Global| Nov 30 2009

Global| Nov 30 2009EMU Prices Rise - Has The Worm Tuned?

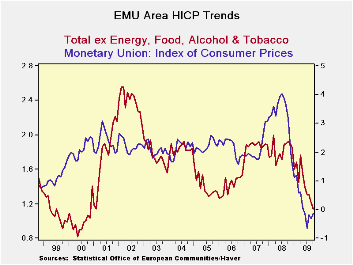

Summary

EMU prices rose in October. Trends are still good but core inflation is showing a hint of acceleration as three month core prices are up at a 1.4% annual rate above their six-month and 12-month pace of increase. Headline inflation [...]

EMU prices rose in October. Trends are still good but core inflation is showing a hint of acceleration as three month core prices are up at a 1.4% annual rate above their six-month and 12-month pace of increase.

Headline inflation shows a clear acceleration from an annual pace of -0.1% Yr/Yr to a +1.2% annual rate over six-months and to a 2.3% annualized pace over three- months.

Germany, France, Italy and Spain all show the same accelerating headline inflation pattern from 12-months to six-months to three-months. Italy’s 3-mo inflation rate is up to 3.4% annualized.

Core inflation has much less clear patterns across countries.

Core inflation is not accelerating from 12-months to six-months to three-months in any of these large EMU countries. It is accelerating from six-months to three-months in Germany and in Italy. But that similarity has little breadth. In Italy core inflation is running at a strong 4.1% pace. In Germany it is at 1.1% only the same as its Yr/Yr pace but up from its six-month pace. In France the core rate is still steadily decelerating. Spain’s core is back down after a pop-up over six-months.

On balance combined with news that UK consumers are repaying credit this holiday season and that German firms are having a tough time getting credit, it hardly seems that inflation is about to take root. The recent rise in energy prices is the reason for most headline inflation to be creeping higher. Core inflation is still largely under wraps. Still it is notable that inflation is starting to show some traces in the more inflation-prone country of Italy.

We don’t expect any policy change in EMU but the inflation worm may be starting its turn. Even so we expect it to be a big slow turn, even for a worm.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Oct-09 | Sep-09 | Aug-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU | 0.2% | -0.1% | 0.5% | 2.7% | 1.2% | -0.1% | 3.2% |

| Core | 0.1% | 0.0% | 0.2% | 1.4% | 1.0% | 1.0% | 2.4% |

| Goods | 0.4% | 0.5% | 0.4% | 5.5% | -0.2% | -1.4% | 3.5% |

| Services | 0.1% | -0.7% | 0.2% | -1.7% | 1.1% | 1.8% | 2.6% |

| HICP | |||||||

| Germany | 0.2% | -0.3% | 0.7% | 2.3% | 0.7% | -0.1% | 2.5% |

| France | 0.0% | -0.1% | 0.5% | 1.3% | 0.8% | -0.2% | 3.0% |

| Italy | 0.0% | 0.4% | 0.5% | 3.4% | 1.1% | 0.2% | 3.6% |

| Spain | 0.1% | -0.3% | 0.7% | 2.1% | 1.9% | -0.6% | 3.6% |

| Core:xFE&A | |||||||

| Germany | 0.1% | -0.2% | 0.4% | 1.1% | 0.9% | 1.1% | 1.5% |

| France | 0.0% | -0.1% | 0.3% | 0.6% | 0.9% | 1.0% | 2.3% |

| Italy | 0.2% | 0.4% | 0.5% | 4.1% | 1.7% | 1.4% | 3.0% |

| Spain | 0.0% | -0.1% | 0.1% | 0.2% | 0.7% | 0.2% | 2.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief