Picks Up in March But Fails to Restore Full Confidence

Summary

The chart puts the evolution on the EMU-area PMIs in their proper context. Last month the two sector indices fell sharply. This month there is a partial rebound with services rebounding slightly more and manufacturing showing a very [...]

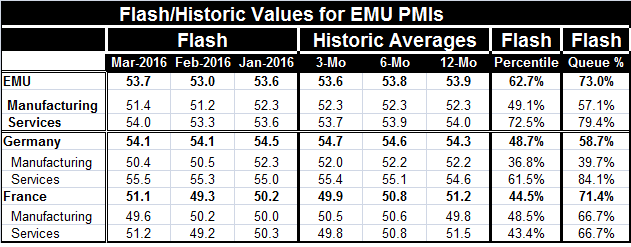

The chart puts the evolution on the EMU-area PMIs in their proper context. Last month the two sector indices fell sharply. This month there is a partial rebound with services rebounding slightly more and manufacturing showing a very small bounce. The EMU-wide services sector reading is still somewhat low compared to its range of the past year although it does sit at its one-year average value. Manufacturing is clearly lower than it has been and sits below its 12-month average. The EMU manufacturing rating over the various sequential periods has been steady at 52.3; however, the month's value sits well below that mark. For services, there has been ongoing erosion in the moving averages. This month's reading boosts the index back to its 12-month average and is an offset to the ongoing erosion.

The chart puts the evolution on the EMU-area PMIs in their proper context. Last month the two sector indices fell sharply. This month there is a partial rebound with services rebounding slightly more and manufacturing showing a very small bounce. The EMU-wide services sector reading is still somewhat low compared to its range of the past year although it does sit at its one-year average value. Manufacturing is clearly lower than it has been and sits below its 12-month average. The EMU manufacturing rating over the various sequential periods has been steady at 52.3; however, the month's value sits well below that mark. For services, there has been ongoing erosion in the moving averages. This month's reading boosts the index back to its 12-month average and is an offset to the ongoing erosion.

Germany shows contrary trends in its sector indices. Manufacturing had been relatively steady before plunging last month and is holding to a lower level this month. Services have been gaining momentum and this month's rise puts the German services index above all its sequential average readings. The services reading is the strongest since November 2015 and the third strongest since August 2014. Clearly the German services sector is doing a great deal to pump up the German economy, an economy traditionally led by its manufacturing sector.

Also on release today is the German ZEW index for March. That index features a current and an expected reading. Here again there is a split. The German current index eased lower while expectations made a small advance. Still, the rankings of the two sectors are opposite to their respective monthly movements. Expectations are weak (stronger 72% of the time) while the current situation is stronger only 19% of the time. Still, the ZEW current index has slipped for two months running. It made a sharp transit lower from September to October last year, having been oscillating toward lower levels since then. ZEW expectations hit a 16-month low last month, but this month rebounded (skipping last month) to its weakest reading since October 2015 and since October 2014 before that. The ZEW index, while not on the ropes, it is showing signs of wear and tear. Migrant issues have blown up in the face of European officials recently as the EU has struggled for a solution. The devastating bombing in Brussels today is only going exacerbate tensions over migrants further.

In France, the composite PMI reading edged back over 50 to register expansion. In February, it had slipped below 50 for the first time in 13 months. Now it is back signaling expansion albeit weak expansion. The French composite index had been below 51 for three months running until this month. France's manufacturing sector is back with a sub-50 reading, its first since August 2015. The services sector, which weakened sharply one month ago (below 50), is back up at a 51.2 reading, its strongest reading in four months. Despite a very low PMI value, the manufacturing index sits in the 66th percentile of its historic queue of values, the same as its service sector reading.

Still, the overall EMU PMI has only a 73 percentile standing. Germany's composite has a 58th percentile standing while France has a 71st percentile standing. These are moderate to soft readings and not exactly achieved on good momentum. The ongoing squabbles regarding migrants and the recent Belgian terrorist bomb detonation surely are going to mean further challenges to growth in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief